US High Yield: Energy Is Lagging, but Consumers Are Set to Spend

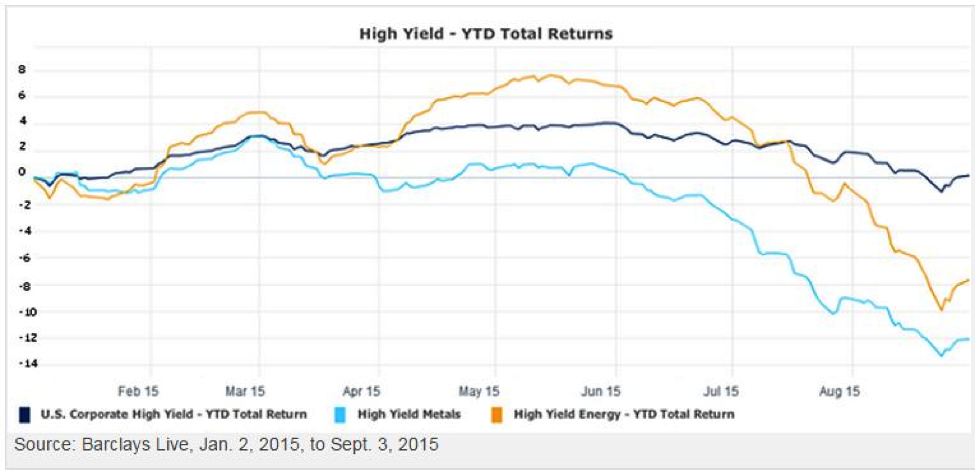

Weak commodity prices have made this year’s US high yield story a “tale of two markets.” Year-to-date returns for the overall high yield market were a meager three basis points (0.03%) through Aug. 31.1 However, if you peel back energy and metals and mining, the rest of the asset class delivered a respectable 2.6% total return over the same period.1

The Invesco High Yield team thinks this bifurcation of the high yield market broadly between commodity- and non-commodity-related segments is likely to persist in the coming months. We expect commodity prices to remain lower for longer, challenging those commodity-related sectors in US high yield that are vulnerable to global supply/demand changes. However, the US economy remains on track to grow moderately, supporting US-centric high yield issuers that are less exposed to volatility in global commodities. We believe this dynamic bodes well for the overall high yield market over the longer term, as around 75% of high yield issuers are US-focused and are in good fundamental shape.2 For the most part, we expect the US-centric segment of the high yield market to be relatively immune to the volatility we have seen out of China and other emerging markets.

2015 US high yield returns have been dragged down by commodity-related sectors

Energy: Suffering short-term pressure, but market forces may strengthen prices

We think the underperformance of the US high yield energy sector is justified, in the short run, as global macro factors (perceived or otherwise) and a near-term mismatch between supply and demand have weighed heavily on oil prices. However, we believe we are seeing signs that US oil supply is adjusting and that global oil demand is running higher than consensus estimates — a combination of factors that could help balance the market and bring stability to prices.

As for the macro side of the equation, most fears center on the potential for a sharp decline in Chinese demand, but we do not anticipate a hard landing in China. We firmly believe oil is different from many other commodities since it is the cheapest available transportation fuel. While demand for many commodities is down year-over-year, the opposite is true for oil, as global demand continues to grow.3 With these points in mind, even some of the most bearish oil forecasts are calling for oil prices around the $60-per-barrel level (West Texas Intermediate) in 2016.3 We think this is reasonable, if not a little low.

That said, our strategy within the energy sector continues to center on owning higher-quality, independent producers that can weather the current low-price environment. Overall, we are slightly overweight the sector, but credit selection is critical.

Metals and mining: China drives the pace of demand

China slowdown fears have had a pronounced impact on the US metals and mining sector, with a year-to-date total return of -15.3%.1 From a demand standpoint, China remains the largest consumer of non-oil commodities and thus has the greatest demand-side influence on most commodity prices. However, the recent down cycle in commodities has as much to do with supply as it does with demand.

Within the sector, the worst performer continues to be coal, which is facing secular decline due to stiff environmental regulations and the impact of substitution toward cheap natural gas. While steel faces overcapacity issues globally, US producers in particular have had to contend with competition from imports and thus lower margins. Mining, on the other hand, is coming out of a mostly debt-funded growth spurt, which has created an oversupply situation resulting in a sharp price correction for most industrial metals.

Against this backdrop, we remain underweight the sector. We recognize that supply imbalances can take time to correct and we focus on credits that can survive the tough pricing environment. We expect the pace of recovery for each commodity to be determined by China’s share in global demand for that commodity. We seek to capture US-centric ideas or credits that have a cost advantage in the long run.

Mining for alpha

Global macro headwinds and technical forces may impact short-term movements in the high yield market, but default forecasts remain well below long-term averages.4 The high yield asset class outside of commodity-related sectors has been fairly resilient, and we continue to favor the retail, housing and health care sectors — which are more dependent on US consumers than they are on global commodity prices. At the same time, we believe that there are select opportunities to be had within the lagging commodity sectors, and we look for those via careful credit selection and prudent risk management.

1 Source: JP Morgan US High Yield Index, Aug. 31, 2015.

2 Source: BAML, April 6, 2015.

3 Source: CIBC, The Oil View, Aug. 12, 2015.

4 Source: JP Morgan high yield default forecast — 2015: 1.5%; 2016: 3%; Long-term average: 3.6% (Dec. 31, 1986, to June 30, 2015)

Important information

Commodities may subject an investor to greater volatility than traditional securities such as stocks and bonds and can fluctuate significantly based on weather, political, tax, and other regulatory and market developments.

Businesses in the energy sector may be adversely affected by foreign, federal or state regulations governing energy production, distribution and sale as well as supply-and-demand for energy resources. Short-term volatility in energy prices may cause share price fluctuations.

The risks of investing in securities of foreign issuers, including emerging market issuers, can include fluctuations in foreign currencies, political and economic instability, and foreign taxation issues.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2015 Invesco Ltd. All rights reserved.

US high yield: Energy is lagging, but consumers are set to spend by Invesco Blog