US Equity and Economic Review For Sep. 28-Oct 2; The Bull Needs Stronger Earnings, Edition

This week’s economic news was mostly positive. Manufacturing is still expanding and consumers are still spending, especially on durable goods. But the stronger dollar and weaker international environment are clearly taking their toll, as the ISM is just barely in expansionary territory. The markets are in somewhat precarious shape as we enter earnings season; they remain expensive and therefore need to see topline revenue growth. Unfortunately, that doesn’t appear to be coming.

This article should be read in conjunction with the weekly bond market review.

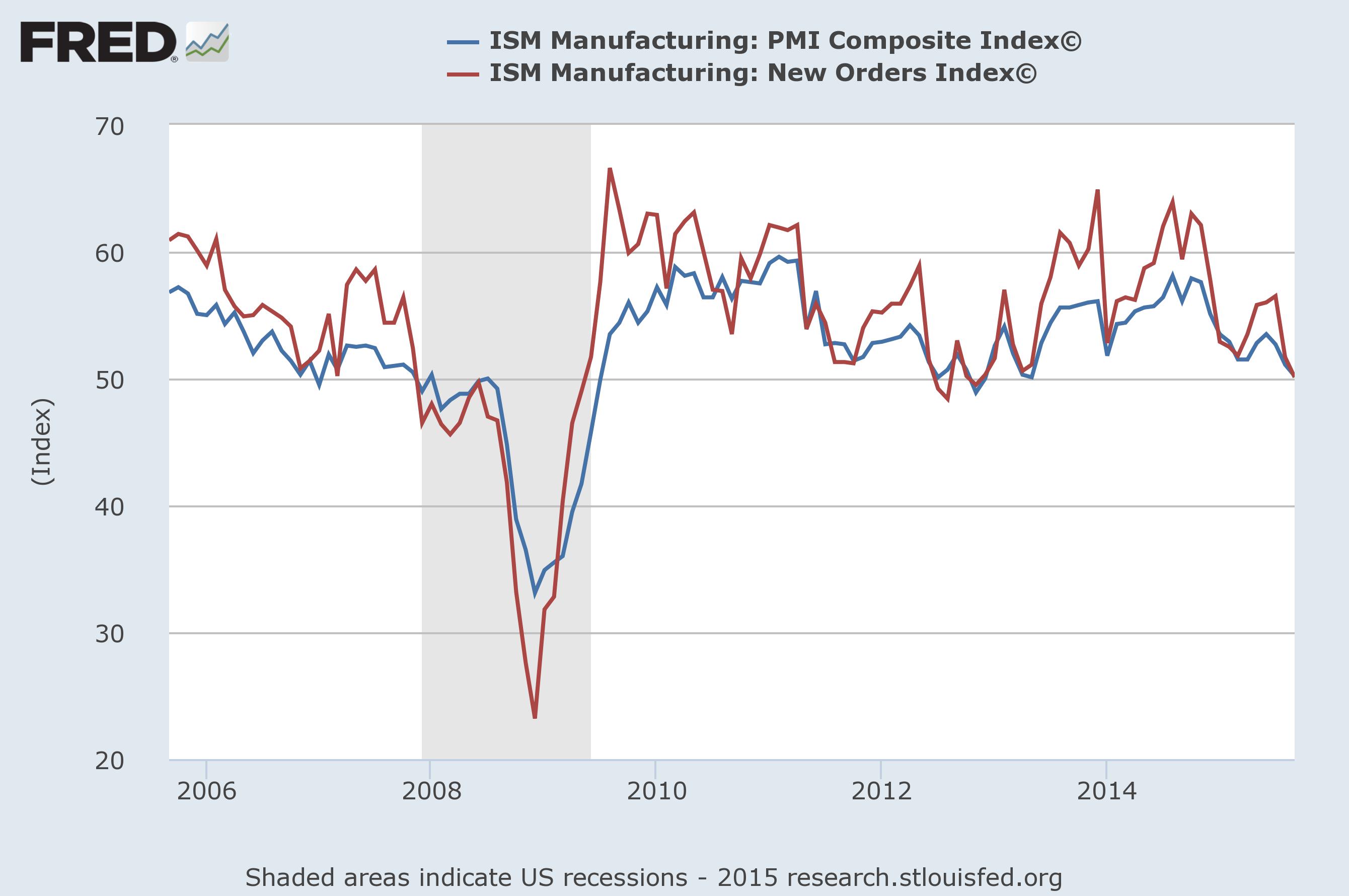

The ISM reported the latest manufacturing index at 50.2 – just barely positive. New orders were also just on this side of expansion at 50.1. Both numbers are trending lower since mid-2014:

