“The situation is desperate but not serious.”

Old Viennese saying

The ceteris paribus enigma

One of the questions I am most often confronted with goes as follows:

Why is the extraordinarily and persistently low interest rate environment not great news? Why is it not a once-in-a-lifetime opportunity to get all the wheels spinning again? Put another way, why do I think very low interest rates for an extended period of time can actually do quite a lot of damage?

It is a tricky question to which there is no simple answer. Low interest rates, ceteris paribus, obviously boost overall economic activity, and those who are so critical of our central bankers for their relentless pursuit of easy money, should probably think again before they have another go. Imagine what economic activity would have been like, had rates not been kept extraordinarily low. The economy post 2008 is without precedent, and an economy without precedent requires a monetary policy that is also without precedent.

The sharp reader will now argue that I am contradicting myself. One moment I suggest that low interest rates for an extended period of time can do a lot of damage. The next I scold those who criticize our central bankers for keeping interest rates low. How come? The answer lies in the use of the term ‘ceteris paribus’. The point is, other things are not equal.

More often than not, the critics point at the ongoing paltry GDP growth rate to prove their point. My point is different. Low interest rates for an extended period of time don’t damage economic growth directly, but they cause damage in a multiple of other ways – a point almost universally missed by the critics. That is what this month’s Absolute Return Letter is all about.

Credit growth has driven GDP growth over the years

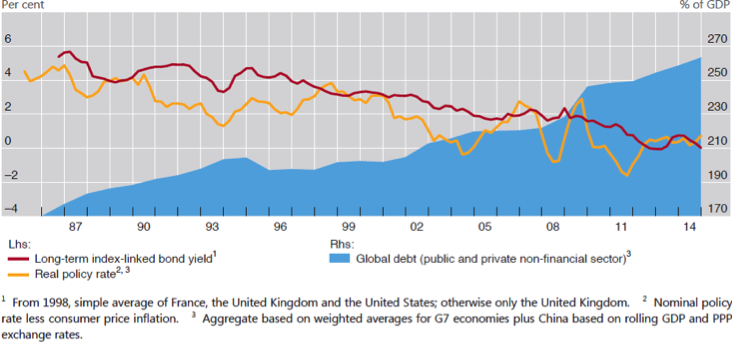

Let’s begin by looking at how the low interest rate environment post 2008 has affected total borrowing. When the Bank for International Settlements (the central bank of central banks) published its 2014-15 annual report a few months ago, they answered that very question (chart 1). As you can see, total debt (public and private) continues to rise almost as if 2008 never happened.

Chart 1: Debt soars as interest rates sink

Source: BIS 85th Annual Report 2014-15

This leads me to the obvious question – is debt creation actually good or bad news as far as economic growth is concerned? Few topics divide the investment community more than this question. When reading other commentators, it appears that the fundamentalists amongst us are of the opinion that any increase in debt from current levels is going to come back and haunt us eventually. Debt is akin to evil, or so they seem to think.

On the other side you will find those who accept that some debt creation is actually good for economic growth but only up to a point. Let’s call those who subscribe to that view the pragmatists. Going back to the question again – does debt creation actually create economic growth? - allow me to revisit a chart I used in last month’s Absolute Return Letter. Produced by Deutsche Bank in 2008, it demonstrates a very clear link between credit growth and C+I, which is a proxy for private sector demand (chart 2).

Chart 2: Credit growth’s impact on domestic demand in the United States

Source: Deutsche Bank

C+I is part of the well-known formula GDP=G+C+I+(X-M)1. The fact that the growth in credit correlates very tightly with C+I implies that credit growth also correlates quite highly with GDP. Looking at chart 2 again, it is therefore fair to conclude that the pragmatists have the upper hand in the war of words with the fundamentalists – or had, at least until 2008.

Let’s go back to the fundamentalists’ point of view for a moment. How can they possibly argue that debt creation will ultimately prove very damaging? After all, it is hard to argue against the findings of chart 2. The argument put forward by their camp is that ‘when interest rates normalise, we will be proven right’.

Assuming that a ‘normalisation’ of interest rates to levels we experienced before the great recession would imply a return of economic growth and inflation to those same pre-2008 levels, as regular readers of the Absolute Return Letter will know, I don’t think there is a cat in hell’s chance that we will return to those sorts of levels of growth anytime soon. For that very reason, neither will interest rates.

