Weighing the Week Ahead: What is Behind the Recent Market Volatility?

The recent market volatility has led to a lot of head scratching. Even the Pundit-in-Chief seems to be struggling to make his daily morning and evening observations fit with observed reality. With a light economic calendar and earnings reports just getting started market observers will be asking:

What’s the cause of the market volatility?

Prior Theme Recap

In my last WTWA I predicted that everyone would be wondering whether global weakness would drag down the U.S. economy. This proved to be one of my better guesses. Monday’s trading opened with concern about “record low industrial profits” in China and ended with the weaker-than-expected employment report on Friday. Nary had an hour passed during the week without someone chiming in on the global weakness theme. To get the wild weekly story, let us look at Doug Short’s weekly chart. This one saves more than a thousand words! (With the ever-increasing effects from foreign markets, you should also add Doug’s World Markets Weekend Update to your reading list).

Doug notes that the intra-day swing is in the top 3% of moves during this year. See his full post for more excellent charts and analysis.

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead. You can make your own predictions in the comments.

This Week’s Theme

Along with the increase in volatility there is a bull market in theories. Market observers like to think they can explain every move. It makes them seem smart on TV and also provides some comfort when trades go the wrong way. This week’s trading was especially interesting since big moves happened without a proximate news event to label as the cause.

With earnings reports just getting started and a light economic calendar, there is time for some pondering of the past. I was going to use, “What’s it all about?” with appropriate theme music, but I can be a little more specific. I expect the pundits to be asking:

What is behind the increase in market volatility?

As always, the viewpoints are varied.

The Viewpoints

Almost everyone has some theory about volatility including the following:

- Seasonality – it is just that time of year.

- Good news is now good news, and bad news is bad. This notion lasted for about two hours after the jobs report!

- Reaction to all data related to China, which always seems to signal weakness.

- Someone from the Fed said something.

- International conflicts and related effects on oil prices.

- Oil price movements. But why are higher prices viewed as a market positive?

- Thin markets are easily moved. Wait until earnings season.

As always, I have my own ideas in today’s conclusion. But first, let us do our regular update of the last week’s news and data. Readers, especially those new to this series, will benefit from reading the background information.

Last Week’s Data

Each week I break down events into good and bad. Often there is “ugly” and on rare occasion something really good. My working definition of “good” has two components:

- The news is market-friendly. Our personal policy preferences are not relevant for this test. And especially – no politics.

- It is better than expectations.

The Good

There was some good economic news – some of which is challenging to interpret.

- Government shutdown averted —for now. Removing uncertainty is a definite market positive. We’ll revisit this soon. Treasury Secretary Lew says that we need action within the next month.

-

Auto sales were excellent. This is an important spending indicator using non-government data. We should take it seriously. “Davidson” (via Todd Sullivan” writes as follows:

The history of vehicle sales shows that current rate is very high and still trending higher. The historical record reveals that at some point the sales trend eventually levels off and continues at high levels for 3yrs-4yrs prior to the next recession. We have yet to reach a sustained sales level. Sales are still rising!

- Construction spending beat expectations, but we need to use care in interpreting the data. Mesirow Financial has a nice update of the nuances.

- ADP employment showed a gain of 200K private jobs. This report is based upon actual payroll records for a significant segment of employers. The “official” government report is based upon a survey with a sampling error of +/- 100K jobs. We should embrace all sources of information, particularly when different methods are used.

- PCE inflation remained low. This is continuing good news, which many pundits have backwards. They cannot wait for the Fed to start raising rates. Low inflation gives them the flexibility to focus on the other mandate – economic growth.

The Bad

There was also negative news, with similar mixed themes if you look a little below the surface.

- Chinese industrial profits declined by 8.8%, the “lowest level on record“. This sparked Monday’s selling in U.S. stocks. I am scoring it as a negative in accordance with my rules, but this is a Silver Bullet topic waiting to happen. The data are not seasonally adjusted and there is no comparison to past months. More importantly, we keep seeing reports of weak manufacturing, which is the portion of the economy that is intentionally shrinking. Multiple reports on the same sector are being treated as independent information. Finally, the profit decline was partly based upon the currency devaluation that increased manufacturing costs. Give this a little thought. If U.S. markets treat the devaluation as a negative, based upon an appreciating dollar, then it is senseless to draw this conclusion about internal Chinese profits.

- Pending home sales decreased 1.4%, more than the expected 0.5%.

- Personal income remained positive at 0.3% growth but that was a bit lower than expectations. Spending was a bit higher than expected.

