Equity Outlook Fourth Quarter 2015

U.S. Large Cap Equities

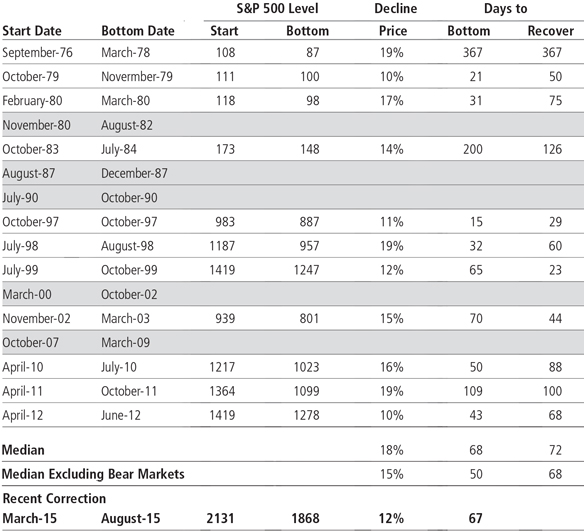

We upgraded our view of U.S. large cap equities to slightly overweight for the next twelve months. The S&P 500 registered its first correction since 2011, declining more than 10% from its high in May. The key question for investors today is whether the pullback represents a momentary pause in the current economic cycle, as in 2011, or anticipates something more serious, such as a global recession. In our view, the latter prospect is unlikely, given the resiliency of the U.S. economy and, importantly, broad policy commitment to cushion economic shocks. The Federal Reserve, in particular, is likely to be cautious in light of recent events and the absence of inflationary pressures as it assesses the timing and pace of any rate hikes.

Still, it bears noting that the past seven years have seen extraordinary gains in U.S. equities with a near absence of major (10%-15%) corrections. The recent swoon may be overdue, and actually healthy, as it creates more attractive valuations.

U.S. Equities: Corrections of 10% or More

Shading Indicates Bear Markets of 20% or More

Source: FactSet, Goldman Sachs. As of August 31, 2015.

Indexes are unmanaged and are not available for direct investment. Investing entails risks, including possible loss of principal. Past performance is no guarantee of future results.

Developed Market Non-U.S. Equities

Europe: The Committee as a whole remained at a slight overweight for Europe. Although growth and inflation forecasts for the region are subdued, the European Central Bank (ECB) stands ready to increase and/or lengthen its quantitative easing program as needed in support of its objectives. We anticipate that ECB stimulus will support European equities and maintain that there is more catch-up potential for the region from an economic recovery and earnings perspective.

Japan: Our view on Japanese equities moderated slightly from the third quarter. Japanese stocks are benefiting from a weak yen and reallocation of pension fund assets, but are threatened by a slowing Chinese economy. While we continue to believe that Japanese equities have upside potential, a contraction in second quarter GDP gives us concern about growth and the efficacy of Abenomics.

Emerging Markets Equities

China volatility, commodity weakness and dollar strength persist, creating headwinds for emerging markets equities, while corporate profitability remains under pressure. Against this backdrop we are maintaining our neutral view of emerging markets equities and believe selectivity from a regional/country and sector/company perspective remains paramount in today’s environment.

Brazil: With the country mired in recession, we have downgraded our view on Brazilian equities and further believe that the country may encounter meaningful risks with respect to its debt.

Russia: Russia has held up reasonably well in recent months compared to other emerging markets but Committee members remain cautious on the long-term outlook for the country’s equities due to a weak growth forecast, sizeable exposure to energy prices and the potential for ongoing geopolitical risk.

India: Thanks to some respectable policymaking and a solid fiscal position, India is hanging on to its position as a relative bright spot within our emerging markets outlook. The country, however, has not been immune to China volatility and the broader emerging markets equity pullback.

China: We have moderated our view on Chinese equities to neutral. In mid-August, the PBOC surprised investors by effectively devaluing the yuan relative to the U.S. dollar by nearly 2%, triggering a wave of volatility across global financial markets. Chinese equity markets experienced a broad pullback in response as investors evaluated whether the currency adjustment was reflective of a longer-term plan to create more open financial markets or part of a concerted effort to boost China’s export sectors and offset the country’s slowing economic growth trajectory.

We view the potential for a meaningfully slower China as a key risk. Even though the official growth rate for China is 7%, many view this figure as suspect, with other metrics including its manufacturing PMI telling a different story. The resources available to China’s policymakers, including room for additional interest rate cuts and $3.5 trillion in foreign exchange reserves, are considerable but we anticipate slower growth and ongoing volatility in the months ahead.

