SUMMARY

- Goals-based asset allocation seeks to align our total portfolio, including financial and nonfinancial assets, with our personal goals and our human way of thinking about risk.

- The framework combines attributes of modern portfolio theory and behavioral finance in a common-sense manner, and is extremely flexible at the individual level.

- Focusing the investor, and the portfolio, on meeting the investor's short- and long-term goals should reduce the tendency toward counterproductive reactions to market volatility.

- This approach may be especially effective in the current environment of financial repression, where market valuations are intentionally distorted for policy purposes.

Introduction: Rethinking theory and framework

The wealth management industry, as is true of many industries today, is experiencing rapid change on several fronts. The vehicles used to deliver investment products are evolving, with new varieties of “alternative” mutual funds and a greater diversity of ETFs, including new forms of actively managed ETFs. The relationship between wealth managers and their clients is also evolving, as legacy transaction-based arrangements shift to fee-based ones. Perhaps most significant of all, capital market theory, the body of knowledge that attempts to explain the workings of the market itself, is also evolving, from one that held that markets are mostly efficient and should, thus, primarily be approached by investors passively to one that recognizes enduring structural and behavioral aberrations.

We will focus in this paper on this third area of change and will discuss how to incorporate some of these behavioral concepts in an investment program. Behavioral finance has evolved into a generally accepted, if not quite unified, body of research that acknowledges that we all are human and at times irrational in an economic sense in our investment decisions. Rather than trying to alter human nature, many wealth managers are now designing asset allocation frameworks to deal with these traits structurally. Instead of being market-driven in focus, these approaches are driven by the individual investor’s financial goals and attempt to use the financial markets to best meet those goals. This is an important shift of focus – from the primacy of the market to the primacy of each individual's goals. These goals-based asset allocation frameworks (GBAA) typically have two main attributes that differentiate them from conventional asset allocation approaches based on Modern Portfolio Theory (MPT): They directly incorporate nonfinancial and illiquid assets, including human capital, into the mix, and they seek to satisfy, rather than combat, the economically 'inefficient' goals that many investors have. This second point is a key distinction – these programs are designed to meet the investor’s goals on the investor's terms, as opposed to those of a completely rational economic actor.

If it's not difficult enough dealing with multiple crosscurrents of change all at once, we also find ourselves, six years after the Great Financial Crisis (GFC), in a seemingly endless environment of financial repression – an unprecedented intervention into global capital markets by monetary authorities both here and abroad. This has been a deliberate effort to drive down risk premiums and raise valuations across asset classes in an attempt to offset the deflationary aspects of the end of a multidecade global credit cycle. To say that this complicates life for investors and investment managers is a gross understatement. No one can know how far this will go, how long it will last or how it will end.

Our intention in this paper is to address, at a fairly high level, the concept and implementation of GBAA in light of the current environment of financial repression. We feel that this context needs to be considered today in any discussion of goals-based frameworks, which produce somewhat misshapen allocations relative to conventional ones. Financial repression, in turn, distorts market valuations. Our goal here is, thus, to come to terms with a misshapen allocation implemented in a market of distorted valuations.

Aligning portfolios with preferences

Much of what we are discussing here may be standard in a very high-net-worth financial planning context, although the nomenclature likely varies across practitioners. In its most comprehensive form, a financial plan is both personalized and complex, as it aims to incorporate client risk tolerance, current and future income needs, tax management, estate planning and other specific goals. What we are concerned with here is a more generalized approach primarily in the realm of risk management – a framework that can work for a cross section of wealthy investors, while still being flexible enough to incorporate the unique aspects pertaining to each individual or family.

