Current trends support the notion that U.S. stock valuations are far from overstretched.

Prices up, prices down—the trends in mutual fund flows seem to continue unaltered. Money flows out of domestic U.S. equities and into foreign equities, hybrid funds, and bonds, regardless of how low yields fall or how well or poorly the stock market does. In the present instant, this pattern would all seem reasonable, given the recent panic in equity markets (though foreign equities, if anything, have suffered worse). What is unusual is that the equity outflows also occurred when stock prices were rising rapidly. Nor, it seems, have different market environments prompted trends to accelerate or decelerate. Having such a strong ongoing trend means that there is no telling when patterns might change, much less when a preference for domestic equities will return. The ongoing flight from U.S. equities does, however, offer one firm conclusion: the stock market looks far from overbought.

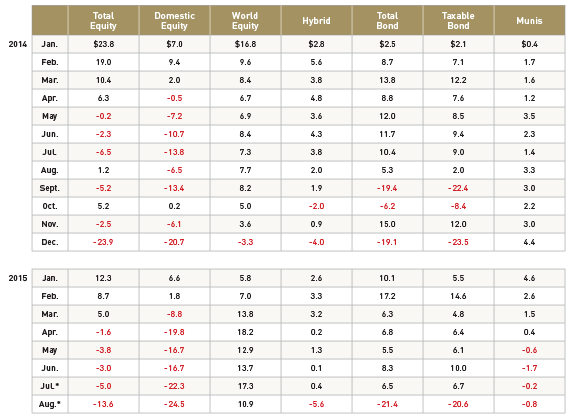

According to Investment Company Institute (ICI) data (a summary of which is provided in Table 1), domestic equity funds suffered net outflows in August and July only modestly more severe than generally for the last 15 months. Admittedly, the August figures are incomplete, but the preliminary tally points to a net outflow of $24.5 billion, or about 0.4% of such assets under management. That is only a slight acceleration from the $22.3 billion net outflow recorded in July, though it is a greater acceleration from the still large $16.7 billion net outflow recorded in May and June each or the $20 billion net outflow recorded in April.1

Much of this money has gone into what the ICI labels world equities and hybrid funds. The former enjoyed inflows of $17.3 billion in July and $10.9 billion in August. Both are entirely consistent with monthly inflows of between $13–$18 billion this past spring, and inflows only slightly less going back all the way to before January 2013. Indeed, during the past 32 months, world funds have suffered only one month of outflows, December 2014, and that amounted to only $3.3 billion. Hybrid funds have proceeded along a less even path, but on balance have received inflows. They did see net outflows of $5.6 billion in August, or about 0.4% of the assets so classified. Otherwise, they have experienced only two other months of outflows during the last three years.

Bonds have not benefited from the July–August flight from equities. According to preliminary data, bonds (taxable and municipal combined) saw outflows of $21.4 billion in August, after inflows of $6.5 billion in July, or about -0.6% and 0.2%, respectively, of the outstanding amount. But otherwise during this longer three-year period, money, with some notable exceptions, continued to flow into bond funds as it flowed out of domestic equities. Aside from the August outflow, bonds in general have suffered only three months of outflows in the past three years. Drilling down to the distinction between taxable and municipals shows no great difference, though the months of maximum outflow and inflow differ between the two categories.

All this data only vaguely point to a reason why investors have remained so equity-shy for so long, even when prices were rising fast and retail investors in the past would have chased positive returns. Earlier in the recovery, between 2012 and 2013, this was indeed the case. During that time, very few months suffered outflows from domestic equities and several enjoyed inflows in excess of $20.0 billion. The turn in sentiment developed only after the opening months of 2014. It would seem from this timing that it reflects fearful memories of past stock market busts, especially the steep declines between the 2007 peak and the 2009 trough. Earlier in the upswing, when the likelihood of such a violent downturn was lower, retail investors seemed less afraid. But contrary to historical patterns, when investors invariably chased gains, impressive stock gains in 2013 and early 2014 combined with these fearful memories to create a strong wariness that equities might not sustain high prices and would collapse again. That wariness has persisted into the present.

The pattern, however, is a clear break from the past. Then as retail investors reliably chased good stock performance by increasing investment flows into domestic U.S. equities, their action tended to exaggerate the market gains, prompting markets to realize any remaining value quickly, thereby setting up the rally for a fundamental correction. Without such behavior this time, the market should continue to realize value, albeit at a slower pace than in the past, extending its up move over a longer time frame and delaying the point when valuations tempt a more fundamental retrenchment.

Table 1. Flows Into and Out of Mutual Funds

($ in billions, net of market movements)

Source: Investment Company Institute.

*Preliminary.

1All data herein from the Investment Company Institute.

Note: All investments involve risks, including the loss of principal invested. The value of investments in equity securities will fluctuate in response to general economic conditions and to changes in the prospects of particular companies and/or sectors in the economy.

The opinions in the preceding economic commentary are as of the date of publication, are subject to change based on subsequent developments, and may not reflect the views of the firm as a whole. This material is not intended to be relied upon as a forecast, research, or investment advice regarding a particular investment or the markets in general. Nor is it intended to predict or depict performance of any investment. This document is prepared based on information Lord Abbett deems reliable; however, Lord Abbett does not warrant the accuracy and completeness of the information. Consult a financial advisor on the strategy best for you.