Last season, the Green Bay Packers started the season 1-2. Some fans panicked, to put it mildly. Conspiracy theories surfaced for why Green Bay’s quarterback Aaron Rodgers didn’t seem to be playing well and most people formed an opinion on who was to blame. It was at this point, following the team’s second loss, Rodgers found himself being peppered with questions from reporters attempting to figure out what was “wrong” with him and/or the team. Rodgers’ response was, “R…E…L…A…X.” The Green Bay Packers subsequently won 11 out of their next 13 games and Rodgers ended the season with 38 touchdowns, only 5 interceptions and was voted the NFL’s most valuable player. For Rodgers, with disappointment came questions because people thought something must be wrong. But, with success came silence.

Patience

I started this blog with the reference above to illustrate that, by and large, we are an impatient society. And, in my opinion, it is only getting worse. We need immediate gratification. When something isn’t working, we want to get rid of it. Disappointment must be rationalized because many of us cannot deal with the thought of being average, or (you may need to sit down), being below average! That simply can’t be. We’re too smart to be below average. We need better. We need results now.

Why do I bring this up? It’s not simply to state that impatience is bad. Or, that we shouldn’t strive for better. To the contrary, in many circumstances I believe impatience is good. It is part of what drives ambition, motivation and a host of other positive behaviors. However, I also believe impatience is the Achilles heel of successful long-term investing. This is especially true for investors that stray from a “true” passive investing strategy in search of better results (if you’re unsure what I mean by “true” passive investing strategy, please refer to my last two blog posts (Part 1 and Part 2). And for investors that stray from passive investments and passive investing, many will find themselves in the world of active investments, which I’ll touch on in today’s post.

As a reminder from my first post, an active investment is often associated with investment products whose manager(s) attempts to beat a stated market index through various means, such as through individual stock selection or by investment in specific sectors or industries. It is a style of management where active decisions are made based on a manager’s forecasts for individual companies, sectors and industries and/or other factors.

Bad Behavior

Based on my experience, selecting individual active investments is littered with land mines and a host of potential pitfalls. As I mentioned above, I believe the largest pitfall for long-term investment success is the lack of patience. This is why I have commonly viewed the “active vs. passive” debate not as a debate between individual product types (active or passive), but rather a debate between “patience and passive.” To illustrate my point, we need look no further than a study from Vanguard. The table below displays average returns, the time-weighted return, of a universe (all individual products categorized by style) of active products compared to the estimated Investor return in the same universe. Needless to say, the difference (shown in olive green) is eye-opening!

Investor Return

Why is this? What causes such a large performance gap? This is largely caused by impatience and impatience’s nasty sibling, “recency bias” (the belief that what has occurred most recently will continue to occur moving forward). Combined, these behaviors typically result in the desire for investors to chase good performance. Investors don’t want to be below average, even in the short run. They need better. They need to invest in products that have delivered great investment returns on both an absolute and relative basis. The only issue? Investment returns for active products, relative to a benchmark, are anything but consistent!

Lack of Consistency

If investment results for an active product were consistently better over the long term, then something wouldn’t be right. Either the benchmark selected or the benchmark construction would be wrong, or the investment strategy would be too good to be true. While not a perfect example, this is one of the main reasons Harry Markopolos filed a complaint with the Boston office of the SEC in 2000 identifying Bernie Madoff as a fraud (nearly eight years prior to Madoff’s Ponzi scheme falling apart). Madoff’s hedge fund returns were too consistent, and consistently good, to be actual returns, especially when factoring in normal market volatility. This example isn’t meant to infer that consistency of investment results immediately equals fraud; rather the point is that the performance of active investments is rarely consistently in excess of their designated benchmark, especially over shorter term periods. All active investments will periodically underperform their designated benchmark over shorter term timeframes.

Despite this fact, when an investment performs exceedingly well, investor money commonly rushes in because everyone wants to invest in above average investment products. Investors are uncomfortable with mediocrity – even in the short run! We want results now, not five years from now. Unfortunately, what commonly occurs is that as the previous winning product’s performance recedes (on a relative basis), investors become frustrated, determine that something must be wrong and sell the product to reinvest in another winner. Rinse and repeat.