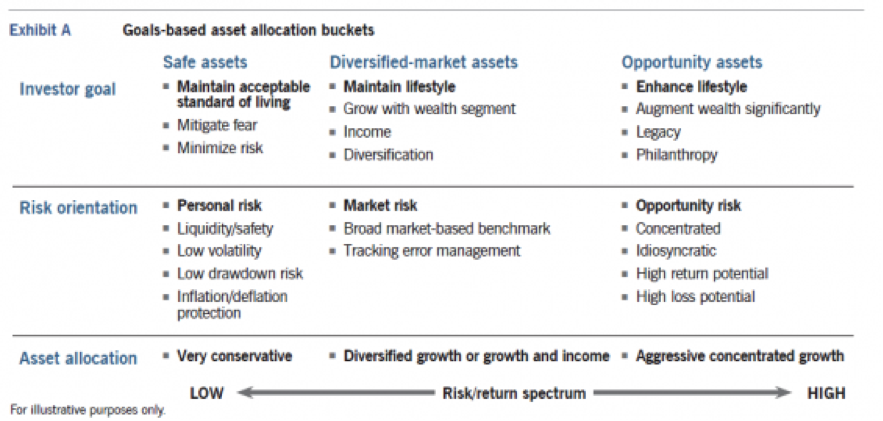

As mentioned above, goals-based allocation frameworks have two primary defining characteristics – incorporating nonfinancial and illiquid assets into the mix, and structuring the mix in a behaviorally sensitive fashion. The latter is manifested in the segmentation of the assets, typically into three main risk buckets, as depicted in Exhibit A: A safe bucket where the objective is to preserve purchasing power; one or more diversified buckets where the objective is to perform in line with, or above, the market on a risk-adjusted basis; and, finally, an undiversified, high-risk bucket that has the potential for significant wealth enhancement. For simplicity's sake, we will call these the safe, the diversified-market, and the opportunity buckets. Other practitioners have used different terms – such as personal, market and aspirational, or liquid, longevity and legacy – to describe similar risk bucketing concepts.

The rationale for including nonfinancial and illiquid assets in the mix, and assigning them to the correct buckets, is straightforward. These assets are often significant in size and have unique risk characteristics that should be factored into the overall portfolio mix. The main assets we are considering here would include primary and secondary homes, as well as investment real estate, concentrated stock or options positions (perhaps incentive-based and not yet fully vested), ownership of private businesses and human capital, especially for professionals. If one is a lawyer, a doctor, a corporate executive, a professional athlete, an entrepreneur, a hedge fund manager or one of many other possibilities, a significant portion of one’s wealth is the present value of that earnings stream. Furthermore, the riskiness of that stream and the factors that impact it will vary greatly by occupation; its portfolio weight will also change significantly over time as other assets are acquired and fewer working years remain. All this needs to be considered and appropriately accounted for in our framework.1

The behavioral rationale for subdividing the portfolio into three main pieces rests on common sense as well as the findings of Prospect Theory. Common sense tells us that we all have a hierarchy of financial goals, from basic standard-of-living goals to higher aspirational goals – to achieve things for ourselves, our families or our communities that will require greater financial resources. These goals, whether we explicitly recognize them or not, will likely have a big impact on our investing behavior. Prospect Theory, which documents how people typically make decisions involving risk, attempts to codify some of this behavior. It was derived largely through empirical observation several decades ago by Daniel Kahneman, who won the Nobel Prize in Economics for his efforts.1

Among the key findings of Prospect Theory is that people tend to focus more on gains and losses than on ending wealth level or status. In other words, we care more that we have just lost or gained, say, $500K than that our ending net worth is $5MM. Furthermore, we tend to be risk-averse with respect to gains in situations of high probability, and risk-seeking with respect to gains in situations of low probability. What this means is that, despite our understanding of mathematical probabilities, we nevertheless perceive additional value in both certainty (e.g., insurance) and also in possibility (e.g., lottery tickets). In other words, we like a safe bet and, somewhat in contradiction, we also like a long shot.

For example, Kahneman did simple experiments and found that when people were given the choice of receiving, say, $3,000 with a 90% probability or $6,000 with a 45% probability, the vast majority chose the highly certain $3,000 option. On the other hand, when given the choice between a 1% chance of $6,000 or a 2% chance of $3,000, again two choices with the same expected value, a significant majority in this case chose the longer-shot chance of the larger payout.