- ISM manufacturing was weaker than expected and barely in positive territory at 50.1. This poor report was immediately labeled as recessionary by many commenting, and it certainly does underscore the recent manufacturing weakness. To keep some perspective, it is helpful to read the official ISM commentary. Since manufacturing is declining versus services, you can have a negative ISM report and still have positive GDP. This reading, if annualized, is consistent with growth of about 2.2%.

| MANUFACTURING AT A GLANCE SEPTEMBER 2015 |

||||||

|

Index |

Series Index Sep |

Series Index Aug |

Percentage Point Change |

Direction |

Rate of Change |

Trend* (Months) |

| PMI® | 50.2 | 51.1 | -0.9 | Growing | Slower | 33 |

| New Orders | 50.1 | 51.7 | -1.6 | Growing | Slower | 34 |

| Production | 51.8 | 53.6 | -1.8 | Growing | Slower | 37 |

| Employment | 50.5 | 51.2 | -0.7 | Growing | Slower | 5 |

| Supplier Deliveries | 50.2 | 50.7 | -0.5 | Slowing | Slower | 2 |

| Inventories | 48.5 | 48.5 | 0 | Contracting | Same | 3 |

| Customers’ Inventories | 54.5 | 53.0 | +1.5 | Too High | Faster | 2 |

| Prices | 38.0 | 39.0 | -1.0 | Decreasing | Faster | 11 |

| Backlog of Orders | 41.5 | 46.5 | -5.0 | Contracting | Faster | 4 |

| Exports | 46.5 | 46.5 | 0 | Contracting | Same | 4 |

| Imports | 50.5 | 51.5 | -1.0 | Growing | Slower | 32 |

| OVERALL ECONOMY | Growing | Slower | 76 | |||

| Manufacturing Sector | Growing | Slower | 33 | |||

Manufacturing ISM® Report On Business® data is seasonally adjusted for New Orders, Production, Employment and Supplier Deliveries indexes.

*Number of months moving in current direction.

- Employment report was disappointing. The net increase in payroll jobs missed expectations by more than 50K. Prior months were also revised lower, and the labor participation rate was weaker. While some harbor hopes for an eventual revision, I do not buy it. Revisions are mostly based upon late-reporting firms. There is no reason to expect the laggards to have stronger results. It makes more sense to view several months of data at a time. The recent pattern has been weaker than the expected monthly growth of 200K. (But please note the Silver Bullet section while interpreting the data). The WSJ has a nice summary.

The Ugly

Air strikes. The Russian strikes in Syria are popular at home, even though there is doubt about the targets. Some recent U.S. strikes (not confirmed at the time of writing) may have also had tragic consequences. There are always justifications that seem right to leaders, but most hope that a peaceful solution can be found.

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. Think of The Lone Ranger.

This week’s award goes to Merrill Lynch economist Michelle Meyer (via Lisa Beilfuss at the WSJ). I have studied the employment report for many years, writing dozens of articles on these topics. Meyer’s analysis covers the most important mistake and myths, and does so effectively. She explains seasonal adjustments, the birth-death model, and the five-week month myth. It is excellent work.

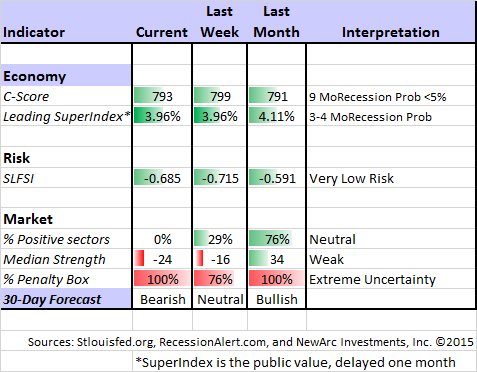

Quant Corner

Whether a trader or an investor, you need to understand risk. I monitor many quantitative reports and highlight the best methods in this weekly update. For more information on each source, check here.

Recent Expert Commentary on Recession Odds and Market Trends

Bob Dieli does a monthly update (subscription required) after the employment report and also a monthly overview analysis. He follows many concurrent indicators to supplement our featured “C Score.”

RecessionAlert: A variety of strong quantitative indicators for both economic and market analysis. While we feature the recession analysis, Dwaine also has a number of interesting systems. These include approaches helpful in both economic and market timing. He has been very accurate in helping people to stay on the right side of the market.

Georg Vrba: An array of interesting systems. Check out his site for the full story. We especially like his unemployment rate recession indicator, confirming that there is no recession signal. He gets a similar result from the Business Cycle Indicator. Georg

Georg also analyzes the market after a “Death Cross” event – often a weaker market, but not a time to panic. His work was featured in this Seeking Alpha article.

Doug Short: Provides an array of important economic updates including the best charts around. One of these is monitoring the ECRI’s business cycle analysis. Jill Mislinski has joined Doug’s team and provides this week’s update. The ECRI’s most recent article suggests that U.S. economic growth has been declining for eighteen months according to their indicators. They have continued in the chorus of Fed critics. While eventually stepping back from their mistaken and insistent recession call in 2011, ECRI has remained persistently bearish on economic growth.