Behavioral Biases Affect Everyone

It’s important to pause here and note that when I refer to investors, I am not simply talking about individual investors. Through my experience, I’ve also seen this type of behavior from investment boards of large institutional plans, from other financial professionals and among people of every age group and educational background. In fact this behavior may actually be worse among investment boards and financial professionals than it is among individual investors. This may be because selling a “loser” is significantly easier than having to talk about it with a disappointed client. Plus, it’s much easier to find an issue in something that has fallen short of expectations (remember the reporters’ questions to Aaron Rodgers after the team’s 1-2 start?) than it is when something is performing above expectations. So, an underperforming investment may be sold and replaced with an outperforming investment. Out of sight, out of mind.

Selling, Not Just Buying, Must Be Discussed

While the reasons for a sale may not always be nefarious, such as the practice of “window dressing” – making a portfolio look better than it actually has been through the purchase of strong performers and the sale of weak performers right before a performance reporting period, ignorance is not a valid excuse. There may be a perfectly well researched reason for why an investment product is struggling and should be sold. The fact is not all underperforming investments should be owned indefinitely, but not all underperformers should be sold either. As a fee paying client, you simply need to know why. It’s your money. You deserve a well-thought out explanation.

Misplaced Motivations

Similar issues may plague asset managers. However, the end result is the same: investor disappointment and frustration. Some asset managers’ (I by no means, mean all) after garnering significant assets in a product, motivations may change. Protection of the assets that are invested in the product may become more central to the investment process than generating attractive long-term investment returns. In essence, they may become fearful that if they underperform, assets that are invested in the product may leave. So, they may become closet indexers; managers that charge an active investment management fee, but largely deliver benchmark-like returns. Needless to say, investors need to be on the look-out for these types of managers, because closet indexers have become much more prevalent, while true active managers have become a relatively rare breed.

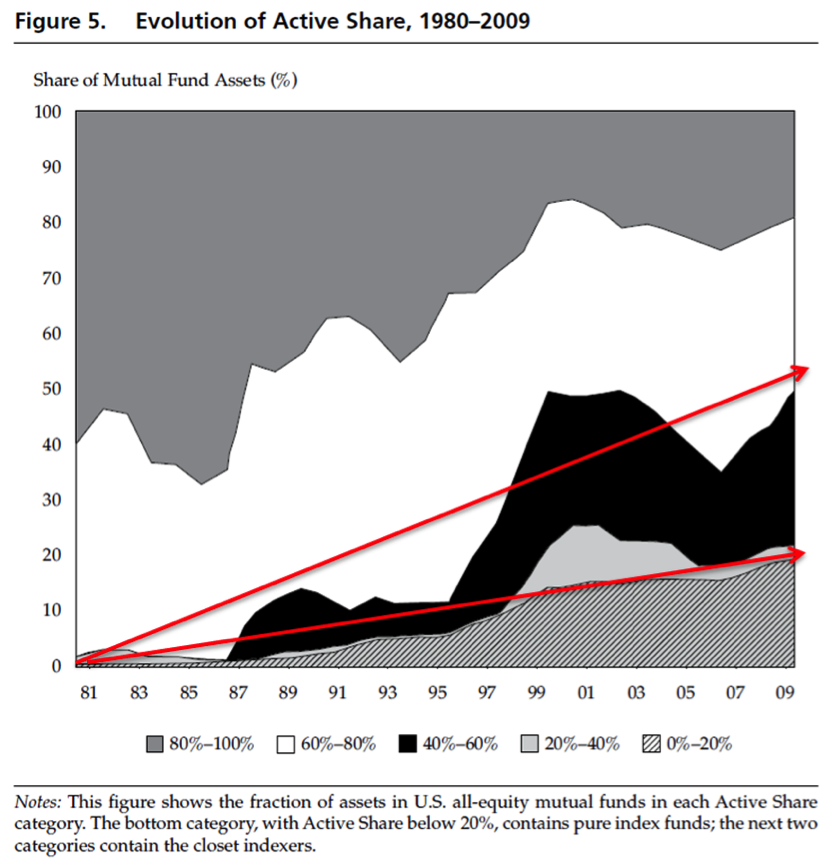

To illustrate how this practice has increased, the chart below from Financial Analysts Journal 2013 article “Active Share and Mutual Fund Performance” by Antti Petajisto, shows that the percentage of investment products that could be labeled as closet indexers, note the area approximately between the two red arrows, has grown substantially over the past 30 years.