While Prospect Theory only documents these preferences and does not, as far as we know, attempt to explain them, they seem to reflect the basic human traits of fear and greed, and our desire both for safety and upside. We buy insurance because we fear loss and desire a certain amount of safety, and we buy lottery tickets, or invest in a startup or risky stocks, because we dream of financial success. We mentally account for these goals and embed them in our investment behavior whether we realize it or not. Unfortunately, our inherent fear and greed, combined with our excessive focus on gains and losses, will tend to work against our long-term investment success. As has been documented by Dalbar, among others, the actual returns that investors earn over time are far below market returns because too often we sell out of markets at the bottom, or buy into markets near the top. This behavior demonstrates that a single market-oriented portfolio does not adequately fulfill our hierarchy of needs; furthermore, our efforts to make it do so often result in counterproductive activity.

The goals-based framework is designed to better align our financial accounts with our mental accounts, and our portfolio components with our multiple goals, so that we will stick with our investment plan no matter what happens in the markets. Thus, instead of conflicting with our natural way of thinking about risk, or forcing it to change, this framework adopts it in a disciplined way to help us satisfy our behavioral preferences, avoid more damaging behavioral mistakes, and ultimately achieve our financial and personal goals.

1 See Appendix for further materials.

Structuring a goals-based allocation

The basic process for structuring a goals-based portfolio need not be overly complicated, although meeting other objectives such as income generation and tax management can add layers to consider. Since we are trying to fit liquid financial portfolio components around illiquid assets, it makes sense to start with the illiquid assets and assign them first to the correct buckets. Then a determination needs to be made of the appropriate relative size of each bucket, based on the individual’s circumstances and preferences. Finally, each bucket is augmented with the right mix of liquid financial assets, built around the illiquid ones, to achieve the goal of each bucket. In order to do any of this, however, we need to first clearly define and understand the objectives of each bucket.

Our first bucket, the safe bucket, is meant to deal with our fear. The intent is to provide a security layer of assets that retain their purchasing power under a wide range of scenarios and are sufficient to maintain a minimum living standard. Thus, the objective is to earn at least a zero real return, and the relevant benchmark is the rate of inflation. This is a much easier task in normal financial markets when cash yields tend to track inflation than it is in the financially repressed environment of today, with negative real yields. There are a number of illiquid assets that typically fit here, depending on an individual’s age and circumstances. A primary residence, a steady earnings stream from a stable profession (doctor, lawyer, corporate manager etc.) prior to retirement and defined benefit pension income after retirement would all fit here. Insurance assets and annuities would also likely go here. Around these are built a combination of low-volatility and low principal risk income-producing assets, and some alternative inflation-sensitive assets in addition to the residence. Low-volatility absolute return strategies, with limited drawdown risk, could also be appropriate for a portion of this bucket.

The diversified-market bucket is the closest in this framework to a conventional asset allocation model, and is likely the one with the fewest illiquid assets. This piece is designed to meet or exceed market returns on a risk-adjusted basis, and the benchmark is likely a blend of stocks and bonds, perhaps with either a growth tilt or income tilt depending on an individual’s circumstances. While this bucket may lend itself to partial passive management, it can also accommodate creative active management approaches, including smart/strategic beta exposures. In addition, "liquid alternatives" designed to provide diversification and risk mitigation, as well as alpha, would fit here. Low-leverage investment property might also be a type of less liquid "alternative" that fits here.

The third component of our framework, the opportunity piece, is the least straightforward and most adaptable part of this framework. It is designed to accommodate the illiquid, nondiversified, high-risk/high-return assets that provide an individual's best chance for significantly augmenting wealth. Given its unique characteristics, this piece defies benchmarking. These assets, when they exist, are typically related to the individual’s career and have significant upside potential, at least in the mind of the individual. Examples would include ownership interest in a private company, concentrated stock or options positions in a public company employer and perhaps highly leveraged investment real estate. The future earnings of a range of people in make-or-break professions, such as athletes, performers, artists, investors and entrepreneurs would also fit here, as would bonuses and incentive compensation for professionals.

A common characteristic of third-bucket assets is that the individual believes the assets are leveraged to career success; in other words, there exists at least a mental "optionality" here, meaning a payoff structure with upside convexity, like a call option. This is obvious in many situations (private businesses, lucrative careers), but less so in others. For example, a concentrated position in a public company may be unduly risky for unaffiliated investors, but may be justified for an insider with a positive view, and perhaps better information, about the company’s prospects and his own prospects within the company. If the company succeeds and the insider succeeds within the company, there is upside leverage. This might be considered irrational behavior in an MPT context, whereas it represents an important wealth opportunity for the individual in a behavioral finance context.