For the record, U.S. interest rates will probably rise more than they will here in Europe, but they will stay comparatively – and surprisingly – low everywhere. Hence the biggest risk is therefore not that interest rates suddenly take off. Rather the biggest risk is that interest rates stay very low. Let me explain.

Issue # 1:

Low interest rates lead to lower productivity

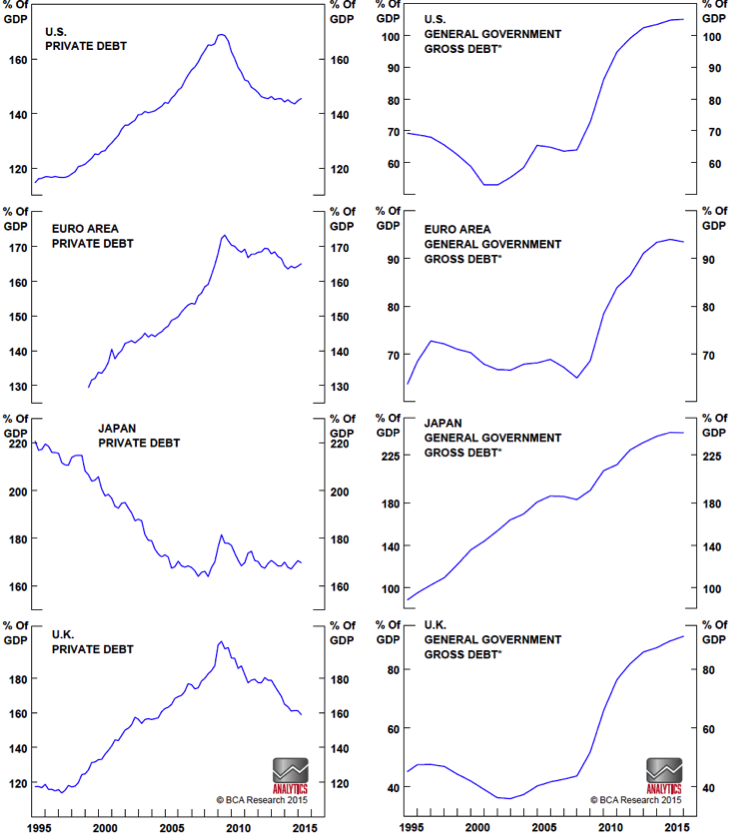

My journey begins by digging one level deeper than chart 1 did. Who has actually taken on all the additional debt since 2008? The good news in this context is that private debt, although it is still comparatively high in places, has actually fallen meaningfully since the peak of the financial crisis (chart 3). Public debt, meanwhile, has not, as is obvious when looking at the right hand side of chart 3.

Chart 3: Public debt and private debt are on two very different paths

Source: BCA Research

This leads to my first conclusion of the day. As virtually all the net debt accumulation of recent years is public debt, the debt service burden (i.e. future taxes) could rise significantly, should interest rates begin to move higher. The alternative, interest rates to stay very low, is not an attractive option either for reasons that will become obvious in a moment or two. You are damned if you do and damned if you don’t.

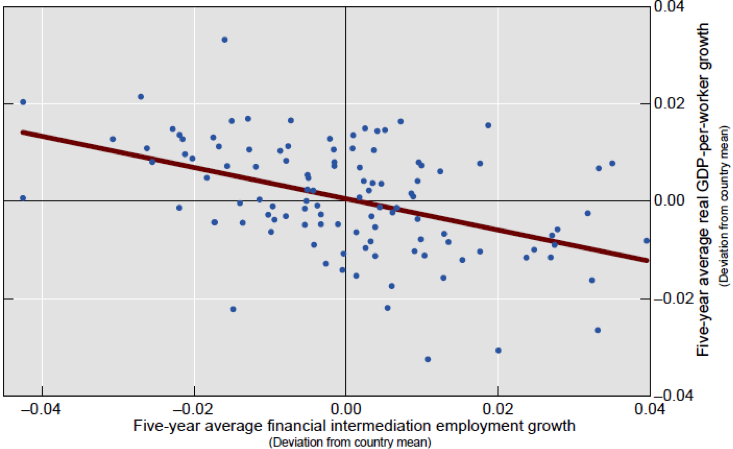

However, before I go any further, let me point at one of the more interesting findings of BIS in their ongoing research into the causes of the great recession2. They have found that the growth of a country’s financial system holds back overall economic growth because a growing financial sector is a drag on productivity growth (chart 4).

