US Monetary Policy: It’s Déjà Vu All Over Again

Brooks Ritchey, senior managing director at K2 Advisors®, Franklin Templeton Solutions®, pays homage to the late Yogi Berra in this piece about monetary policy in the United States. Quoting one of Berra’s famous quips, Ritchey says that sadly, our collective future “ain’t what it used to be” and questions whether maintaining US interest rates at near zero may be doing more harm than good at this point.

In honor of baseball legend Yogi Berra, who died last month, I have decided to build my take on US monetary policy around a collection of his famous so-called “Yogi-isms”—sayings that seem to make no sense on the surface but which turn out to be both funny and wise after you give them some thought.

“It’s like déjà vu all over again.” – Yogi Berra

Before the news broke of Berra’s death, his “déjà vu” quip was top of mind for me given the Federal Reserve’s (Fed’s) decision to again postpone raising interest rates at its September policy meeting.

I must admit I was not exceptionally surprised by the decision, and neither were the markets; predictions regarding the probability of a hike had generally been split down the middle. If I had to describe my visceral response, however, it would be disappointment. I feel like the Fed may have missed an ideal opportunity to act. With this latest deferment, it is very possible the window for a hike in 2015 has been closed—and the earliest we may see an interest rate increase could now be early 2016—if not beyond. The odds seem low for a hike in October; there is no Federal Open Market Committee meeting in November, and the calendar—and Treasury market liquidity for that matter—is simply not favorable for a rate hike at the December 16 meeting, in our view. Could they move then? Possibly, but I’m not holding my breath.

“If you don’t know where you are going, you might wind up someplace else.” – Yogi Berra

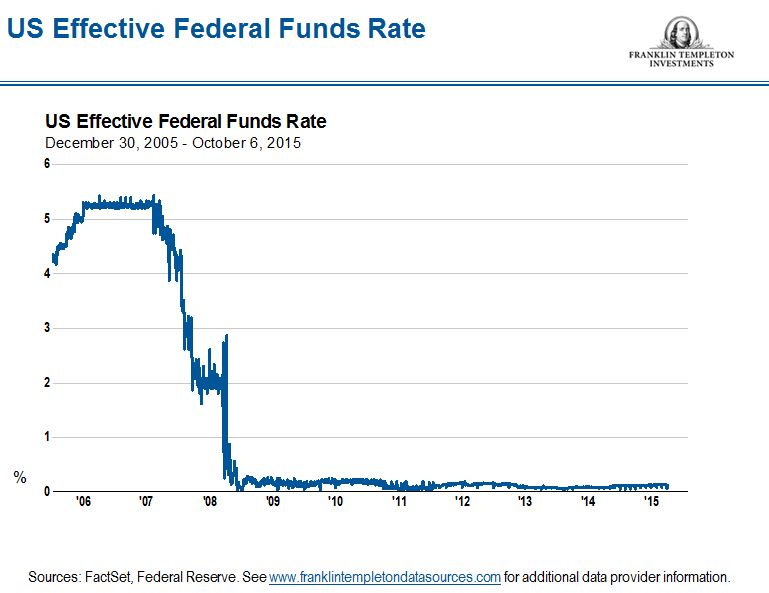

The bottom line is that the Fed has kept its benchmark interest rate (the federal funds rate) at near zero (zero interest rate policy, or ZIRP) for more than seven years. For the moment it looks like it will stay that way for the foreseeable future. I am beginning to believe this is a mistake, and the longer we head down this path, the further we are from where we need to be.

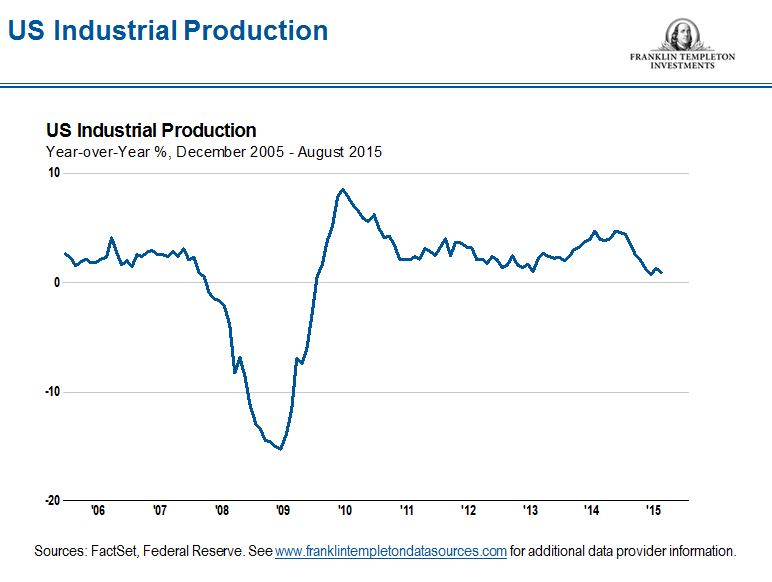

Lowering the rate initially was intended to provide support to an economy reeling from the Great Recession of 2007-2009, and was applauded by most economists at the time as the right thing to do. Many of those same economists today are now questioning its continued utility—as am I. While ZIRP initially provided much-needed liquidity during the crisis and a 200+% boost to major stock market averages, any associated economic growth that Former Fed Chair Ben Bernanke et al. attempted to engineer seems to be a little more dubious. For the most part, industrial output has remained tepid at best, and many corporations appear reluctant to commit huge sums of capital to their core businesses, instead plowing trillions into stock buy-backs, dividend hikes and mergers and acquisitions.