It is no surprise that this third bucket will likely change the most over time, in size and composition, as an individual's age and wealth advance. In cases where the existing assets have grown quite large relative to an individual's entire portfolio, some hedging or reconfiguration of these assets, or moving a portion into the diversified bucket, may be desirable, depending on total wealth level. Concentrated or idiosyncratic assets may at some point be replaced or diversified with other high-risk/high-return assets; or, if an investor is content with the wealth status he has attained, this bucket can be eliminated entirely. For wealthy investors who have divested their unique assets (sold a company, ended a career) yet still aspire to a higher wealth status, it may be possible to assemble a portfolio of assets with high return potential such as hedge funds, private equity or venture capital. The message here is that this is a highly personalized allocation, both in size and composition, and it will change over time.

The process for weighting the respective pieces in this framework is perhaps the most nuanced aspect of the framework, as it rests on the investor's circumstances, especially age, family situation, existing wealth level relative to wealth goals, risk preferences and projected future spending needs to the extent they can be anticipated. This structure, though, should at least facilitate arriving at a suitable mix via an iterative process of stress/scenario testing. This could include setting a minimum wealth threshold, factoring in spending needs over some intermediate horizon and allocating so that it is virtually impossible to drop below it.

It is worth noting that alternative frameworks are more problematic when it comes to setting overall risk parameters. Conventional mean variance asset allocation produces an efficient frontier and asks the investor to choose a spot along it – a difficult task, with little context for the investor’s decision. Frameworks that are more time-structured, such as personal liability-driven schemes that try to align assets with spending needs over multiple horizons, leave us with a different, and equally difficult, set of questions (e.g., how big is your 10- to 15-year spending bucket?). More importantly, neither of these alternative frameworks satisfies our behavioral preferences – our desire for both safety and possibility – nearly as effectively as the GBAA framework. We believe the GBAA framework is the least difficult puzzle to solve, primarily because it is explicitly constructed in pieces the investor both understands and cares about.

Goals-based portfolios and the impact of financial repression

If we take a step back and consider the net result of the GBAA framework, we can see that it results in an allocation that is barbelled between low-risk and high-risk assets to a greater or lesser extent depending on an investor's circumstances and preferences. To state the obvious, the greater one weights either the safe or the opportunity bucket, or likely both, the more barbelled the resulting portfolio allocation. This barbell structure seeks to satisfy our psychological longings, while retaining a core exposure in the market blend. On the other hand, as our investor reduces these buckets in favor of the diversified-market bucket, that investor increasingly resembles the rare, economically rational man, invested mostly in an MPT-efficient market portfolio.

We do not need financial simulations to see that the more barbelled the overall allocation, the more convex the return distribution will be compared to the MPT portfolio. In other words, a well-constructed GBAA portfolio, allocated to all three buckets, will have more downside protection and more upside potential than a conventional portfolio. (Note that upside potential is not the same as expected return; the third bucket, by definition a concentrated position, has the potential to do extremely well or to fail completely.) The GBAA portfolio will also likely underperform by some margin across a wide range of middle-return scenarios. This is conceptually similar to augmenting a market portfolio with long positions in out-of-the-money put and call options, with the premiums paid from the market portfolio returns. While this analogy is useful in concept, it is important to remember that our actual safe and opportunity buckets, given their specific construction, will differ quite a bit from market-based put and call options.

