At the beginning of every major disruptive innovation, fear, uncertainty and doubt reign supreme. Consumers are fearful of the unknown, uncertain of the benefits and doubt the durability of the innovation. But, in the end, fear, uncertainty and doubt give way to confidence, understanding and acceptance. The fund management industry is on the cusp of a major disruptive innovation.

In “Smart Beta 2.0: The Next Battleground for Asset Management Dollars Heats Up,” Moody’s describes how “asset managers are accelerating their expansion in the smart beta space, as alternative index strategies become more sophisticated and gain broader acceptance.”

The report continues: “This accelerating activity has coincided with a shift in the evolution of smart beta products from the basic – simple and static security selection and weighting schemes – towards the development of more sophisticated products that are based on multiple factors and timing of exposures. Smart beta’s next phase – call it ‘smart beta 2.0’ – will be more research intensive.

“This next phase will likely place smart beta funds in direct competition with traditional mutual funds … In a sense, smart beta 2.0 will evolve into a more disciplined and cheaper form of active management – that is, it will attempt to achieve the goals of traditional active managers, but at a lower cost and with more consistency in terms of adhering to a set of investing rules.

“Those most at risk are traditional mutual funds with highly diversified portfolios whose performance closely tracks, and typically lags, the index – e.g., closet indexers with over 100 securities in their portfolios. The AUM loss from these firms could directly accrue to asset managers well-positioned to offer the next iteration of smart beta funds.”

Smart beta is a disruptive innovation for investors. The promise of smart beta is excess returns in a cheaper, simpler and more predictable way. Before now, only mutual funds managed by humans could boast the potential for excess returns—and, if and when they did generate alpha, it was not necessarily repeatable: there were more unknowns, higher fees and higher taxes. Smart beta aims to capture these same excess returns in a cheaper, transparent and predictable, rules-based way.

Passive vs. Active vs. Index Realities

The emergence of ETFs in the 1990s allowed investors to invest mechanically in broad equity market segments for the first time. Previously, most assets in the United States were actively managed by investment managers. Over time, investors began to view the decision to invest in an index fund as a “passive” investment, and the decision to hire a portfolio manager via a mutual fund as an “active” investment. The emergence of smart beta funds has blurred the lines.

Today many view a fund following an index as a “passive” investment, which doesn’t quite tell the whole story. In “Indexes Can Be Passive, Active Can be Indexes, but Passive Can’t Be Active,” John Rekenthaler describes Morningstar’s approach:

“Historically, active and index investing have been viewed as binary events. A fund is either one or the other… It is fine to place exchange traded funds and indexed mutual funds into the same index group, and put all remaining mutual funds into the active group… Although even then, a third set is helpful. There’s a difference between indexes that weight securities according to market capitalization… and indexes that incorporate viewpoints… By our reckoning, the active/index duo should expand to three: 1) actively managed funds, 2) index funds weighted by market cap, and 3) strategic beta index funds.

“Let’s switch from discussing active vs. passive to active vs. index. Those are not the same things because passive is not a synonym for indexing. A passive fund is a fund that does not express a viewpoint. An index fund is a fund that mimics a list of securities. Those are two different things. Thus a strategic beta fund is an index fund, but it is not a passive fund.”

Let’s start by decomposing the terms passive and active management. A passively managed fund is designed not to take a viewpoint, as Rekenthaler put it, which means that passive funds follow benchmark indexes like the S&P 500 or MSCI World Index. When he says that passive funds don’t have a viewpoint, what he means is that they simply own all the stocks in a benchmark index, in the exact same weight. No human decisions are made in a passive fund. As the index changes, the fund is similarly adjusted. The fund performs almost identically to the underlying index, minus fees.

Traditionally, an actively managed fund is managed on a discretionary basis by a portfolio manager to achieve results relative to some benchmark. Portfolios usually represent a small fraction of the companies in the reference benchmark. Changes to the composition of the portfolio occur continuously as the portfolio manager adjusts the portfolio to pursue opportunities. For actively managed funds, performance tends to deviate from the benchmark, sometimes better and sometimes worse, minus fees.