How Active is Your Active Manager?

The chart above also leads me into the next part of the discussion; determining how active an active manager really is. This is an important concept because if you’re paying for active management, then you should actually be getting active management. And by definition, the vast majority of active managers are attempting to beat a designated benchmark. If that’s true, then the active manager should at least be somewhat different than the benchmark, correct? Active share is a statistic that attempts to measure the difference.

Active share was introduced in September, 2009 in the Review of Financial Studies in a paper authored by Antii Petajisto and Martijn Cremers titled, “How Active is Your Fund Manager? A New Measure That Predicts Performance.” Active share essentially measures how different an investment product is relative to the benchmark the product compares itself to. The calculation is relatively straightforward; it is the sum of the absolute value of all overweights and underweights in a portfolio compared to its benchmark, divided by 2. So, an active share of 100% would mean that there are no positions in the portfolio that are also in the benchmark, while an active share of 0% would mean that the portfolio is a pure index option or the product has completely replicated the benchmark.

This measure has been embraced by active asset managers as a way to demonstrate value-add. Overall, I believe it is a very useful measure, but that’s not to say the study doesn’t have its own warts. For instance, high active share, which was found to be a good predictor of future results, is much easier to accomplish when the benchmark a product is measured against has a large number of individual holdings. As an example, a small cap equity manager whose benchmark is the Russell 2000 Index can differentiate itself much more easily than a large cap equity product that benchmarks itself to the S&P 500 because the number of holdings in the small cap index is significantly greater. I raise this issue (and I will write a more detailed post in the future about active share) to illustrate that while active share is indeed a useful measure, it is not the only answer needed to identify active investment products that can outperform a given benchmark over a complete market cycle. High active share does not necessarily equal active investment manager success. As I’ve stated many times, there is no easy answer when it comes to long-term investment success. Active share is just one calculation/measure in a vast mosaic of information that must be measured and understood. In fact, in my opinion, high active share should be the byproduct of a robust manager research and due diligence process. What it should not be is the beginning and the end of the manager research and selection process.

Selecting Active Investments

How is someone actually supposed to find active investments that have the ability to outperform their designated benchmark over a complete market cycle when there are roughly 31,000 open-end mutual funds (this total includes multiple share classes for investments) and another 12,000 separate account strategies and collective investment trusts? Unfortunately, there is no secret formula. And there isn’t a magical, proprietary algorithm that sifts through the manager universe and spits out the best future performer. In my opinion, one of the only ways to achieve consistent success is to follow a very detail-oriented, in-depth manager selection process that includes a stringent review of all materials from an asset manager about the product that is being reviewed, discussions with the portfolio manager(s) and the investment team, a review of historical holdings and characteristics of the product and a review and validation of many other key portfolio statistics like costs, average holding period and turnover.

If you, or your financial representative, cannot conduct this level of research and analysis, then an easier option would be to use passive investments and follow a passive investment strategy. There is nothing wrong with this decision. However, if you believe markets are inefficient and some managers have the ability to outperform their designated benchmark over a complete market cycle, then at a minimum, make sure that you’re prepared to stick with the active manager chosen for the long-term. The same can be said if you hire a financial representative to select active investments for you. Again, I cannot reiterate this enough, make sure the individual has a sound investment selection process, educate yourself on that process, and then make sure they consistently do what they say they would do.

While I will not go through the entire research and investment process we follow for selecting individual managers at our firm, what I will tell you is to be keenly focused on minimizing fees wherever possible. For mutual funds this means no load (sales load on the front end or deferred load) and no 12b-1 fees. And make sure the manager doesn’t trade a lot (relatively low turnover); trading costs are not reflected in a mutual fund’s expense ratio, but are very much reflected in its performance results.

Conclusion

Investments in actively managed products requires an investor to exercise patience, avoid recency bias, have a relatively long investment horizon, thoroughly research and understand the investment chosen, or understand the investment process of the individual you have hired to select your investments, make sure the investment chosen is truly active and minimize fees wherever possible. Obviously, abiding by these requirements will not guarantee investment success, but at least you will start with a better foundation than most investors.

I’ll explore active investing as it relates to total portfolio management in my next, and final, post on active vs. passive.

Charles J. Batchelor is Director of Investment Research for Cleary Gull