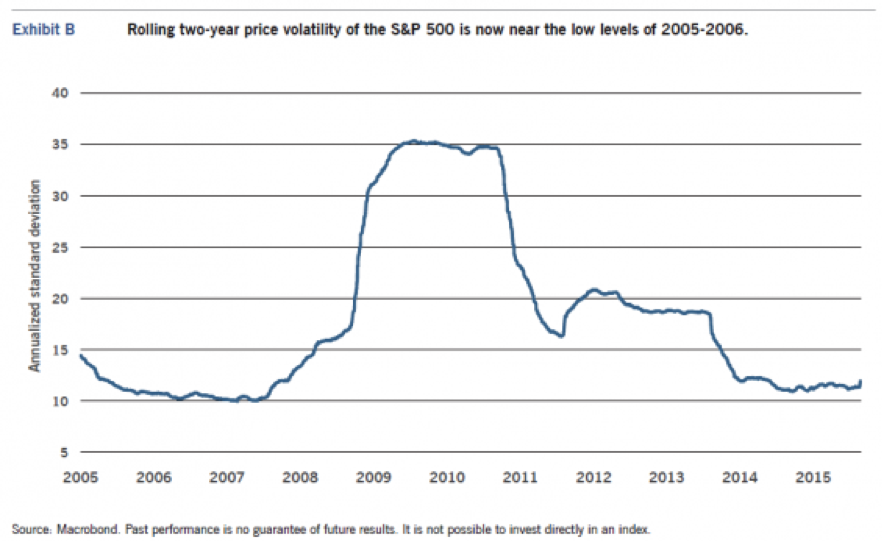

While necessarily limited, this analogy nevertheless provides insight into the impact of financial repression on the GBAA process and resulting portfolios. We will assume here that the reader hasn’t just arrived from another planet and is familiar with the zero interest-rate policies (ZIRP) and quantitative-easing programs (QE) undertaken by the developed world’s central banks since the GFC over six years ago. These programs have succeeded in raising valuations and compressing risk premiums across virtually all asset classes, so much so that prospective future returns are now abnormally low. These efforts have also suppressed volatility in the markets, especially the equity markets. Exhibit B shows the rolling two-year price volatility of the S&P 500, which is now near the low levels of 2005-2006. As we know, trends in volatility drive options prices, which are based on the market’s view of future volatility. In this way, volatility also drives the pricing of barbell portfolios relative to bullet portfolios; when implied volatility is low, barbells will be cheaper to implement than when volatility is high. Furthermore, when volatility falls, barbells will tend to underperform bullet portfolios, everything else equal. When volatility rises, barbells will tend to outperform.

The implications for goals-based allocations are intriguing. The bad news is that they have likely underperformed market portfolios of similar overall risk since the GFC, as markets have become more highly valued and volatility has progressively declined. In other words, our GBAA “insurance policy” has not been needed during this period. The good news is that, with volatility low and valuations high, this may be an excellent time to shift to a GBAA framework from a conventional one.

Several caveats merit mention. First, the realized performance of any actual GBAA allocation over these past six years has depended on both the relative weightings of all three buckets and, likely as important, the specific assets held in each bucket, especially the opportunity bucket. If assets held in this bucket have paid off very handsomely, then the GBAA portfolio may have outperformed. Future performance will similarly depend on the specific assets held.