Export orders contracted for the fourth consecutive month and only seven of eighteen industries expanded. And for the first time in several quarters, the anecdotal notes trended bearish:

- "Revenues and profits in our industry continue to [be] impacted by low crude and gas prices." (Petroleum & Coal Products)

- "North American business steady. International business trending bearish." (Chemical Products)

- "High value of dollar is affecting global procurement pricing."(Computer & Electronic Products)

- "Concerns about China downturn and its effect on our consumer confidence." (Fabricated Metal Products)

- "Overall business is slowing. Consumers are nervous. Not sure what is coming next." (Transportation Equipment)

- "Business is picking up." (Furniture & Related Products)

- "The orders from customers seem to be slowing a bit from the first part of the year. We have promises but not actual Purchase Order numbers." (Nonmetallic Mineral Products)

- "Sales revenue and profitability improving slowly. Getting close to 2015 budget/sales plan. Not seeing consistent trends up or down." (Electrical Equipment, Appliances & Components)

- "Continue to feel impact of oil and gas market slowdown. Aerospace demand has also been slower than expected. Consumer Electronics not robust." (Primary Metals)

- "Concern for AI [Avian Influenza] for poultry when bird migration begins." (Food, Beverage & Tobacco Products)

Overall, it appears China’s slowdown, the strong dollar and the negative impact of oil’s price drop are all negatively impacting durable good demand.