Bear in mind, this Fed is comprised largely of academic Keynesians, and it is their belief (hope) that the thousands of economic models they have created with their staff of hundreds of Ph.D. economists will lead the world down a path toward normalization. Forgive my skepticism, but I feel like we’ve all been down this road before. Recalling another quote from another famous sports figure, it’s like boxer Mike Tyson once said, “everybody has a plan until they get punched in the face.”

That is to say, perhaps it is naïve to expect these best-laid plans to work as predicted, given that they are based on theory and as such do not reflect the complexity and depth of the billions of economic reactions and participants influencing market behavior every day. The only way the Fed can build a model to describe such complexity is to assume away the real world; to impute market motives and relationships based on an implicitly imperfect, academic understanding of how things work and interact.

To me, this is not a realistic expectation. Even if we could plan our way back to sustained economic prosperity, a monetary instrument by itself already at its lower bound—the proverbial piece of string—is not enough to resolve growth problems in the developed economies, problems driven by fiscal shortcomings and a decade-long trend toward credit accumulation.

At a minimum, we need fiscal instruments—government budgets, tax policies and prudent regulatory policy—to remedy what is primarily a fiscal problem, in our view.

Fed Chair Janet Yellen’s predecessor Ben Bernanke knew this, and said so explicitly: “… monetary policy is no panacea. Many other steps could be taken to strengthen our economy over time, such as putting the federal budget on a sustainable path, reforming the tax code, improving our educational system, supporting technological innovation and expanding international trade.”

Indeed, from an Austrian-centric economic view, the primary reason we are in this position of yet again wondering why massive liquidity has not stimulated growth is because of—well—massive liquidity! That is to say the policy measures implemented are the same policies that put us here in the first place. In the simplest of terms it is like robbing Peter to pay Paul. In contrast to the Keynesians, those same Austrian economists would likely say that by using artificial stimulus to smooth the economy when things are a little rough simply postpones the necessary corrections, therefore making the pain that much more severe when the bill finally comes due. Essentially, they would probably suggest that ultra-easy monetary policy discourages the structural adjustments that are necessary at all levels, whether in governments, banks, corporations or households. In effect, zombie companies and governments are kept alive, and the financial sector is encouraged to misallocate.

So the question remains: Is maintaining a ZIRP in the United States today a good idea, or is not raising rates doing more harm than its intended good? I suppose that depends on perspective and opinion. Certainly from the perspective of the many retirees who have not earned much on a lifetime of bank savings over the past decade or so, the answer is an emphatic “yes” to the latter part of that question. Of course it is not solely mom and pop feeling the interest rate pain, but many others as well. It is the pension funds that are having difficulty growing assets quickly enough to meet exponentially growing liabilities, the markets that have been hamstrung in terms of the ability to naturally and efficiently allocate capital, and the strong companies forced to compete against businesses kept alive artificially by cheap credit. In other words, what was once a medicine for stimulating growth may in fact today be acting as a poison.

“You can observe a lot by watching.” – Yogi Berra

Lastly, some observations: In terms of what we can anticipate going forward with regard to market behavior, the global economy, and the prospect for growth, the outlook is perhaps more clouded today than it has been in a generation. As we noted, over the short term the quantitative easing (QE) experiment succeeded in staving off further contraction and buoying the financial markets. Longer term, its utility and impact is unclear to us. Presumably, the Fed believes the developed world will fully grow itself out from under its mountainous pile of debt and unfunded entitlements, which to me seems optimistic. There are many that argue QE served to only delay the inevitable, that the fundamental issues that caused the recession have not been addressed and that eventually the United States and other indebted nations around the world will be faced with the prospect of defaulting on obligations in some form or other. Only time will tell what the lasting impact of QE will be.

In the meantime, perhaps the only thing almost everyone agrees on—and a view that we are comfortable in endorsing with a high level of confidence as well—is that the future will bring more volatility. And, from an investment management perspective, we believe portfolios should be positioned accordingly—with an emphasis on risk mitigation, tactical asset allocation and true benchmark agnostic active management. A good dose of hope won’t hurt either; after all, as Yogi once said, “it ain’t over ’til it’s over.”

Brooks Ritchey’s comments, opinions and analyses are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including the possible loss of principal. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Bond prices generally move in the opposite direction of interest rates. Thus, as the prices of bonds in a portfolio adjust to a rise in interest rates, its value may decline.

© Franklin Templeton Investments

© Franklin Templeton Investments