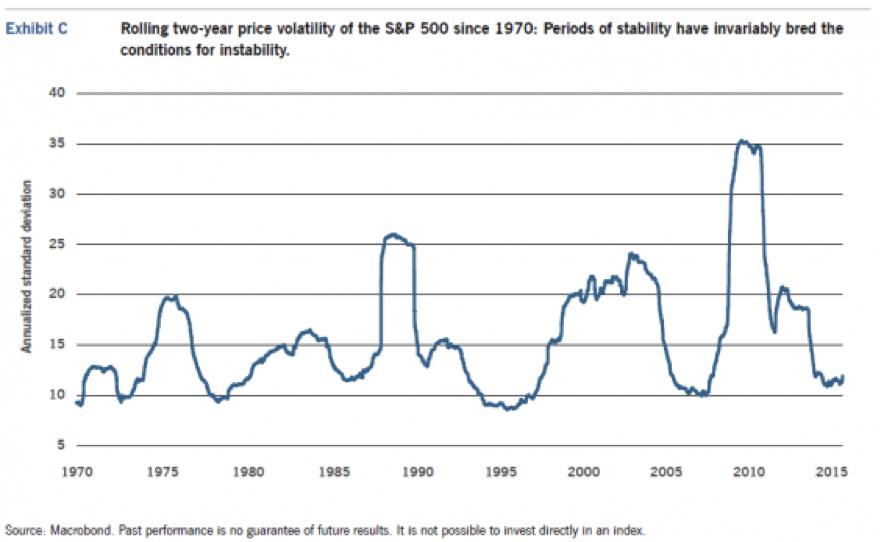

Second, future performance will also depend on what happens next with market volatility and returns. The key here is whether volatility stays repressed, with sustained high valuations, for the foreseeable future, or begins to mean-revert higher as policy support is reduced and markets return to more normal functioning and valuations. Exhibit C demonstrates that volatility has reliably mean-reverted over the past four decades, as periods of unusual stability invariably bred the conditions for instability. Of course, this time may be different. In the next section, we will consider the possibilities for the evolution of financial repression, and the implications for GBAA.

The half-life of financial repression

The objectives of ZIRP and QE have always seemed somewhat muddled – namely, to artificially but temporarily raise valuations of risky financial assets by making safe financial assets relatively scarce. By lowering interest rates and compressing risk premiums, and, thus, the cost of capital, it was thought that more borrowing, investing and economic growth would begin to occur. At that point the programs would end, and markets would return to normal functioning. How this return to normal would not damage the economy as much as the intervention had helped was never fully explained, perhaps because the Fed had no good explanation. Ben Bernanke has even admitted that the Fed isn’t really sure how or why QE works, attributing it mostly to a signaling effect, the signal being that policy will remain accommodative for the foreseeable future. Given that, one might indeed wonder if QE will work in totality – that is, if it will leave the economy better off after the programs have been concluded and the signal is that support is now being withdrawn. In other words, is QE at best a temporary salve to markets and the economy?

Clearly, lower interest rates and lower risk premiums have allowed debt to be refinanced and carried more cheaply, and have, thus, transferred wealth from creditors to debtors. Nevertheless, because households are net creditors and government and corporations are net debtors, it’s not certain how helpful this has been for economic growth. Clearly, higher equity and home prices have increased the wealth of those already owning those assets, while also making them more expensive to acquire for those who don’t. Again, we have both winners and losers, although the winners have a higher propensity to save than the losers. So, here too, the benefits are questionable. Perhaps the major benefit has come from currency depreciation. QE cheapened the dollar relative to foreign currencies, and the U.S. gained trade competitiveness despite losing international purchasing power. Other major central banks, however, are now pursuing QE more aggressively than the Fed and the dollar has recently strengthened, so perhaps these trade gains are now reversing. Or, at best, perhaps competitive devaluations are approaching a stalemate of sorts, allowing competitiveness to now stabilize across currency regions.

It seems more questions than answers exist about QE, which is not surprising considering the unprecedented nature of what central banks have undertaken these past few years. Our objective here, though, is not to judge the wisdom or efficacy of these programs, but to gauge the likelihood of what comes next. What we can say with some conviction is that the Fed is now gradually moving to reverse the process unless something upsets the apple cart. Its net bond buying has ended and it has been signaling that ZIRP is likely to end this fall with the first rate hike since 2006. Policy is gradually being tightened, and this is likely to continue, barring a change in the growth outlook. Bond market volatility has begun to move higher, as have bond yields. In recent weeks, equity volatility has also begun to move higher, somewhat dramatically, although equity indexes remain near all-time highs.

Without getting too far into the weeds and beyond the scope of this paper, we think it is possible to make several inferences here for GBAA. First, a shift in policy regime after such a long time seems as likely a candidate as any to trigger a move higher in market volatility. Historically, it has taken several tightening moves to provoke markets. One could argue here that, even though this would be the first rate increase, actual policy tightening began months ago when the Fed first reduced and then stopped asset purchases altogether. A counter argument would be that this rate scenario has been well telegraphed and is already priced into markets, and volatility will remain low unless something unexpected happens.

The second implication goes beyond volatility and focuses on valuations. QE has helped U.S. equities in particular achieve all-time high nominal prices and rich valuations measured in a host of ways – relative to trailing, forward or normalized earnings, relative to book value or replacement costs, relative to GDP, relative to sales and so forth. When also considering that U.S. profit margins are at the high end of historical ranges, and that labor costs and interest rates may now be rising, all collectively a drag on future earnings growth, it is reasonable to conclude that forward-looking returns from equities will be significantly lower than the recent past or historical norms. Common estimates today are 0%-3% real returns for the S&P 500 over the next 7-10 years, barely above expected real returns for bonds. In other words, the efficient frontier today is both low and flat – investors are being offered lower returns and much less incremental return for incremental risk than has typically been the case historically.