A new form of active management has emerged, called smart beta. Smart beta ETFs are designed to follow an index, but that index is different than a benchmark index. Smart beta indexes do take a viewpoint on markets and express that viewpoint by a selection and/or weighting scheme that differs from a benchmark index. If we consider the true “activeness” of a fund—as we will discuss in the next section—rather as the extent to which a portfolio differs from a broad benchmark, then we can much more effectively analyze a fund’s true contribution to an overall portfolio.

Morningstar’s Rekenthaler goes on to describe the evolution of the fund management industry since 1994: “Active management dominated for the first 10 years … market indexes took control after the 2008 market crash and has never looked back; and … strategic beta, the newest member of the troika, is rapidly becoming a major force.”

Understanding Active Share

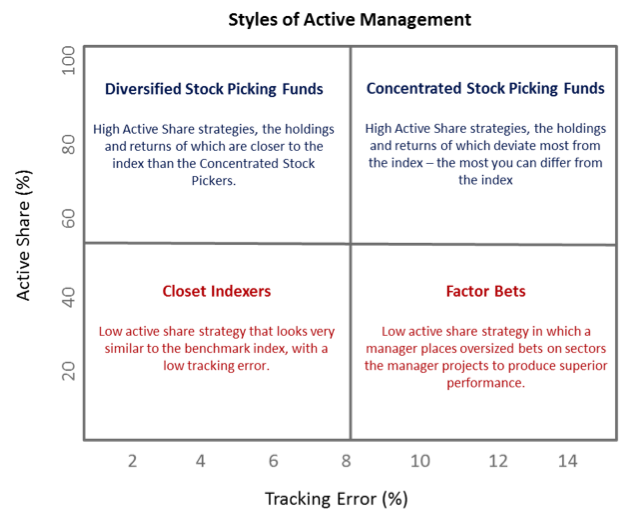

Thanks to the work done by Martijn Cremers and Antti Petajisto, investors now have a tool to measure how “active” a fund really is. Active share is a percentage (ranging from 0% to 100%) for long-only funds that measures how different a fund’s holdings are from the benchmark holdings. Cremers and Petajisto combine active share with tracking error to devise four types of active management styles: 1) closet indexer, 2) factor bet, 3) diversified stock picker, and 4) concentrated stock picker. Many actively managed funds, it turns out, tend to hold a portfolio of stocks that look very similar to the reference benchmark.

A closet indexer holds a portfolio that is nearly identical to the benchmark. These actively managed funds charge a higher fee, commensurate with an actively managed fund, for what is in essence a passive product. Closet indexers can be identified by their very low active share and very low tracking error. Not surprisingly, from 1990-2009, the authors found that after fees, these funds had the worst performance among all active asset managers.

Factor bets are actively managed funds that invest based upon systematic risk factors. These types of funds may invest in an entire industry or sector or use a timing rule to tactically move in or out of cash or other assets. Factor bets tend to have a high tracking error but a relatively low active share due to holdings which resemble the composition and weighting of the benchmark. Strategies that use ETFs exclusively for equity exposure often fall into this camp. The authors found that these funds sometimes can beat their indexes but for the most part, any outperformance disappears after fees.

Diversified stock pickers have a high active share and a low tracking error. They own a diverse portfolio of stocks, which allows them to achieve great deviation from the benchmark index. By extensively diversifying, they can eliminate much idiosyncratic risk. Many high ranking actively managed mutual funds fall in this category. The authors found that diversified stock picking funds consistently outperformed the benchmark after fees.

Last, the concentrated stock pickers have a high active share and a high tracking error. Concentrated stock pickers combine the best attributes of factor bets and diversified stock pickers by “taking positions in individual stocks as well as systematic risk.” This is a unique group, populated by high return, low risk allocation-style funds. Cremers and Petajisto found that concentrated stock picking funds consistently outperformed the benchmark after fees.

