KEY TAKEAWAYS

As companies report third quarter 2015 results, the health of the global economy will likely get plenty of attention.

The U.S., China, the Eurozone, and Japan account for nearly two-thirds of global economic activity; thus, these areas are where global growth matters the most.

The market continues to expect that global GDP growth will accelerate in 2015, 2016, and 2017, aided by lower oil prices and stimulus from two of the three leading central banks in the world.

The market continues to expect that global gross domestic product (GDP) growth will accelerate in 2015 (3.0%), 2016 (3.4%), and 2017 (3.4%) from 2014’s 2.0% pace, aided by lower oil prices and stimulus from two of the three leading central banks in the world. The prospect for another year of decelerating growth in emerging markets remains a concern for some investors, who may still be waiting (in vain) for China to post 10–12% growth rates as it consistently did during the early to mid-2000s. The likelihood of rate hikes in the U.S. in late 2015 and the U.K. in early 2016 is also a potential growth headwind. Still, much stimulus remains in the system, and more is likely from the Bank of Japan (BOJ) and the European Central Bank (ECB), which may help bolster growth prospects in two key areas of the globe. Although China is unlikely to embark on quantitative easing (QE), Chinese authorities have recently enacted a series of targeted fiscal, monetary, and administrative actions aimed at stabilizing China’s economy in 2015 and beyond; more such actions may follow, but fears of a hard landing in China persist.

WHY GLOBAL GDP GROWTH MATTERS

The outlook for global growth matters to investors because it defines the ultimate pace of activity that creates value for countries, companies, and consumers. As investors begin to digest the S&P 500 earnings reports for the third quarter of 2015 (36 S&P 500 companies will report third quarter results this week, with another 300 set to report in the final two weeks of October 2015), we provide an update on how consensus estimates for economic growth for 2015 and 2016 — in the United States and worldwide — have evolved over the past few years, and how they have been impacted by China, oil prices, and the stronger dollar. We’ll also look at how global growth estimates are tracking for 2017.

In recent years markets have focused more on global GDP growth, whereas in the past, prospects for U.S. economic growth garnered the most attention from market participants. Why does global GDP growth matter? As we have noted in prior Weekly Economic Commentaries, financial markets — especially equity markets — focus intently on earnings. Broadly speaking, earnings growth is driven by “top-line” growth, or revenue growth, less the costs incurred earning that revenue, with labor accounting for more than two-thirds of total costs.

A good proxy for global revenue growth is global GDP growth plus inflation. Thus, the pace of growth in the global economy is a key driver of global earnings growth, and ultimately, the performance of global equity markets [Figure 1]. As we note in the recent Weekly Market Commentary, “Earnings Preview,” the consensus of analysts expects that S&P 500 companies will post a 4% drop in earnings growth in the third quarter of 2015 versus the third quarter of 2014. The expected decline is primarily driven by the stronger U.S. dollar and the decline in oil prices; however, we expect more than a handful of firms may cite global growth concerns (mainly in emerging markets and especially in China) when discussing third quarter results and providing guidance for the fourth quarter of 2015 and beyond.