Master Limited Partnerships

We have upgraded our view on Master Limited Partnerships (MLPs) to a slightly above-normal return outlook. The sharp selloff in the energy sector has produced significant collateral damage, even among businesses like midstream pipeline operators with a less direct, long-term relationship to the price of crude oil.

Distributions by most pipeline operators have been unaffected, but prices are significantly lower, translating into attractive yields and meaningful discounts to historical valuations.

From a fundamental perspective, earnings and distributions from midstream MLPs continue to grow around 5% a year in many cases, providing a positive outlook on the security of distributions and the potential for continued growth.

MLPs: Spread Versus Treasury Suggests Yield Opportunity

Alerian MLP Index Yield vs U.S. 10-Year Treasury Yield

Basis Point Spread: December 31, 1995 – August 31, 2015

Source: www.alerian.com; www.federalreserve.gov.

Indexes are unmanaged and are not available for direct investment. Investing entails risks, including possible loss of principal. Past performance is no guarantee of future results.

About the Asset Allocation Committee

Neuberger Berman’s Asset Allocation Committee meets every quarter to poll its members on their outlook for the next 12 months on each of the asset classes noted. The panel covers the gamut of investments and markets, bringing together diverse industry knowledge, with an average of 24 years of experience.

This material is provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Information is obtained from sources deemed reliable, but there is no representation or warranty as to its accuracy, completeness or reliability. All information is current as of the date of this material and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole. Neuberger Berman products and services may not be available in all jurisdictions or to all client types. Investing entails risks, including possible loss of principal. Investments in hedge funds and private equity are speculative and involve a higher degree of risk than more traditional investments. Investments in hedge funds and private equity are intended for sophisticated investors only. Indexes are unmanaged and are not available for direct investment.Past performance is no guarantee of future results.

The views expressed herein are generally those of Neuberger Berman’s Asset Allocation Committee which comprises professionals across multiple disciplines, including equity and fixed income strategists and portfolio managers. The Asset Allocation Committee reviews and sets long-term asset allocation models, establishes preferred near-term tactical asset class allocations and, upon request, reviews asset allocations for large diversified mandates and makes client-specific asset allocation recommendations. The views and recommendations of the Asset Allocation Committee may not reflect the views of the firm as a whole and Neuberger Berman advisors and portfolio managers may recommend or take contrary positions to the views and recommendation of the Asset Allocation Committee. The Asset Allocation Committee views do not constitute a prediction or projection of future events or future market behavior. This material may include estimates, outlooks, projections and other “forward-looking statements.” Due to a variety of factors, actual events or market behavior may differ significantly from any views expressed.

A bond’s value may fluctuate based on interest rates, market conditions, credit quality and other factors. You may have a gain or a loss if you sell your bonds prior to maturity. Of course, bonds are subject to the credit risk of the issuer. If sold prior to maturity, municipal securities are subject to gain/losses based on the level of interest rates, market conditions and the credit quality of the issuer. Income may be subject to the alternative minimum tax (AMT) and/or state and local taxes, based on the investor’s state of residence. High-yield bonds, also known as “junk bonds,” are considered speculative and carry a greater risk of default than investment-grade bonds. Their market value tends to be more volatile than investment-grade bonds and may fluctuate based on interest rates, market conditions, credit quality, political events, currency devaluation and other factors. High Yield Bonds are not suitable for all investors and the risks of these bonds should be weighed against the potential rewards. Neither Neuberger Berman nor its employees provide tax or legal advice. You should contact a tax advisor regarding the suitability of tax-exempt investments in your portfolio. Government Bonds and Treasury Bills are backed by the full faith and credit of the United States Government as to the timely payment of principal and interest. Investing in the stocks of even the largest companies involves all the risks of stock market investing, including the risk that they may lose value due to overall market or economic conditions. Small- and mid-capitalization stocks are more vulnerable to financial risks and other risks than stocks of larger companies. They also trade less frequently and in lower volume than larger company stocks, so their market prices tend to be more volatile. Investing in foreign securities involves greater risks than investing in securities of U.S. issuers, including currency fluctuations, interest rates, potential political instability, restrictions on foreign investors, less regulation and less market liquidity. The sale or purchase of commodities is usually carried out through futures contracts or options on futures, which involve significant risks, such as volatility in price, high leverage and illiquidity.

This material is being issued on a limited basis through various global subsidiaries and affiliates of Neuberger Berman Group LLC. Please visit www.nb.com/disclosure-global-communications for the specific entities and jurisdictional limitations and restrictions.

© 2009-2015 Neuberger Berman LLC. | All rights reserved