The main US news this week was not economic, but political: Kevin McCarthy withdrew his bid to become Speaker of the House. As of this writing, several candidates have announced their desire to seek the position, but there is no clear front-runner. This couldn’t happen at a worse time: within the next 60 days, the debt ceiling must be raised and Congress must vote on a budget. And the leadership vacuum is occurring when 3Q US growth is projected to be weak. While there is never an opportune time for palace intrigue, this could potentially place the US’ credit rating in jeopardy and temporarily shut down the government. In short, the negative economic ramifications are very large.

The only major non-Federal Reserve economic news was the released of the ISM services index. Although it dropped 2.1%, it still printed a strong 56.9. Business activity and new orders are bullish at 60.2, and 56.7, respectively. Employment increased 2.3 to 58.3 while 13 of 17 industries expanded. The anecdotal points contains some cautionary comments:

- "Continued egg pressure from avian flu." (Accommodation & Food Services)

- "The turmoil in Europe has not affected our business." (Information)

- "Outlook improving, economic conditions stabilizing." (Educational Services)

- "Recent economic turmoil has caused sales to drop. We feel that this will be only temporary if the stock market returns to normal." (Retail Trade)

- "Continued concerns about the market impacting customer confidence and amount of orders." (Wholesale Trade)

- "Budget approval this month. Several capital projects expected to be funded." (Public Administration)

- "Depressed commodity pricing and government driven restrictions on the fossil fuel energy sector have, and will continue into the foreseeable future, negatively affected the current energy business condition." (Mining)

- "Our business remains strong and growing." (Health Care & Social Assistance)

Three recent events caused the concern: general instability (largely emanating from China), oil price weakness and the potential for a Washington budget stalemate.

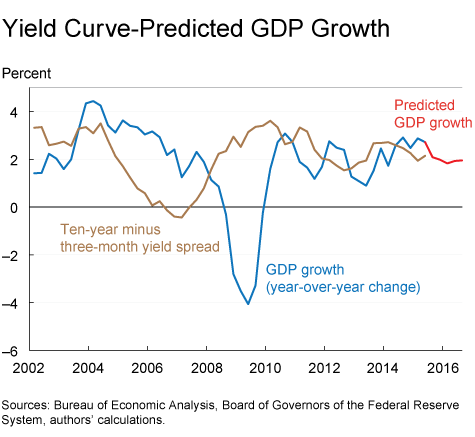

Projected GDP growth is still weak:

The Atlanta Fed’s model (top chart) is now ~1% while the Cleveland Fed’s interest rate based model is ~2% Y/Y.

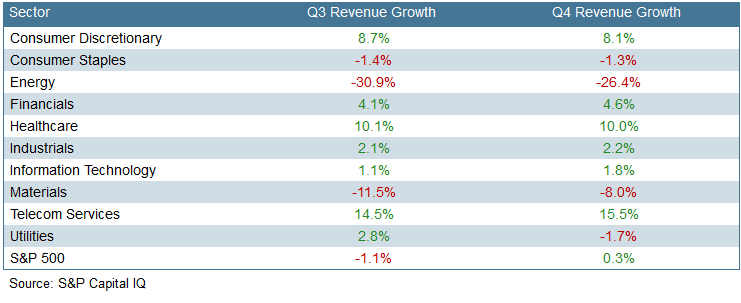

The market remains expensive. The current and forward PEs of the SPYs and QQQs are 21.52/17.01 and 20.75/16.85. For stocks to move higher, corporate earnings have to increase. Unfortunately, that will be difficult in the current environment. According to Briefing.com, analysts are projecting a 1.1% decline in 3Q S&P 500 revenue:

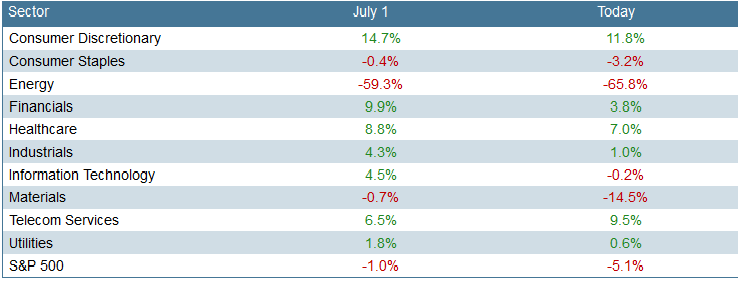

And EPS projections have not only dropped since July 1, but they are also projected to be negative:

Granted, the energy and material sectors are the primary reasons for the projected decline. But the decline in earnings estimates across all sectors since mid-summer indicates a broader weakness. And while the Chinese sell-off over the summer triggered the SPYs correction, the dearth of meaningful revenue and earnings growth will further hinder upside movement.

Let’s start by looking at the SPYs chart:

Prices traded between ~187-200 since the Chinese induced sell-off in the summer. But, within that trading range, prices also formed a double bottom, with the first low occurring in late August and the second in late September. (For more on this, see this article by Chris Kimble). On Thursday, prices broke through resistance, indicating a breakout was in play. This occurred around the same time as the index gave a very important and rare buy signal. According to my dusty Encyclopedia of Chart Patterns, the most likely percentage increase for a rally from this pattern is between 20-30%. A few other indicators (A rally in emerging markets, improved breath indicators and an energy sector rebound) are also supporting the bullish argument.

Other averages are potentially confirming the breakout:

Both the IWMs (Russell 2000, top chart) and IYTs (transports, bottom chart) have moved through downward sloping resistance. As an added bonus, the IYTs also formed a triangle pattern at the bottom of their recent downward sloping pattern.

But these breakouts are occurring while the treasury market still has a strong bid. The IEFs (7-10 year treasury) are near multi-year highs. The TLTs (20+ year treasury) are about ~10% off their recent highs, although they still have a decent bid. And the 30 year 2 year yield spread was 2.24% on Friday which is not bullish. When this data is combined with weak revenue and earnings growth, an environment unfriendly to bulls emerges.

The overall environment is still slightly bearish. The IMF lowered global growth projections earlier last week. US growth projections are lackluster, as are corporate revenue and earnings projections. While bullish indicators emerged last week, it’s difficult to see enough momentum to move the market through previous highs. To do so, we really need revenue and earnings growth, which just doesn’t seem to be in the cards yet.