With the avalanche of data, it is important to stop and consider what is really important. The single best way to stay grounded in economic reality is to check with Doug Short’s Big Four – the indicators important for official recession dating.

Brian Wesbury also explains that there is “no recession in sight”.

“Invictus” provides yet another comforting “no recession” indicator:

The Week Ahead

It is a modest week for economic data. While I highlight the most important you can get an excellent comprehensive listing at Investing.com. You can filter for country, type of report, and other factors.

The “A List” includes the following:

- ISM services (M). Stronger than the widely followed (but less important) older brother?

- Initial jobless claims (Th). The best concurrent news on employment trends, with emphasis on job losses.

- FOMC minutes (Th). Hard to believe that there will be fresh news, but the punditry will find some!

The “B List” includes the following:

- Trade balance (T). August data relevant for Q3 GDP.

- Wholesale inventories (F). August data also relevant for Q3 GDP.

- Crude oil inventories (W). Current interest in energy keeps this on the list of items to watch.

The official start of earnings season, but next week will open the floodgates. Brian Gilmartin helps us with what to watch. Join me in keeping a close eye on his earnings season reports.

How to Use the Weekly Data Updates

In the WTWA series I try to share what I am thinking as I prepare for the coming week. I write each post as if I were speaking directly to one of my clients. Each client is different, so I have five different programs ranging from very conservative bond ladders to very aggressive trading programs. It is not a “one size fits all” approach.

To get the maximum benefit from my updates you need to have a self-assessment of your objectives. Are you most interested in preserving wealth? Or like most of us, do you still need to create wealth? How much risk is right for your temperament and circumstances?

My weekly insights often suggest a different course of action depending upon your objectives and time frames. They also accurately describe what I am doing in the programs I manage.

Insight for Traders

Felix has turned bearish, as we noted was possible last week. Felix is only partially short since the penalty box indicator is on full tilt. This means that things are difficult to predict. Stay small or not at all. For more information, I have posted a further description — Meet Felix and Oscar. You can sign up for Felix’s weekly ratings updates via email to etf at newarc dot com. Felix appears almost every day at Scutify.

We have a signal from a “death cross four horseman” event. That has a suitably scary name. Based upon past occurrences the returns over the next month are expected to be negative, but are usually good on a three-month horizon. Traders should remain agile!

Insight for Investors

I review the themes here each week and refresh when needed. For investors, as we would expect, the key ideas may stay on the list longer than the updates for traders. Major market declines occur after business cycle peaks, sparked by severely declining earnings. Our methods are focused on limiting this risk. Start with our Tips for Individual Investors and follow the links.

We also have a page summarizing many of the current investor fears. If you read something scary, this is a good place to do some fact checking.

Other Advice

Here is our collection of great investor advice for this week.

If I had to pick a single most important article, it would be the overall economic and market assessment from “Davidson” via Todd Sullivan. I am very wary of anonymous writers, but this source has been very good for a long time. The contributions are always strong and data-based. I cited the basic auto sales facts above, but that is only part of the story. Here is his take on the initial pundit reaction to the employment news:

According to CNBC ‘Experts’ after this morning’s employment report, this week’s data indicate that the economy is in dire straits. Each ‘Expert’ on this morning’s panel tried to talk-over the others in being more pessimistic. If you heard the commentary, you would think our economy had had literally zero improvement since 2009 especially in in Personal Income growth. I am long beyond being shocked at the lack of basic analysis which has been prevalent in the financial industry, but the commentary this morning was particularly misinformed in my opinion.

Check out the supporting evidence and a great chart pack. He shows the strong relationship between employment, personal income, and vehicle sales. You will not see this anywhere else.

Stock Ideas

Biotech stocks. Here are six ways to profit from Clinton’s $132 billion tweet. I own several of the named stocks, including the recommendations by our go-to expert, John McCamant.

How should you balance your desire for yield with the risk of stocks? In the most recent installment of his excellent series, Chuck Carnevale considers the issue. As always he provides plenty of stock ideas with fine supporting analysis.

Too Much Ado about China

Jack Ma explains that U.S. investors over-react to China news.

The China Beige Book covers a wider range of companies and data than most sources you see in the news. The conclusion is also much more balanced.

“Those touting China’s sudden fragility are either exaggerating current problems or have entirely missed the slowdown of the past several years,” said China Beige Book, a U.S. research firm, in a report this week. It said China’s image might be “more thoroughly divorced from facts on the ground” than at any time since it began conducting surveys of the country’s economy five years ago.