The Barbell Approach

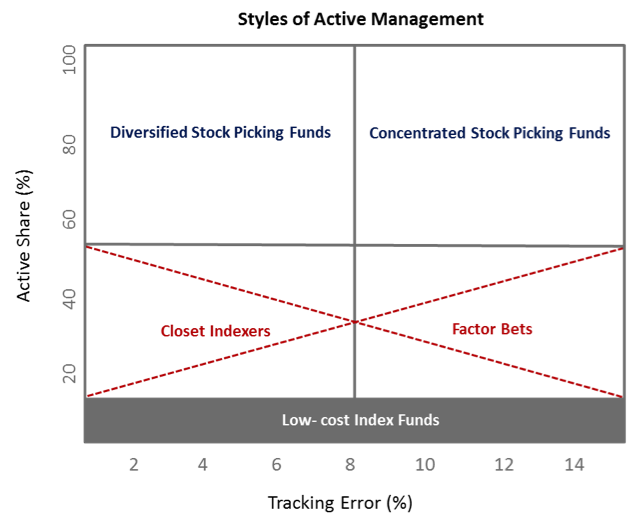

Petajisto updated his recommendations to investors in 2013 with even greater clarity. Investors should, he wrote, “…pick from the two extremes of active share, but not invest in any funds in the middle. The funds in the middle are providing only moderate levels of active management, which has not added enough value even to cover their fees. Closet indexers are a particularly bad deal, as they are almost guaranteed to underperform after fees given the small size of their active bets, yet they account for about one third of all mutual fund assets.”

From their work, we point out two easy rules for investors to improve any portfolio by focusing on the high and low ends of the active share spectrum, and eliminating the middle completely.

- Select high active share funds (diversified and concentrated stock picking funds), which consistently outperformed the benchmark after fees.

- Combine with low cost, passive index funds.

In the chart below, we show how to focus on funds on both extremes: high active share and passive index funds. Cremers and Petajisto call this strategy--to maximize portfolio efficiency and minimize fees--a barbell approach. We believe this approach should be a key consideration in portfolio management and drive all fund selection decisions.

Why Consider Smart Beta Funds

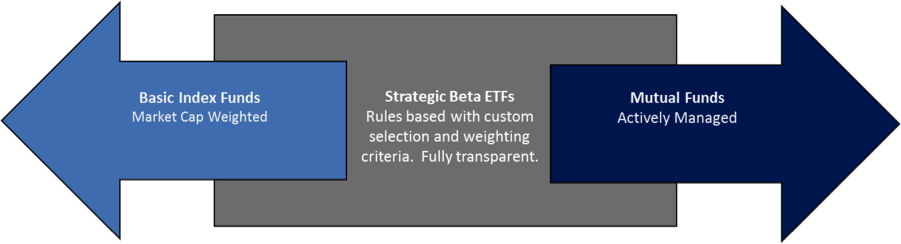

There’s another new type of product that can be employed to implement the barbell approach. Smart beta ETFs are index products that can combine some of the best characteristics of passive and active strategies.

There are key differences between benchmark index ETFs and smart beta index ETFs. The S&P 500 and most other well-known benchmark indexes are constructed using a market capitalization weighting methodology. The larger the company’s market cap, the larger the weighting it has in the index. Benchmark market cap-weighted index ETFs have an active share of zero relative to themselves. These passive indexes fall at the lowest end of the active share spectrum, and the key is they give exposure to the broad market and have very low fees. At the other end of the barbell are highly active strategies. These funds will have an active share between 60 and 90%.

Smart beta indexes are defined by their adherence to a rules-based, quantitative approach. Smart beta indexes use non-capitalization weighted, rules-based methodologies to construct an index. A smart beta strategy could be based on a fundamental characteristic (such as growth or dividend yield) or it could be based on a factor (such as size or knowledge intensity). What is most interesting about smart beta indexes is that they can exhibit active characteristics as a result of intentional deviations from traditional capitalization weighted benchmark indexes. This means smart beta indexes can have a high active share, offering investors an important additional tool which can be used alongside both passive and actively managed investments to create efficient portfolios that seek to combine the best of passive and active investment approaches while reducing fees. In the graphic below, we illustrate the three fund types.