Chart 4: Financial sector growth v. productivity growth

Source: Working Paper 490, BIS

Why is that? It is only a guess, but one could argue that the financial sector competes with the rest of the economy for resources (human as well as capital), and strong growth in the relatively well paid financial sector drains other parts of the economy of talented people.

BIS actually goes one step further in its conclusions. Not only does strong growth in the financial sector act as a drag on overall economic growth, credit booms do the same, and that is because credit booms harm the more R&D intensive engines of economic growth.

This is a poorly understood side effect of low interest rates combined with strong credit growth, and could become a real issue for some countries – in particular the Anglo-Saxon ones, where the financial sector continues to grow.

Issue # 2:

Low interest rates lead to more risk taking

Investors (and people in general) not only take on more debt when the debt service burden is low; they also take more risk, potentially leading to further asset bubbles. Investors looking for income chase higher yielding opportunities, as safer bonds no longer offer the income required, and capital appreciation seeking investors allocate more to riskier asset classes such as equities. The net result? Potentially a lot more risk in many portfolios than people are aware of and would be comfortable with, did they know and/or fully understand.

Obviously this only becomes an issue if markets run into serious headwinds but, in that respect, I subscribe to Sod’s Law3. If anything can go wrong, it will, and that would certainly include the present situation in financial markets. Having said that, I don’t at all expect a repeat of 2008, but less can also be quite damaging, and there is no question that the risk profile is out of whack in many portfolios at present.

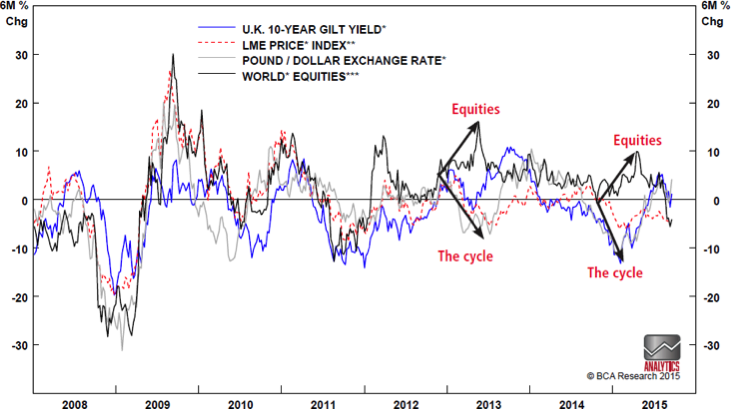

I have written extensively about the risk-on, risk-off environment, which has prevailed since 2008, but here is another angle. What’s the link between UK gilts, metal prices and £/$? Not a lot at first glance, but they have all followed the same cycle since 2008. All three have proven to be risk-on, risk-off assets (chart 5).

Chart 5: Gilts, metal prices and £/$ all follow the same cycle

Source: BCA Research

Now, you would be forgiven for asking: So what is the link? If I told you that German exports have followed exactly the same cycle (chart not shown here), the answer becomes obvious: It is global economic growth, stupid.

Chart 6: Equities are different than other risk-on assets

Source: BCA Research

Now the punchline - if it is indeed global economic growth that is the common denominator, one would expect global equities to track the same cycle, and they have – except for early 2013 when the Fed launched QE3 ($), and earlier this year when the ECB launched QE1 (€) – see chart 6.

In other words, central bank action has had the effect of de-linking equities from the global growth cycle, as equity investors have chosen to blatantly ignore the fall in global trade in favour of more risk-taking at the back of accommodating central banks. Risk-on, risk-off has miraculously turned into risk-on, risk-on. “Don’t fight the Fed”, as they say, and equity investors have obviously chosen not to.

