SUMMARY

- We believe that a confluence of factors – not just concerns about China and Fed policy – has led to the sudden, sustained jump in volatility in recent weeks.

- Often, the best opportunities present themselves when uncertainty is running high. A carefully chosen actively managed equity strategy may help investors capitalize on opportunities in today’s market.

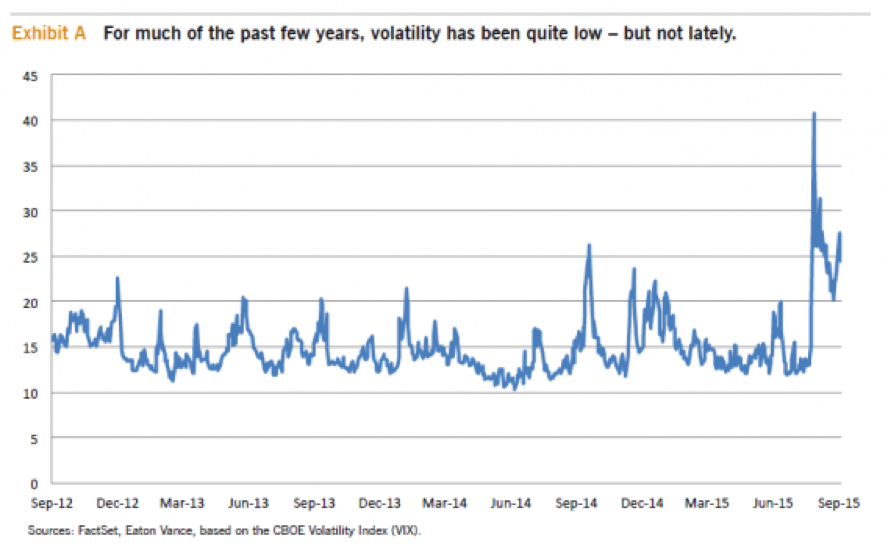

Prior to the final week of the second quarter of 2015, there were zero days when the S&P 500 Index rose or fell by more than 2%. In the third quarter, there were eight such days. As recently as August 17, the Chicago Board Options Exchange Volatility Index (VIX), a measure of implied future volatility on U.S. stocks, was at 13, a very low level relative to its history. One week later, without warning, it hit 53 intraday, more than quadrupling in the span of five trading days. As of early October, it was in the mid-20s, well above historical levels.

What caused the spike in market volatility and the sell-off in equities? Many market commentators have pointed to fears of slowing economic growth in China and uncertainty around the timing of Fed policy. While these may be the proximate catalysts, they do not explain why stocks have reacted so violently, in our view.

We believe that a confluence of factors has led to the sudden, sustained jump in volatility in recent weeks.

Price-insensitive sellers

A meaningful percentage of the equity market sells stocks without regard to fundamentals, valuations or the price that is achieved. These include index mutual funds (which must sell when they have outflows), ETFs (which must sell the underlying securities when there are net sellers of the ETF itself), and various pension funds and variable annuities that have implemented so-called "risk-parity" or "minimum volatility" programs that require them to "derisk" when measures of volatility (like the VIX) spike.

Regulatory pressures on brokerage firms

Historically, during a sell-off, Wall Street trading desks would use their balance sheets to buy stocks, which would often stabilize the market. As a result of the so-called "Volcker Rule," firms are prevented from making directional bets with their own money. Also, the Comprehensive Capital Analysis and Review (CCAR) rules around capital requirements for banks apply a heavy charge to risk-taking activities within the trading business, which has led many firms to reduce their commitment to this area.

Excessive crowding

In the first half of 2015, the breadth of the stock market had grown very narrow, with a handful of stocks accounting for the bulk of the market's performance. As momentum-based investors crowded into a smaller set of stocks, they became vulnerable to bad news. The best recent example of this is the health care sector, which had become the most popular sector in our investor sentiment monitor. During the recent market sell-off over the final six weeks of the third quarter, health care was the second-worst-performing sector in the S&P 500, exacerbated by the discussion in political circles of price controls for drugs.

Remember, volatility spells opportunity

It has been said by others that investors often pay a very high price for certainty. Volatility is the market's attempt to price uncertainty. History has shown that the best opportunities tend to present themselves when uncertainty is running high. If part of the market is made up of investors who sell without regard for price, it must represent opportunity for those of us who are willing to do the hard work of fundamental analysis and valuation. Those with the fortitude to embrace uncertainty should be able to benefit from the volatility, in our judgment.

At Eaton Vance, we are paying close attention to measures of crowding, including those stocks that are large constituents of ETFs. We maintain downside (as well as upside) price targets on current and prospective holdings to help guide the decision to act when a stock's price has become dislocated from its fundamentals.

Activate your portfolio

It has been a long dry spell for investors trying to find true bargains in the equity market. While much of the market still looks fairly to fully valued, it appears that pockets of opportunity have finally begun to materialize for discerning investors.

A carefully chosen, proven actively managed equity strategy may help investors to capitalize on emerging opportunities in today's market. As the U.S. bull market ages, we believe signs of a tipping point in favor of active management are building. Importantly, a key potential benefit of active management is the ability to manage risk in a volatile environment like today’s and potentially help limit losses when the market slides.

The S&P 500 Index is an unmanaged index commonly used to measure the performance of the broad U.S. stock market. The Chicago Board Options Exchange Volatility Index shows the market’s expectation of 30-day volatility and is a widely used measure of market risk. It is not possible to invest directly in an index. Unless otherwise stated, index returns do not reflect the effect of any applicable sales charges, commissions, expenses, taxes or leverage, as applicable. Historical performance of an index illustrates market trends and does not represent the past or future performance of any fund.

About Risk

Investments in equity securities are sensitive to stock market volatility. Equity investing involves risk, including possible loss of principal. Investments in foreign instruments or currencies can involve greater risk and volatility than U.S. investments because of adverse market, economic, political, regulatory, geopolitical or other conditions. In emerging countries, these risks may be more significant.

Past performance is no guarantee of future results.

About Eaton Vance

Eaton Vance Corp. is one of the oldest investment management firms in the United States, with a history dating to 1924. Eaton Vance and its affiliates offer individuals and institutions a broad array of investment strategies and wealth management solutions. The Company's long record of exemplary service, timely innovation and attractive returns through a variety of market conditions has made Eaton Vance the investment manager of choice for many of today's most discerning investors. For more information, visit eatonvance.com.

The views expressed in this Insight are those of Edward J. Perkin and are current only through the date stated at the top of this page. These views are subject to change at any time based upon market or other conditions, and Eaton Vance disclaims any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Eaton Vance are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Eaton Vance fund.

This Insight may contain statements that are not historical facts, referred to as forward-looking statements. Future results may differ significantly from those stated in forward-looking statements, depending on factors such as changes in securities or financial markets or general economic conditions.

Before investing, investors should consider carefully the investment objectives, risks, charges and expenses of a mutual fund. This and other important information is contained in the prospectus and summary prospectus, which can be obtained from a financial advisor. Prospective investors should read the prospectus carefully before investing.

©2015 Eaton Vance Distributors, Inc. | Member FINRA/SIPC | Two International Place, Boston, MA 02110 | 800.836.2414 | eatonvance.com