Tax Considerations

One more significant reason to consider employing smart beta ETFs is tax impact. When evaluating the contributions that mutual funds and ETFs will make to the overall portfolio, it is also important to understand issues of intra-day liquidity and tax efficiency. Mutual fund trades are settled once per day, at the end of the market close, and all trades are settled at the end-of-the-day net asset value (NAV). Mutual funds generally hold limited amounts of cash, so a big redemption may necessitate a fund to sell a portion of its holdings to raise cash. These transactions can impact fund holdings and lead to realized capital gains for the remaining investors. ETFs, on the other hand, are traded intra-day and liquidity is provided by market makers, also called authorized participants.

ETFs generally are a more tax efficient investment vehicle than mutual funds due to the internal operating mechanics. When a mutual fund changes the composition of its portfolio, buying and selling stocks, it engages in cash transactions. These cash transactions can result in short and/or long-term capital gains. These gains are distributed annually to mutual fund shareholders. Shareholders generally have no way to anticipate when the mutual fund will realize capital gains or control whether the gains are short or long-term. When evaluating a mutual fund for prospective investment, it is almost impossible to determine the amount of unrealized gains in the fund and when they could be realized. In addition to annually distributed gains, mutual fund shareholders also are liable for capital gains taxes when they sell shares of the fund itself. There are two layers of taxes on most mutual fund investments.

An ETF, by contrast, modifies its portfolio by making what are known as in-kind transactions. On an ongoing basis, an ETF exchanges units in the fund with authorized participants for the basket of stocks comprising the fund’s holdings. When an ETF’s holdings change, for example at an index rebalancing, the ETF simply receives a basket of stocks reflecting the new index holdings from the authorized participant and exchanges units of the fund. In this way, where the ETF does not engage in cash transactions for securities, there is generally no tax liability generated within an ETF. ETF investors are liable for capital gains taxes when they sell the fund, but they can control whether the gain is short-term or long-term by their decision when to sell. Because ETFs do not distribute gains annually, ETF investors sidestep one layer of taxation, and this is why ETFs are typically more tax efficient for taxable investors.

One of the most underappreciated facts of mutual fund investing—especially six years into a bull market—is that, unless a mutual fund is brand new (or the NAV has been declining for some time), investors are buying into a portfolio that likely has embedded unrealized gains. For ETFs, this is generally not a concern. The operating mechanics of ETFs are such that they don’t generate taxes at the fund level, so there are no embedded unrealized gains to worry about. ETFs are a superior investment vehicle in taxable accounts because they sidestep one layer of taxation and allow an investor to decide when and what type of capital gain to incur.

Six years into an equity bull market, this complete absence of embedded gains makes it a very opportune time for an investor to consider the merits of an ETF to achieve equity exposure. Once investors make the switch from mutual funds to ETFs for core equity exposure, they will never have to worry about buying or receiving distributed capital gains again. This is partly why Goldman Sachs is expecting ETF assets to double over the next five years (http://www.etftrends.com/2015/06/etfs-3-trillion-is-nice-but-6-trillion-is-better/).

This is one of the key reasons why investors may want to consider using ETFs instead of mutual funds whenever possible. By filling up the lower and middle sections of the barbell with benchmark index ETFs, investors will find themselves having lowered overall fees significantly per basis point of alpha, and they will have fee budget left over to choose a few strategic, high active share mutual funds and/or ETFs that bring unique attributes to a portfolio (attributes that are not available in any benchmark index ETF).

Conclusion

Some smart beta index-based ETFs, depending on the construction methodology, have a very high active share. Some smart beta index-based ETFs offer a fusion of the rules-based, lower-fee benefit of index investing with the outperformance associated with higher active share strategies. A high active share should be a prerequisite for any smart beta strategy under consideration, as it has been linked to outperformance relative to a benchmark before and after fees.

As Moody’s suggests, there is a new battlefront in the money management business. New smart beta ETFs, so-called Smart Beta 2.0 ETFs, are entering the market to compete against actively managed mutual funds. These funds will be formidable competition for many actively managed mutual funds for a variety of reasons. In general, smart beta ETFs offer lower fees than actively managed mutual funds, both directly via lower expense ratios, but also indirectly via the elimination of annually distributed capital gains. They offer improved trading liquidity and transparency compared to actively managed mutual funds. And, smart beta indexes offer the possibility of superior performance, traditionally the province only of actively managed funds.

