International Economic Week in Review: The Commodity Super-Cycle Explained, Edition

Despite recent financial turmoil, no one has provided a concise explanation of the commodity super-cycle, one of the primary macro-economic forces causing recent volatility. That is, until now. In a September 21 speech, Bank of Canada Governor Stephen Poloz offered the following explanation:”

Because Canada has been endowed with such a wide variety of resources, we’ve had to learn how to deal with large swings in their prices. I don’t just mean the usual high degree of volatility common among many raw materials. I’m also referring to the long-term swings in prices that are often called “super cycles.” What’s important to remember is that these long-term swings are driven by the fundamental economic laws of supply and demand, as well as the continuous technological progress that can affect both output and consumption.

The pattern is familiar. A large and persistent increase in demand leads to sustained upward pressure on resource prices over a number of years. The higher prices act as an incentive to boost supply, and companies act by, for example, investing in new capacity and finding methods to increase efficiency. While high prices can certainly spur research and development, technological progress has been a constant theme in natural resource industries. Such advances uncover ways to raise output and lower production costs. And it’s because of this progress that inflation-adjusted commodity prices have generally been trending lower for 200 years.

The investments that lead to increased output can take years, if not decades, to complete. But, over time, the higher output generated by those investments combines with stabilizing demand to bring about a period of downward pressure on prices. Faced with lower prices, companies may scale back investment and production. Ultimately, the lower prices will encourage demand, and the reduced investment will crimp future supply, leading to higher prices. And producers will ride the price cycle all over again.

The latest cycle began in the early 2000s, when Chinese raw material demand sharply increased. This chart of the DBCs – which track the complete commodities market – shows the net impact of increased Chinese demand:

By early 2008, the entire index spiked to then record highs. Increased PRC demand led to massive increases in global fixed capital investment, typified by the Australian economy:

Australian capital spending increased 8x in a little over ten years. But due to these projects immense size, it takes years for the new production to come online. And the project’s high cost means companies are loathe to leave the capacity idle after the project is completed. But Poloz also noted that just as new capacity ramps up, demand begins to wane. This is where we are now in the “super-cycle:” supply is increasing and demand is decreasing -- a confluence of events that explains why commodity prices are declining across the board. This, in turn, means producer prices are very low, eventually leading to deflationary price pressures.

For the third consecutive week, a leading organization downgraded its Chinese growth outlook. This time, it was the Asian Development Bank, which reported:

In an update of its flagship annual economic publication, Asian Development Outlook 2015, ADB trimmed its GDP growth forecast for PRC to 6.8% for 2015 and 6.7% in 2016. In its March report, it projected growth of 7.2% for 2015 and 7.0% for 2016. The revisions reflect growth setbacks due to decelerating investment growth and weak exports.

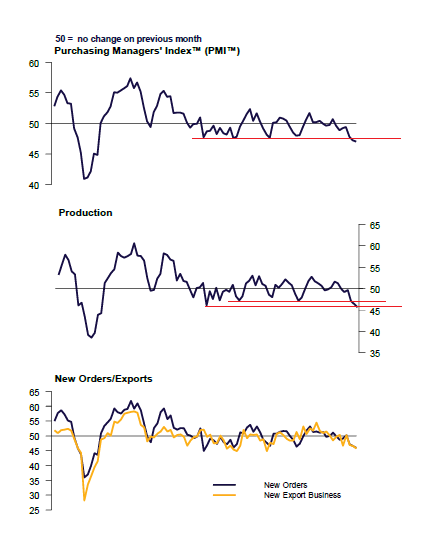

There is nothing surprising in the statement; the bank’s analysis falls squarely in line with that of other Asian analysts. Other news from China was mixed. According to the Chinese Beige Book, talk of the country’s economic slowdown is greatly exaggerated. This report noted services – which account for over half of Chinese economic activity – continue to grow, more than off-setting manufacturing losses. Other analysts such as David Rosenberg recently made this observation. But the latest Markit Chinese manufacturing numbers were the weakest in 78 months. And the report’s graphs paint a very ugly picture of the sector:

Two other news stories highlighted potential economic problems. First, China continues to tap its foreign reserves at an accelerated rate. While the situation is hardly dire, the increased rate of consumption indicates cost of the PBOC’s yuan defense efforts is increasing. Second, the central government will inject capital into a second struggling, state-owned equipment maker. It appears China is embracing the “too big to fail” scenario. At some point, this policy could not only become costly, but it could potentially prevent much needed market discipline from occurring.

In a recent speech to EU authorities, Mario Draghi offered the following assessment of the EU economy:

Turning to the first topic, let me give you an overview of the economic developments since the last hearing in June. Over the summer, industrial production and other indicators of economic activity showed signs of resilience. At the same time, the macroeconomic environment has become more challenging. Our September macroeconomic projections indicated a weaker economic recovery and a slower increase in inflation rates than we had expected earlier this year. The inflation rate will remain close to zero in the very near term, before rising again towards the end of the year. It will take somewhat longer than previously anticipated for it to converge back to and stabilise around levels that we consider sufficiently close to 2%.

Slowing growth in emerging market economies, a stronger euro and the fall in oil prices and in commodity prices more generally are the main causes for these developments. As a result, renewed downside risks to the outlook for growth and inflation have emerged. For many of these changes, it is too early to judge with sufficient confidence whether they will cause lasting slippage from the trajectory that we initially expected inflation to follow when we decided to expand our asset purchase programme in January. More time is needed to determine in particular whether the loss of growth momentum in emerging markets is of a temporary or permanent nature and to assess the driving forces behind the drop in the international price of commodities and behind the recent episodes of severe financial turbulence. We will therefore monitor closely all relevant incoming information and its impact on the outlook for price stability.

Draghi’s comments are eerily reminiscent of the last Fed policy statement, especially his focus on emerging markets. Draghi spends more time discussing inflation, focusing not only on weak oil prices but the potential long-term impact of weak inflation on macro-economic policy. Like other central banks, it appears the ECB’s inflation model is out-of-sync with market reality. Inflation continues to surprise ECB policy makers in a very negative way.

Other EU news, however, was positive. The latest Markit numbers were the best in four years, with a 53.9 composite reading. Manufacturing was 52 while services was 54. German and French numbers were also encouraging: their respective composite readings were 54.3 and 51.4. And French manufacturing posted a positive 51.9 readings. Finally, loan growth continued to recover, posting a 1% Y/Y increase.

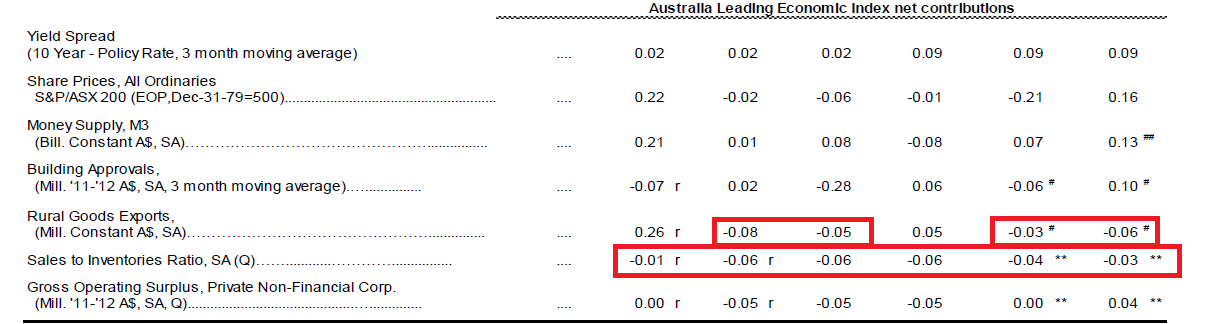

The Conference Board released Australia’s leading and coincident indicators. The LEIs increased for the first time in five months. The following table of itemized LEI components illustrates a fundamental problem:

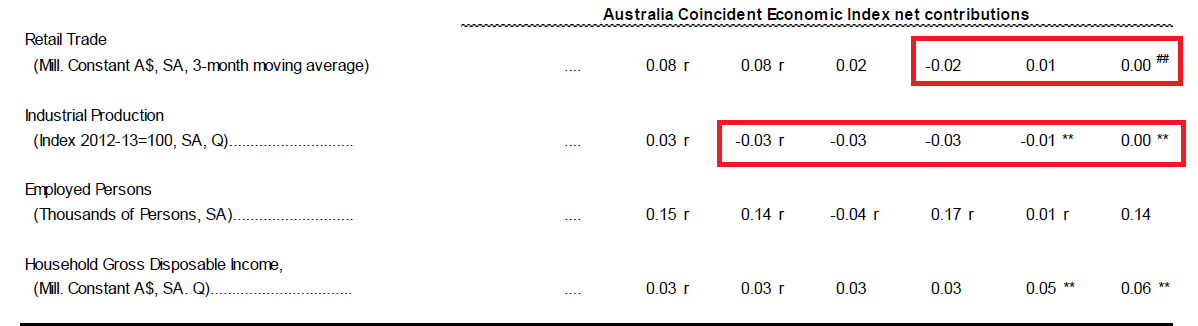

The financial LEIs (interest rates, stock prices and money supply) mostly increased over the last six months while the industrial LEIs (exports and sales/inventory ratios) are mostly negative. Ideally, the financial LEIs lead industrial. For example, the RBA lowers interest rates, increasing money supply, which then translates into more loans, leading to higher business profits. The above data, however, shows no industrial impact from better financial conditions. The coincident indicators also show a concerning situation:

The best retail trade contribution over the last three months was .01 while industrial production decreased for the last five consecutive months. In contrast, contributions from employment growth were strong in 4 of the last 6 months, leading to consistent income growth. Like the LEIs, the CEIs contain a data disconnect: higher wages aren’t translating into higher consumption. Overall, these data points show an economy that, while growing, has problems.

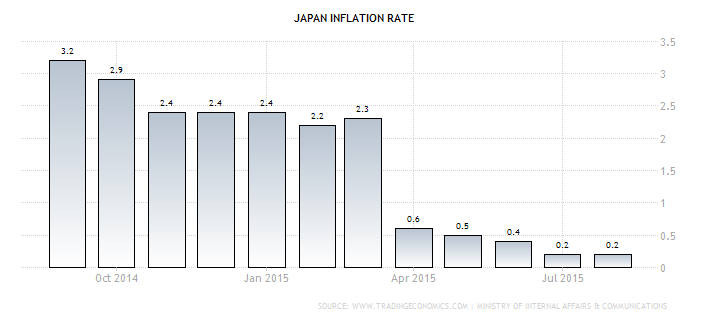

Finally, Japanese CPI increased a paltry .2% Y/Y:

As this graph shows, Japan has the same problem as other developed markets: borderline deflation. This increases pressure on Prime Minister Abe and the BOJ to do, well, something.

This is the third consecutive week where the tone of news releases, speeches and analysis has turned slightly negative. It started with the “surprise” Citigroup release three weeks ago, where they argued Chinese problems increased the possibility of a global recession to over 50%. Until then, analysts were waiting for someone to dip their toe in the water; since that announcement, it seems negative sentiment has increased. This shouldn’t be surprising. Since oil’s price drop a year ago, central banks have been arguing inflation will return to “normal” levels in their respective “intermediate” term. Unfortunately, the length of the intermediate term continues to increase. This continued rejiggering of inflation projections highlights fundamental problems with central bank inflation models, and potentially, macro-economic policy making apparatuses.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis