As China transitions from a manufacturing-driven economy to a consumer-led one, the Chinese investment universe has expanded. Historically, global investors have chosen to invest in Chinese equities via Hong Kong stock exchanges. But with China gradually opening its capital markets to global investors, and more Chinese enterprises successfully listing overseas, the investment options and opportunities have increased significantly. In this changing investment landscape, we are seeing a growing trend toward investors adopting an all-market approach to investing in China.

Offshore versus onshore

Unlike other large international stock markets, China’s equity markets trade on the mainland as well as abroad, each with separate share class names, different characteristics and varying levels of investor access. We believe it’s important for investors to be aware of these distinctions to understand the unique investment opportunity they offer.

-

Offshore Chinese equities are Chinese companies listed outside of China, which are fully accessible to international investors. This includes Hong Kong-listed share classes such as H-shares and red chips, privately owned Chinese companies, and companies listed in the US, London and Singapore. Recently, there has been an increase in the listings of companies in the US and Singapore, especially in the information technology (IT) sector, which has further broadened the investment opportunity set. The MSCI China Index is typically used to represent offshore Chinese equities.

- Onshore Chinese equities are domestic China A-shares that are listed on the mainland exchanges in Shanghai or Shenzhen. They are not fully accessible to international investors. However, global investors can invest in China A-shares via the Qualified Foreign Institutional Investor (QFII), the Renminbi QFII (RQFII) and the recently launched Shanghai-Hong Kong Connect programs.1 The Shanghai-Shenzhen Composite Index (CSI300) is the index that best represents onshore Chinese equities.

An all-market approach

An all-market approach seeks to take advantage of the unique structure of China’s equity markets and the distinct opportunities they offer by allocating across both offshore- and onshore-traded shares. Below, I discuss various characteristics of onshore and offshore Chinese equities:

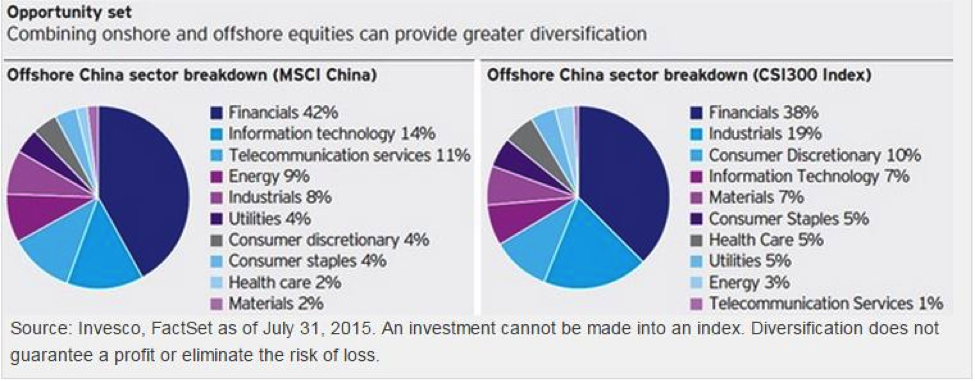

1. Increased sector diversification. By combining offshore and onshore equities, broader sector diversification of a Chinese equities portfolio is possible.

Offshore Chinese equities are primarily those of large, established Chinese companies that include leading public enterprises as well as some traditional Chinese conglomerates. In the MSCI China Index, the largest sector allocation in offshore Chinese equities is financials, followed by information technology (IT) and telecommunication services.

In contrast, onshore Chinese equities have a higher weighting in consumer-related companies than offshore markets. The three largest sectors in the Shanghai-Shenzhen Composite Index (CSI300 Index) are financials, industrials and consumer discretionary. While a large number of state-owned enterprises are listed on the mainland, an increasing number of privately owned companies are listing there as well.

2. Diverse selection of opportunities. Offshore markets are largely driven by global institutional investors, who tend to place more emphasis on fundamentals and relative valuations. As a result, these markets have tended to exhibit lower volatility and more stable returns relative to onshore Chinese markets, helping to mitigate some of the risks associated with investing in Chinese equities.

Domestic retail investors conduct the vast majority of daily trading volume on the mainland’s markets. Additionally, onshore markets are at an earlier stage of development than their offshore counterparts. These influences have made onshore markets driven more by momentum and sentiment, rather than fundamentals. Experienced investors can seek chances to capitalize on price inefficiencies that may arise in onshore markets.

3. An impressive market scale. Today, China’s equity markets rank among the world’s largest. Hong Kong’s market (which includes offshore China shares) is the fifth largest equity market behind the UK. China’s onshore equity market is now the second largest in the world behind the US on a total-market-capitalization basis and the third largest when measured in terms of its free-float market cap (the size of readily available shares). On a cash-turnover basis, it’s over three times larger than the Asia Pacific ex-China region as well as Japan’s Topix or the US’s S&P 500 Index. Given the size of both the Hong Kong and China markets on a global scale, liquidity is of little concern when dealing in both offshore and onshore Chinese equity markets.2