The Value Investing Approach

Even if an investment method is proven over decades, there will be stretches where it seems not to work. When I first started our business, Felix’s dad out-performed Warren Buffet for a few years. I was reminded of this by Morgan Housel, who wrote this week about the relentless focus on one-year returns.

But why one-year returns? Why not 13 months, or two-and-a-half years? Or 5.21 years?

You should expect year-to-year stability in investing returns if there is something special about a year. But there’s not. A money manager is looking for exploitable opportunities, not all of which will fit neatly into a time period governed by the gravitational pull of a celestial ball of gas. Anyone using astrology to measure future returns is considered a lunatic, but almost everyone uses it to measure past returns.

Take the 50-year record of Warren Buffett, whose success virtually everyone agrees comes from more than luck.

Buffett has outperformed the S&P 500 by more than a million percentage points since he took over in 1964. But he underperformed the market in a third of all years — better than a coin toss but not much.

His partner Charlie Munger beat the market tenfold in thirteen years, but trailed in 1/3 of the years.

Eddy Elfenbein, a fellow value investor with a great record, notes that the value method has struggled for years. (I have some ideas about the reasons, but this is not the place).

Personal Finance

Professional investors and traders have been making Abnormal Returns a daily stop for over ten years. The average investor should make time (even if not able to read every day as I do) for a weekly trip on Wednesday. Tadas always has first-rate links for investors in this special edition. As always, there are several great links, but I especially liked this David Harrison article about why people do not save enough for retirement. If your employer is not offering a plan, you need to be proactive.

In addition, I really enjoyed this story about Tadas (thewaiterspad). You will too, including some great advice and good links. I strongly endorse his approach:

“You can’t block out all the noise,” Viskanta says, “you have to be much more of a conscious consumer.” Viskanta finds “an amalgam of stuff.” This diversity of information, he says, helps him figure out what’s important and what isn’t. The problem is that no amount of filtering can outsmart our reptilian brain.

Market Outlook

Goldman Sachs has six reasons to expect a rally. Corporate America is doing better than most think. The post cites some interesting data, including refutation of several common themes about worries.

Tom Lee’s bullish meter is at 10 for the near future, and he has been pretty accurate in recent years. Most people think this is crazy, but the reasons are very interesting. He sees seasonality reversing and a shift in former headwinds like the stronger dollar.

The pundits are out with various efforts to slice and dice YTD results to predict the fourth quarter. Widely popular was this CNBC analysis which suggested that a negative YTD led to a negative 4th quarter 47% of the time.

But maybe stocks outperform after weakness — (Bespoke via WSJ).

It was a very bad month and quarter. If you are willing to throw out 2008 (I am always suspicious of data that throws out best and worst cases) the odds of a rebound are 80%.

Watch out for Target Date Funds

Simple formulas based upon age provide inferior results (Market Watch). Who could have known? It is much better to adjust allocations based upon the relative attractiveness of various asset classes.

Final Thought

Understanding the increase in volatility begins by realizing that we are mostly returning to long-term normal levels after a long period of quiescence. Moves of 1% per day represent volatility of 16, close to normal. Trading has been thin during recent months, so that contributes to larger moves. Excessive fear is another factor.

Daily trading continues to track oil prices, as noted by many veteran market observers. I wrote last week that oil prices represented the most significant concurrent market indicator, starting a persistent trading dynamic. I am repeating this because it was dramatically underscored last week, and remains important both for traders and for investors:

- There is a piece of news, perhaps minor, perhaps totally bogus, and perhaps just speculative.

- The fastest traders and algorithms act instantly in the indicated direction, often using ETFs.

- Slower traders join in, going with the flow.

- Pundits impute major significance to the event, filling air time and media space.

- Readers and viewers join the party, probably on the wrong side and definitely too late to profit.

Rinse, lather, repeat.

I provided several examples, but oil prices are the most important.

The market is trading with a strong correlation to oil prices. Art Cashin mentions it daily and veteran observer Art Hogan says it has been a “lockstep” relationship for weeks. If you were using this indicator on an examination you would get an “F.” Prices include both supply and demand. Global demand has actually increased this year, even more than last year. It is not a sign of weakness. The trading works only because “everyone else” has the same illusion.

Here is a chart of crude oil prices on Friday, illustrating the late-morning turnaround.

Last week’s advice was also on target:

If you are a trader, like Felix, these are treacherous waters. You can see the early reaction, but the algorithms and many other traders will be faster than you are. Unless you think that the initial move is too small, you are too late to trade. I see too many traders who have excessive confidence and probably excessive size. If you are a short-term trader you should beware of getting too big with your positions.

If you are an investor, the prospects are much better. As long as you focus on the long run, irrational dips in prices provide opportunity.

Investors who are able to focus on what stocks are worth rather than the most recent headline or opinion have the most to gain from current trading.