This should be no surprise; after all, the whole point of QE was to compress risk premiums. The implication of a flat efficient frontier and low but potentially rising volatility is that the barbell structure favored by GBAA is both relatively inexpensive to hold, should policy and market renormalization be delayed, and also likely to outperform the market portfolio when policy and market valuations do eventually renormalize. This is because the GBAA portfolio replaces a portion of our risky broad-market assets with, in all cases, an allocation to safe assets and, in some cases, an allocation to concentrated, and likely personalized, "opportunity" assets. In many cases these assets already exist in the investor’s portfolio and just need to be properly accounted for, as opposed to creating a new investment allocation. Concentrated risky assets provide an alpha opportunity – they will hopefully outperform broad-market risky assets but could also underperform, perhaps significantly so. Nevertheless, the investor presumably has better reasons for holding them than overvalued broad-market assets; if not, they should likely be liquidated, if possible.

Flexibility to customize

The comments above are necessarily general and border on the obvious. Still, the beauty of the GBAA framework is its flexibility. Allocations across buckets and within buckets are necessarily already customized for a given investor's situation, risk preferences and illiquid assets. Those with explicit concerns can structure portfolios to better reflect those concerns. While we would not advocate tactically managing assets across buckets, as this may encourage the type of behavior we are trying to avoid, strategic shifts or tilts within buckets based on longer-run market considerations may make as much sense as those due to changes in a given investor's circumstances.

For example, those concerned about a move higher in volatility, with negative or uncertain implications for risky-asset performance, could shift the benchmark and portfolio allocation for the diversified-market bucket to a somewhat less risky one. Another example of a strategic tilt would be a more barbelled allocation within the safe bucket for those concerned about the chances of more extreme deflationary or inflationary outcomes. In this case, the fixed-income portion of this bucket could be reduced, while also raising the quality and duration of those securities to better hedge deflation risk, and the inflation-sensitive portion increased, while further diversifying it among a variety of inflation-sensitive assets.

The key point here is that the GBAA framework should be seen as a dynamic framework and not as a rigid or confining one. It is in essence just a way of segregating and allocating assets more in line with both our personal goals and our human way of thinking about risk. Our goals, our wealth and our risk preferences will all likely change over time, not to mention our age. The GBAA framework is an extremely flexible one, better able to accommodate all those changing factors than conventional approaches. As such, this framework is also more accessible and understandable for the layman. For investment managers whose clients are not primarily CFAs or finance professionals, this should come as a welcome change.

Appendix

Blanchett, David M. and Philip U. Straehl. 2015. “No Portfolio Is an Island.” Financial Analysts Journal, vol. 71, no. 3 (May/June)

Brunel, Jean L.P. 2007. Is a Behavioral-Finance-Based Allocation Really Suboptimal? CFA Institute

Brunel, Jean L.P. 2012. Goals-Based Wealth Management in Practice. CFA Institute

Chhabra, Ashvin B. and Lex Zaharoff. 2001. “Setting an Asset Allocation Strategy by Balancing Personal and Market Risks.” The Journal of Wealth Management, vol. 4, no. 3 (Winter)

Chhabra, Ashvin B. 2005. “Beyond Markowitz: A Comprehensive Wealth Allocation Framework for Individual Investors.” The Journal of Wealth Management, vol. 7, no.4 (Spring)

Chhabra, Ashvin B., Ravindra Koneru, and Lex Zaharoff. 2011. “Modern Portfolio Theory’s Third Rail: Achieving Wealth Mobility through Idiosyncratic Risk.” The Journal of Wealth Management, vol. 14, no. 1 (Summer)

Chhabra, Ashvin B. 2012. A Risk-Based Asset Allocation Framework for Unstable Markets. CFA Institute

Das, Sanjiv, Harry Markowitz, Jonathan Scheid, and Meir Statman. 2010. “Portfolio Optimization with Mental Accounts.” Journal of Financial and Quantitative Analysis, vol. 45, no. 2 (April)