Issue # 3:

The big, white elephant (aka the pension industry)

And now to the big white elephant – the pension industry. My story begins in the UK. The Office for National Statistics announced back in 2012 that total UK pension liabilities amounted to just over £7 trillion, with almost £5 trillion being unfunded (chart 7). To the best of my knowledge no follow-up announcements have been made since, but I could be wrong.

Chart 7: UK pension liabilities in 2012

Source: Office for National Statistics, Mercer

Unfunded pension liabilities can rise as a result of falling asset prices, or they can rise if interest rates fall or people live longer than ‘planned’. The key in this context is the ultra-low interest rates, which are used to discount future liabilities back to a present value; i.e. should interest rates fall, the industry has to use a lower discount factor.

I have no way to verify if this is correct or not, but well-informed sources tell me that UK unfunded pension liabilities are fast approaching £10 trillion, or over five times GDP. Put another way, £10 trillion translate into approx. £375,000 per UK household in future pension liabilities; a whopping number that makes pretty much all other problems look like a walk in the park. The fact that most unfunded pension liabilities in the UK are linked to state pensions only make matters worse; there is in reality only one place to find the money – the taxpayer’s pockets.

The pension industry divides itself up between defined benefit (DB) schemes and defined contribution (DC) schemes. It is in DB schemes that the massive fall in interest rates has caused the almost incomprehensible rise in unfunded liabilities, but that doesn’t imply that one is right and the other one wrong. The two types of schemes differ in terms of who assumes the investment risk, and the big drop in interest rates is going to hurt DB schemes (and hence the member indirectly), whereas in DC schemes it will hurt the member directly.

If you are one of our many non-UK readers, don’t assume that your country is necessarily any better off, although the mix between DB and DC schemes varies greatly from country to country (chart 8). I should also emphasize that some countries have managed their liabilities much better than the U.K. has. You can therefore not assume that, just because your country has a large percentage of DB schemes, you are in trouble. One would have to go into much more detail than I am doing here.

Chart 8: The split between DB and DC schemes in various countries

Source: Towers Watson

Having said that, in the U.S., where DB schemes do not account for a particularly large part of the pensions industry, federal unfunded pension liabilities now exceed $127 trillion (it is not a misprint - see the story here.) One can only imagine what that implies for the U.S. tax payer.

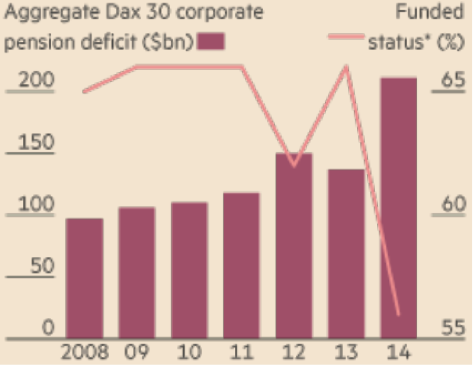

German pension funds’ funded status, already low after years of falling interest rates, took another dive in 2014, and German companies have been forced to set aside billions of euros for their struggling pension funds (chart 9).

Chart 9: German unfunded pension liabilities

Source: Financial Times, Mercer

Some countries have begun to take action. Sweden, Denmark and the Netherlands have all permitted the local pension industry to use a fixed discount factor of 4.2%, and in the U.S. the regulator now allows the industry to use the average rate over the last 25 years when discounting future liabilities back to a present value.

Although initiatives such as these have the effect of reducing the present value of future liabilities and thus the amount of unfunded liabilities overall, they do absolutely nothing in terms of addressing the core of the problem – low expected returns on financial assets in general and low interest rates in particular.

Why returns will remain low for many years to come

I have written extensively in recent years about why returns on financial assets are going to remain low for many years to come, and do not intend to repeat myself; hence the next few paragraphs are no more than a summary of my previous findings.

First and foremost, returns are going to remain subdued because GDP growth will stay low for a long time to come. Demographic factors, productivity factors and mountains of debt in the majority of countries all point in the same direction, and that is towards below average economic growth.

The most structural of those factors – demographics – will remain a negative for the U.S. economy for another 10-15 years, whilst economic growth in the euro zone and Japan will be negatively affected by demographics until at least 2050. This does not imply that there cannot be extraordinarily good years every now and then, but the average growth rate will almost certainly be low, causing interest rates to stay relatively low for a lot longer than most expect and corporate earnings to disappoint as well.

In this context, I note Angela Merkel’s recent announcement that Germany will probably take up towards 800,000 refugees next year. Do not underestimate her. It is obviously a very generous gesture, but she is not stupid and is fully aware that Germany will need millions of new workers in Germany’s many factories in the years to come – people they won’t have unless something changes.

Conclusion

So – to summarise my findings:

Interest rates are likely to stay comparatively low for a very long time to come, and low rates will:

- damage GDP growth because of the effect low productivity has on it;

- tempt investors to take undue risks;

- magnify the risk of a total collapse of our pension system.

The last issue will, to most people, have by far the biggest impact. Given the magnitude of unfunded pension liabilities in the Anglo-Saxon world, something will simply have to give. Political leaders in most countries prefer not to talk openly about it, which is (sort of) understandable, given that it is not the most obvious vote winner one can think of.

However, the fact that David Cameron appointed one of the leading UK experts on pensions – and one with no previous ties to the Conservative Party - as a pension minister when his government was reshuffled earlier this year, is an indication that they are finally beginning to take the problem seriously.

So what could happen? An across-the-board haircut? An extension of the retirement age? A mandatory conversion of DB schemes to less risky DC schemes? (Less risky – at least from the employer’s point of view.) Something else? I have no idea, but something is almost certain to happen. Otherwise entire countries could be forced to default on their pension liabilities, which is in nobody’s interest.

Changing the discount factor is only the beginning of something much bigger to come but, quite frankly, changing the discount factor is akin to financial engineering anyway. No fundamental problems are resolved this way. The best of all worlds would obviously be a material rise in interest rates without a corresponding rise in the debt service burden, and without it having a negative impact on equity prices. One can only dream.

Niels C. Jensen

1 October 2015

©Absolute Return Partners LLP 2015. Registered in England No. OC303480. Authorised and Regulated by the Financial Conduct Authority. Registered Office: 16 Water Lane, Richmond, Surrey, TW9 1TJ, UK.

Important Notice

This material has been prepared by Absolute Return Partners LLP (ARP). ARP is authorised and regulated by the Financial Conduct Authority in the United Kingdom. It is provided for information purposes, is intended for your use only and does not constitute an invitation or offer to subscribe for or purchase any of the products or services mentioned. The information provided is not intended to provide a sufficient basis on which to make an investment decision. Information and opinions presented in this material have been obtained or derived from sources believed by ARP to be reliable, but ARP makes no representation as to their accuracy or completeness. ARP accepts no liability for any loss arising from the use of this material. The results referred to in this document are not a guide to the future performance of ARP. The value of investments can go down as well as up and the implementation of the approach described does not guarantee positive performance. Any reference to potential asset allocation and potential returns do not represent and should not be interpreted as projections.

Absolute Return Partners

Absolute Return Partners LLP is a London based client-driven, alternative investment boutique. We provide independent asset management and investment advisory services globally to institutional investors.

We are a company with a simple mission – delivering superior risk-adjusted returns to our clients. We believe that we can achieve this through a disciplined risk management approach and an investment process based on our open architecture platform.

Our focus is strictly on absolute returns and our thinking, product development, asset allocation and portfolio construction are all driven by a series of long-term macro themes, some of which we express in the Absolute Return Letter.

We have eliminated all conflicts of interest with our transparent business model and we offer flexible solutions, tailored to match specific needs.

We are authorised and regulated by the Financial Conduct Authority in the UK.

Visit www.arpinvestments.com to learn more about us.

Absolute Return Letter contributors:

|

Niels C. Jensen |

Tel +44 20 8939 2901 |

|

|

Gerard Ifill-Williams |

Tel +44 20 8939 2902 |

|

|

Nick Rees |

Tel +44 20 8939 2903 |

|

|

Tricia Ward |

Tel +44 20 8939 2906 |

|

|

Alison Major Lépine |

Tel: +44 20 8939 2910 |

1 G=Government Spending; C=Consumption; I=Investments; X=Exports; M=Imports.

2 See for example BIS WP 490, ‘Why does financial sector growth crowd out real economic growth?’

3 For our American readers, Sod’s Law is the British equivalent of Murphy’s Law.