GROWTH ESTIMATES ARE ALMOST ALWAYS REVISED LOWER

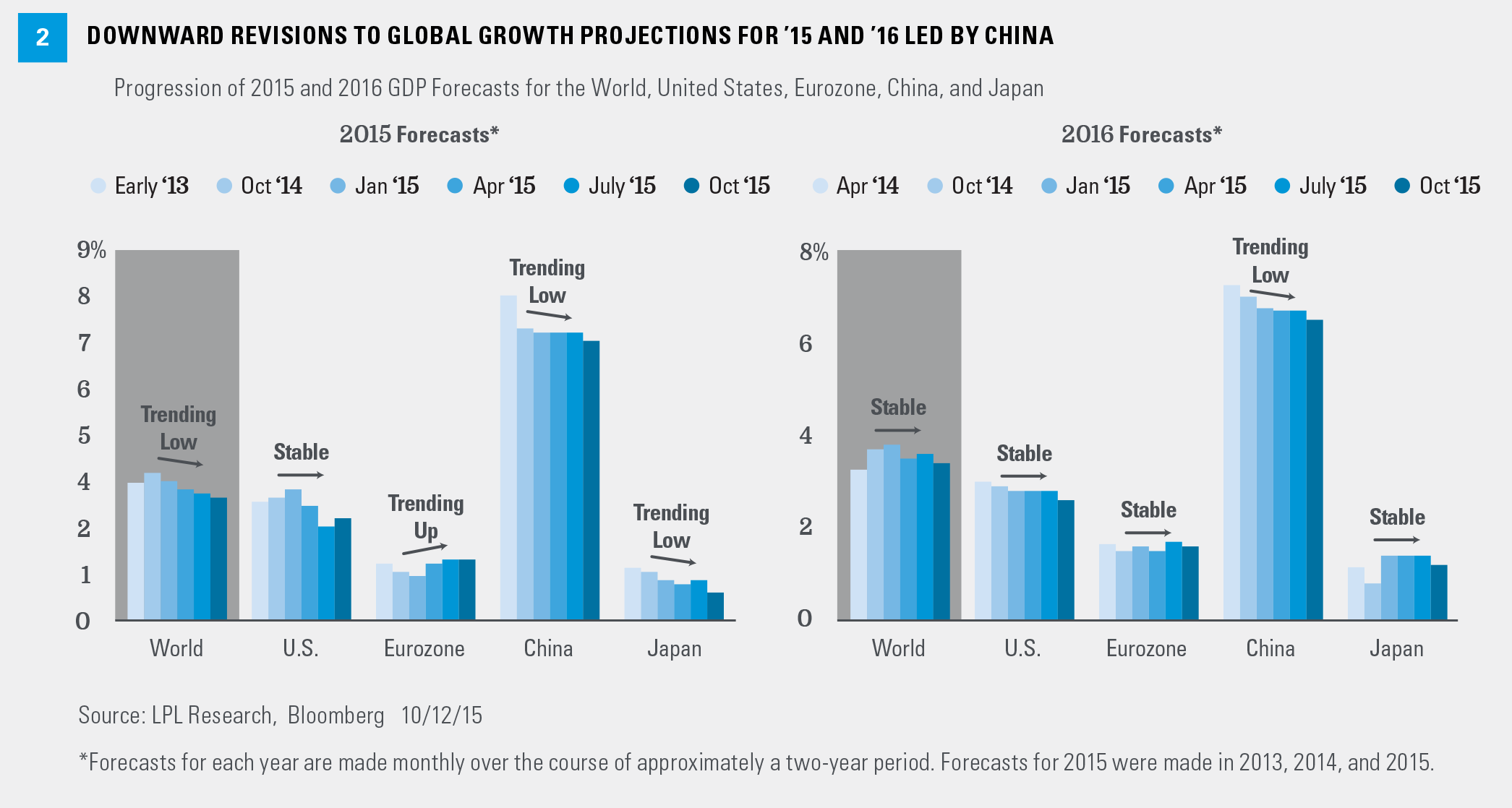

Figure 2 details the progression of the consensus GDP forecasts for 2015 for the world, the United States, China, the Eurozone, and Japan over the past several years. Figure 3 presents the changes over the past five years in the Bloomberg consensus estimate for global GDP for each year from 2011 through 2017, as an extension of the “world” bar. In short, the widespread and frequent reports in the media — most often cited by bearish investors — that “global growth has been revised downward” are technically correct, but miss the point that global growth estimates are almost always revised lower. Despite this pattern of revising GDP growth estimates lower, the global economy has been in recovery since 2009, and global equity prices — as measured by the total return on the MSCI World Index — are up 176% since March 2009, and have posted gains in five of the six calendars years from 2009 through 2014. Year to date through October 9, 2015, the MSCI World Equity Index is up 0.2%.

The latest (mid-October 2015) Bloomberg-tracked economists’ consensus forecast for 2015 global GDP growth stands at 3%, little changed from the 3.1% expected three months ago in July 2015 but below the 3.5% growth expected in 2015 at the start of the year. In early 2013, when Bloomberg first began tracking consensus estimates for global GDP growth for 2015, the consensus expected 3.4% world GDP growth. The downward revisions to 2015 global growth estimates are nothing new [Figure 3]. Consensus estimates for global GDP growth have been consistently revised lower since at least 2010.

Consensus estimates for global growth in 2016, which stood at 3.4% in October 2015, have also been moving lower since the start of 2015 (3.7%) and since 2016 estimates were first compiled by Bloomberg a year ago (October 2014) (3.8%). Here again, this should neither surprise nor concern global investors, as global growth estimates are almost always revised lower over time. The same pattern is emerging for 2017. In early 2015, when Bloomberg began tracking consensus estimates for 2017, the consensus was expecting 3.7% growth in 2017. Today, the consensus is looking for just 3.4% global GDP growth in 2017.

Several Factors Are Contributing to Regional Differences in Growth Estimates

The U.S., China, the Eurozone, and Japan account for nearly two-thirds of global economic activity. So while there have been major upward revisions to GDP growth estimates for 2015 and 2016 in places like India and Poland, major downward revisions to 2015 and 2016 growth estimates in Russia, Brazil, Mexico and Indonesia were offsets to overall global growth estimates. On balance, it is growth in the U.S., China, the Eurozone, and Japan that matters most.