Ibbotson, Roger G., Moshe A. Milevsky, Peng Chen, and Kevin X. Zhu. 2007. Lifetime Financial Advice: Human Capital, Asset Allocation, and Insurance. CFA Institute

Kahneman, Daniel, and Amos Tversky. 1979. “Prospect Theory: An Analysis of Decision under Risk.” Econometrica, vol. 47, no.2 (March)

Nevins, Dan. 2004. “Goals-based Investing: Integrating Traditional and Behavioral Finance.” The Journal of Wealth Management, vol. 6, no. 4 (Spring)

Shefrin, Hersh, and Meir Statman. 2000. “Behavioral Portfolio Theory.” Journal of Financial and Quantitative Analysis, vol. 35, no. 2 (June)

Tversky, Amos, and Daniel Kahneman. 1992. “Advances in Prospect Theory: Cumulative Representation of Uncertainty.” Journal of Risk and Uncertainty, vol. 5

About Risk

As interest rates rise, the value of certain income investments is likely to decline. Investments in foreign instruments or currencies can involve greater risk and volatility than U.S. investments because of adverse markets, economic, political, regulatory, geopolitical or other conditions. In emerging countries, these risks may be more significant. An imbalance in supply and demand in the income market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. High yield and floating-rate loans are primarily below-investment-grade debt obligations, which are considered speculative because of the increased credit risk of their issuers. Floating-rate loans and other debt securities, including high yield for example, are subject to the risk of increases in prevailing interest rates, although floating-rate securities are less susceptible to this risk than other fixed-rate obligations. Generally, bond values will decline as interest rates rise. However, because floating rates on senior loans only reset periodically, changes in prevailing interest rates can be expected to cause some fluctuation in a portfolio’s value. Similarly, a sudden and significant increase in market interest rates, a default in a loan in which a portfolio owns an interest or a material deterioration of a borrower’s creditworthiness may cause a decline in value. Floating-rate loans may be more susceptible to adverse economic and business conditions and other developments affecting the issuers of such loans. The value of income securities also may decline because of real or perceived concerns about the issuer’s ability to make payment of principal and interest payments. Although senior floating-rate loans are generally collateralized, there is no guarantee that the value of collateral will not decline, causing a loan to be substantially unsecured. No active trading market may exist for many loans, and some loans may be subject to restrictions on resale, which may also prevent the manager from obtaining the full value of a loan when sold. Derivative instruments can be highly volatile, result in economic leverage, which may magnify losses, and involve risks in addition to the risks of the underlying instrument on which the derivative is based, such a counterparty, correlation and liquidity risk. The strategies discussed may engage in other investment practices that may involve additional risks. The views and strategies described may not be suitable for all investors. The strategies described should not be considered a complete investment program

Past performance is no guarantee of future results. It is not possible to invest directly in an index.

About Eaton Vance

Eaton Vance Corp. is one of the oldest investment management firms in the United States, with a history dating to 1924. Eaton Vance and its affiliates offer individuals and institutions a broad array of investment strategies and wealth management solutions. The Company’s long record of exemplary service, timely innovation and attractive returns through a variety of market conditions has made Eaton Vance the investment manager of choice for many of today’s most discerning investors. For more information, visit eatonvance.com.

The views expressed in this Insight are those of Thomas A. Shively and are current only through the date stated at the top of this page. These views are subject to change at any time based upon market or other conditions, and Eaton Vance disclaims any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Eaton Vance are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Eaton Vance fund.

This Insight may contain statements that are not historical facts, referred to as forward-looking statements. Future results may differ significantly from those stated in forward-looking statements, depending on factors such as changes in securities or financial markets or general economic conditions.

Before investing, investors should consider carefully the investment objectives, risks, charges and expenses of a mutual fund. This and other important information is contained in the prospectus and summary prospectus, which can be obtained from a financial advisor. Prospective investors should read the prospectus carefully before investing.

©2015 Eaton Vance Distributors, Inc. | Member FINRA/SIPC | Two International Place, Boston, MA 02110 | 800.836.2414 | eatonvance.com