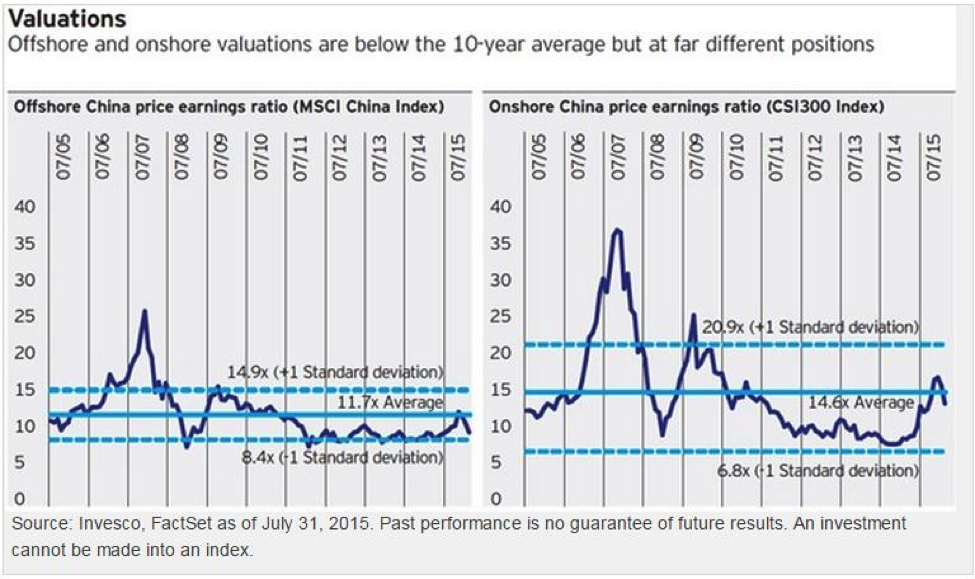

4. Attractive valuations. As measured by price-earnings (PE) ratio, valuations on the MSCI China Index and the CSI300 Index are currently below their 10-year averages.

Hong King-listed offshore Chinese equities were trading near their historical lows, at 9.6x 12-month forward PE, with a price-to-book ratio (PBR) at 1.3x (as of July 31, 2015).3 Overseas-listed companies, such as American depositary receipts (ADRs), are more growth-oriented, in sectors such as internet and health care, and tend to have relatively higher valuations.

Like their offshore counterparts, onshore equities have also been trading at historically cheap levels. Even after the dramatic correction this summer, the CSI300 Index was at 13.3x 12-month forward PE, with PBR at 1.9x (as of July 31, 2015).3 Onshore equities tend to trade at a premium to offshore Chinese equities and typically exhibit higher market volatility, often overshooting on both the upside and downside.

A better balance

I believe the ongoing evolution of China’s investment landscape will continue to sustain the movement toward an all-market approach. Over time, as China opens its markets and the onshore investor base broadens, I expect a better balance in onshore and offshore Chinese equities to emerge.

1 Onshore Chinese equities also include B-shares listed on the Shanghai Stock Exchange in US dollars and Shenzhen Stock Exchange in Hong Kong dollars.

2 Source: Bloomberg as of April 22, 2015. Topix=Tokyo Stock Exchange Tokyo Price Index and S&P 500=Standard & Poor’s 500 Index.

3 Source: I/B/E/S, FactSet, Goldman Sachs

Important information

The MSCI China Index is an unmanaged index considered representative of Chinese stocks.

The Shanghai Shenzhen Composite Index (CSI 300) is a free-floated index that consists of 300 A-share stocks listed on the Shanghai or Shenzhen Stock Exchanges.

The Topix (Tokyo Stock Price Index) is a free-float-adjusted market-capitalization-weighted index measuring the performance of large-cap stocks listed on the Tokyo Stock Exchange.

Price-earnings (P/E) ratio, also called multiple, measures a stock’s valuation by dividing its share price by its earnings per share.

Price-to-book (P/B) ratio is the market price of a stock divided by the book value per share.

Standard deviation measures a portfolio’s range of total returns and identifies the spread of a portfolio’s short-term fluctuations.

American depositary receipt (ADR) is a negotiable certificate issued by a US financial institution representing shares of a foreign stock that is traded on a US exchange and denominated in US dollars.

The S&P 500® Index is an unmanaged index considered representative of the US stock market.

The Shanghai Hong Kong Stock Connect is a cross-boundary investment platform that connects the Shanghai Stock Exchange and Hong Kong Stock Exchange. Under the program, investors in each market are able to trade shares on the other market using local brokers and clearinghouses. It was launched in November 2014.

RQFII stands for RMB Qualified Foreign Institutional Investor. RQFII is a policy initiative of the Mainland authorities which allow qualified holders of RQFII quota to raise funds in Hong Kong and channel such funds to directly invest into Mainland securities available in the Mainland securities market.

Investments in companies located or operating in Greater China are subject to the following risks: nationalization, expropriation, or confiscation of property, difficulty in obtaining and/or enforcing judgments, alteration or discontinuation of economic reforms, military conflicts, and China’s dependency on the economies of other Asian countries, many of which are developing countries.

In general, stock values fluctuate, sometimes widely, in response to activities specific to the company as well as general market, economic and political conditions.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2015 Invesco Ltd. All rights reserved.

An all-market approach to investing in China by Invesco Blog