The asset management battleground is taking shape, and while the winners won’t be known for years, we can confidently predict investors will be the ultimate winner. In every disruptive innovation we have studied, from the telephone to the internet, the consumer is the ultimate beneficiary. We have entered the smart beta marketplace to be a force of disruptive innovation and help investors achieve their investment goals more efficiently. Smart beta 2.0 is here. Let the disruptive innovation begin.

This white paper has been adapted to remove product references at the request of Advisor Perspectives. For a detailed comparative analysis of smart beta indexes vs. actively managed funds, download the original version of this white paper here.

Sources

Agather, Rolf. “Smart Beta Indexes.” Journal of Indexes Europe: ‘Smart’ Beta Rising, December 2013.

Cremers, Martijn and Antti Petajisto. “How Active Is Your Fund Manager? A New Measure That Predicts Performance.” Working Paper, August 2006. Last revised May 2009.

ETF.com. The Definitive Smart Beta ETF Guide. May 2015.

ETF Securities. ETPedia.

Invesco. Smart Beta ETF Strategies

Moody’s Investors Service. “Smart Beta 2.0: The Next Battleground for Asset Management Dollars Heats Up.” Sector Comment. 10 September 2015.

Petajisto, Antti. “Active Share and Mutual Fund Performance.” Working Paper, January 2013.

Rekenthaler, John. “Indexes Can Be Passive, Active Can Be Indexes, but Passive Can’t Be Indexes.” Morningstar.com. September 25, 2015.

Schriber, Todd. “ETFs: $3 Trillion is Nice, but $6 Trillion is Better.” ETFTrends.com. June 8, 2015.

Vanguard. What are the five ETF structures?

Definitions

Active Share is the percentage of stock holdings in a portfolio that differ from the benchmark index. Active Share determines the extent of active management being employed by mutual fund managers: the higher the Active Share, the more likely a fund is to outperform the benchmark index. Researchers in a 2006 Yale School of Management study determined that funds with a higher Active Share will tend to be more consistent in generating high returns against the benchmark indexes.

Alpha is a measure of the portfolio’s risk adjusted performance. When compared to the portfolio’s beta, a positive alpha indicates better-than-expected portfolio performance and a negative alpha worse-than-expected portfolio performance.

Beta is a measure of the funds sensitivity to market movements. A portfolio with a beta greater than 1 is more volatile than the market and a portfolio with a beta less than 1 is less volatile than the market.

Correlation is the extent to which the returns of different types of investments move in tandem with one another in response to changing economic and market conditions. Correlation is measured on a scale of -1 (negatively correlated) to +1 (completely correlated). Low correlation or negative correlation to traditional stocks and bonds may help reduce risk in a portfolio and provide downside protection.

Upside/Downside Capture Ratio is used to show the relationship between the volumes of advancing and declining issues.

Information Ratio is a ratio of portfolio returns above the returns of a benchmark to the volatility of those returns.

Max Drawdown is the maximum single period loss incurred over the interval being measured.

The MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets.

Risk-adjusted Return is a concept that refines an investments return by measuring how much risk is involved in producing that return.

Sharpe Ratio uses a fund’s standard deviation and its excess return (the difference between the fund’s return and the risk-free return of 90-day Treasury Bills) to determine reward per unit of risk.

Standard deviation is a calculation used to measure variability of a portfolio’s performance.

Tracking Error is a measure of how closely a portfolio follows the index to which it is benchmarked.

Treynor Ratio is a risk-adjusted measure of return based on systematic risk. It is similar to the Sharpe ratio, with the difference being that the Treynor ratio uses beta as the measurement of volatility.

Volatility is a statistical measure of the dispersion of returns for a given security or market index.

Disclaimer

This document does not constitute an offer of services in jurisdictions where Gavekal Capital, LLC is not authorized to conduct business. All information provided herein by Gavekal Capital is impersonal and not tailored to the needs of any person, entity or group of persons. Past performance of an index is not a guarantee of future results. It is not possible to invest directly in an index.