U.S.: tracking to above-consensus 3.0%+ growth. Estimates for U.S. GDP growth for 2015 stand at 2.5% here in mid-October 2015. At midyear, the estimate was 2.3%. At the start of 2015, the consensus forecast for U.S. GDP growth in 2015 was 3%. The drop in oil prices, the stronger dollar, and probably most significantly, the poor start to 2015 (due to bad weather, the West Coast port strikes and cuts to energy-related capital spending) account for most of the decline in 2015 estimates from the start of the year (3.0%) to today (2.5%). The consensus estimate for 2016 (at 2.6%) hasn’t moved much this year, although the consensus estimate for 2017 has moved from 2.7% at the start of 2015 to just 2.4% today. We continue to expect 3.0%+ GDP growth over the final three quarters of 2015.*

China: struggling with transition to consumer economy. The consensus expects China to report 6.8% GDP growth this year and 6 – 6.5% growth in 2016 and 2017, and like global growth estimates, the consensus estimates for Chinese economic growth have been moving lower for years. Although China’s economy has been slowing since 2010, the recent pace of the slowdown has captured the market’s attention as fears of a “hard landing” (real GDP growth in the 4–5% range) persist. Chinese authorities have continued to struggle to implement the correct mix of monetary, fiscal, and regulatory policy to help guide China’s economy from an export-led manufacturing economy to a more domestically oriented consumer economy. Over the past few years, China’s property bubble gave way to a property price bust, and some of that “hot” money went into Chinese domestic equities, which soared by more than 160% between mid-2014 and mid-2015, before dropping 35% between early June and early October 2015.

In our view, the 35% drop in Chinese equities over the past several months does not represent any new information about China’s fundamentals any more than the 160% gain between mid-2014 and mid-2015 did. In fact, the 160% gain in Chinese stocks in 2014 and early 2015 was accompanied by generally deteriorating fundamentals for the Chinese economy and many Chinese companies. While we don’t think the large drop in Chinese equity prices over the past month foreshadows another leg down in the Chinese economy, it does distract Chinese officials from their stated goal of shifting the focus of China’s economy. Market consensus expects a 6.9% year-over-year reading for China’s third quarter GDP (due out later this week), and should be well aware that China’s property bubble has burst and that the Chinese economy is no longer growing at 10 – 12%.

Eurozone: improving global growth prospects as Greece concerns fade. Despite the continual discussions about Greece and its place in the Eurozone over the first half of 2015—and bucking the usual trend of downward revisions to growth over time—GDP growth prospects in the Eurozone have been revised higher for 2015 and 2016 since the start of 2015. Actions by the ECB to enact QE earlier this year, which, in turn, helped to heal Europe’s fractured banking system, have contributed to positive growth prospects in Europe. Europe is also benefiting from lower oil prices and from an unfreezing of the European financial transmission mechanism that has bottled up credit expansion to small and medium-sized businesses and households in Europe for years. Currently, the consensus expects 1.5% GDP growth in the Eurozone in 2015, accelerating to 1.7% in 2016 and 2017. The estimates for 2015, 2016, and 2017 are all higher today than they were at the start of 2015.

Japan: adding to global growth consistently. The BOJ is in a “wait and see” mode after enacting QE in early 2013 and increasing the size of the QE program in late 2014, and it has promised to do more if GDP growth in Japan falters or if deflation in Japan persists. The next BOJ meeting is in late October 2015, and given the deterioration in Japan’s growth prospects in recent months, some additional QE from the BOJ seems likely. Consensus GDP estimates for Japan in 2015 stand at 0.7%, down from 1.0% at midyear 2015. Growth estimates for 2016—which were revised up significantly between mid-2014 and mid-2015 to as high as 1.5%—have moved down since midyear and now stand at just 1.2%. Estimates for 2017 have remained steady at just under 1.0%. Although deteriorating demographics and large public debt levels will continue to weigh on Japanese growth in the coming years and decades, Japan is now consistently adding to global growth prospects for the first time in many years.

*As noted in the Outlook 2015, LPL Research expects GDP to expand at a rate of 3% or higher, which matches the average growth rate of the past 50 years. This is based on contributions from consumer spending, business capital spending, and housing, which are poised to advance at historically average or better growth rates in 2015. Net exports and the government sector should trail behind.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal and potential illiquidity of the investment in a falling market.

Investing in foreign and emerging markets securities involves special additional risks. These risks include, but are not limited to, currency risk, geopolitical risk, and risk associated with varying accounting standards. Investing in emerging markets may accentuate these risks.

Commodity-linked investments may be more volatile and less liquid than the underlying instruments or measures, and their value may be affected by the performance of the overall commodities baskets as well as weather, geopolitical events, and regulatory developments.

INDEX DEFINITIONS

The MSCI World Index represents large and mid-cap equity performance across 23 developed markets countries, covering approximately 85% of the free float-adjusted market capitalization in each. This index offers a broad global equity benchmark, without emerging markets exposure.

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.