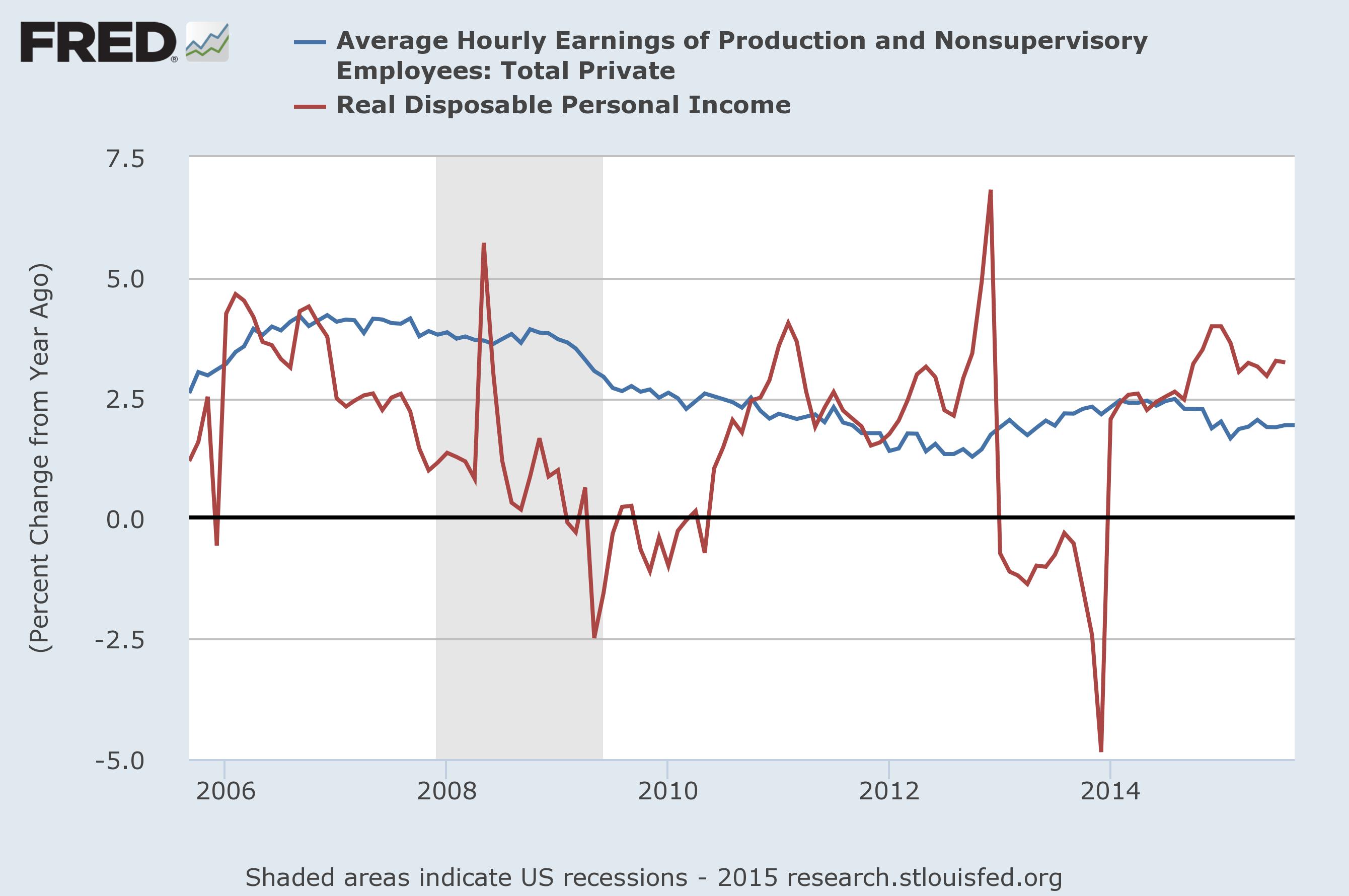

Consumer news was positive. The BEA reported real disposable personal income increased .3% while real PCEs were up .4%. DPI continues to increase slightly higher than 3% Y/Y. However, this measure includes many sources of income; the far more important average hourly earnings of non-supervisory employees are increasing below 2% Y/Y:

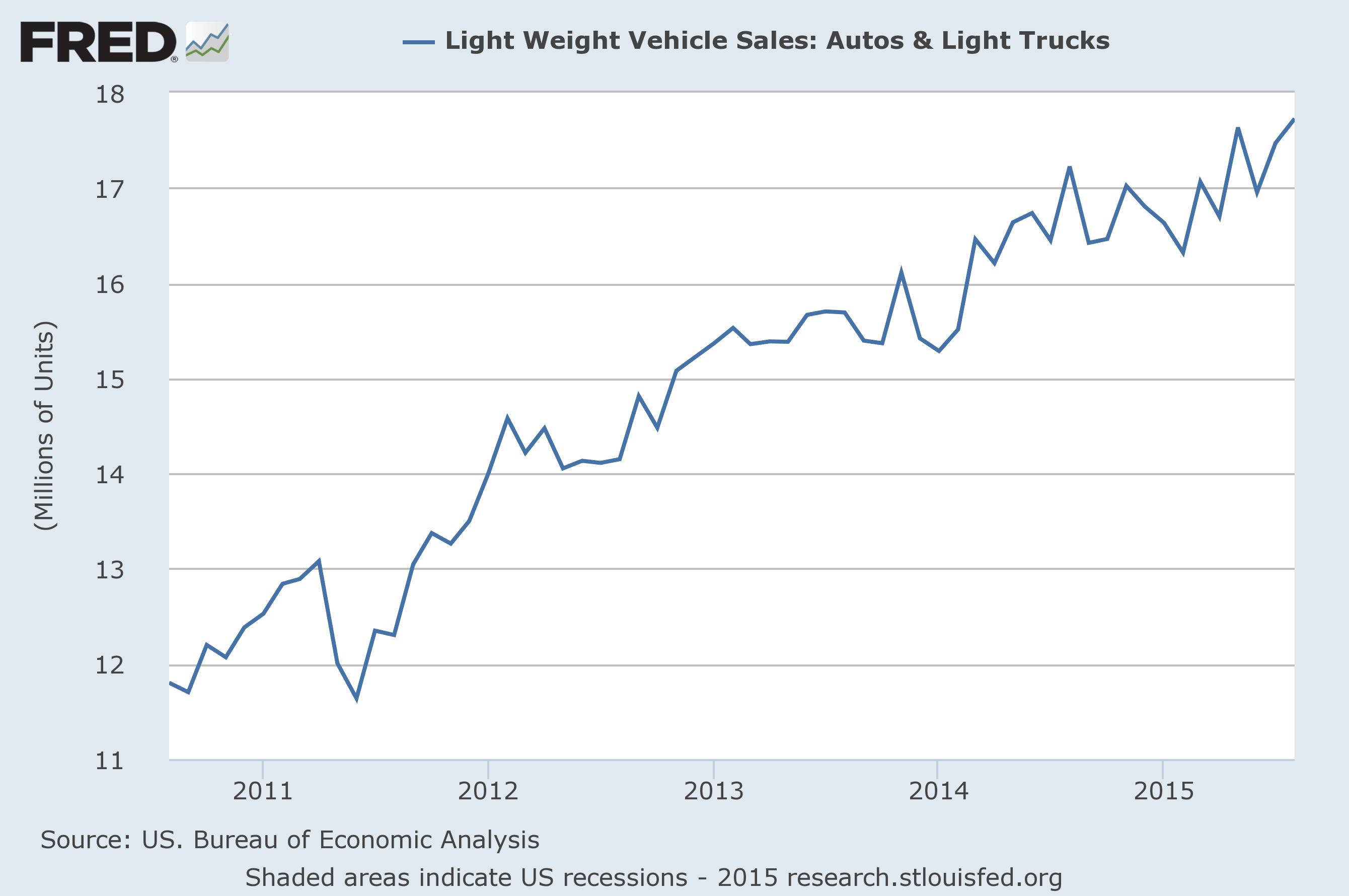

And auto and light truck sales increased smartly:

September was a blockbuster sales month for the U.S. auto industry — except at Volkswagen, where an emissions scandal forced the company to halt sales of most of its diesel-powered vehicles.

Strong Consumer demand, easy credit and generous incentives combined to fill dealer showrooms. The industry sold 1.44 million cars and light trucks last month, up 15.8 percent from a year ago.

This data point continues to increase at solid rates:

The employment report, which is covered in the weekly bond market review, was a big miss.

Economic Conclusion: the news this week was weakly positive. The strong dollar and Chinese slowdown are weighing on both manufacturing and employment. While income increased, the more important wage figure is doing so at a far lower level. Auto and light truck sales were the best news, as they indicate the consumer is willing to spend on expensive durable goods. This is a tacit admission of confidence.

Market Analysis

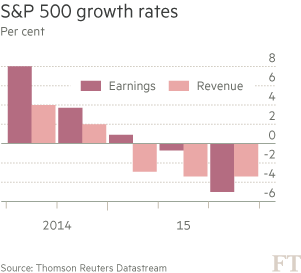

The market remains expensive. The current and forward PEs for the SPYs and QQQs are 20.75/20.52 and 16.05/17.65, respectively. As I’ve noted numerous times over the last few months, the markets are in desperate need of top-line revenue growth, which still appears elusive. Consider this graph from the Financial Times:

Both revenue and earnings growth are negative for the 1H15. And the third quarter is not looking promising. Thanks to weak inflation, companies have little pricing power, and therefore can’t meaningfully increase top-line revenue. This is leading to lower earnings guidance for all 2016.

Let’s look at the SPYs weekly chart to better understand the long-term situation:

Prices broke the near 4-year rally that started at the end of 2011. They’ve currently found support in the upper 180s/lower 190s. But the 10 week EMA is already below the 50 and the 20 week EMA is about to cross lower as well. And with prices below all three the trend is clearly lower. Weak momentum and price strength simply add fuel to the bear’s fire. On this chart, prices really want to move lower, with the 200 week EMA being the logical price target. Assuming that to be an accurate prediction, prices have another downward move of ~5%.