The negative impact of China’s slowdown continued this week as the OECD lowered its global growth forecast:

“Global growth prospects have weakened slightly and the outlook is clouded by important uncertainties,” said OECD Chief Economist Catherine L. Mann. “Emerging economies have vulnerabilities that could be exposed by rising US interest rates and/or a sharper-than-expected slowdown in China, giving rise to financial and economic turbulence that could also exert a significant drag on advanced economies. Continued policy stimulus is warranted to support global demand, but the mix of policies will differ by country, and choices need to be consistent with financial stability and reviving long-run growth.”

While their analysis focuses on the now familiar triangle of China, emerging economies and Fed policy, the OECD emphasizes emerging economies’ dual economic vulnerabilities to China’s slowdown and US interest rate policy. The former began within the last 12 months while the latter is an ongoing threat. The OECD analysis also noted the US continues to grow “solidly.” They were somewhat disappointed in the EU, commenting, “Growth in the euro area is improving, but not as fast as would be expected given the falls that have been seen in oil prices, long-term interest rates and the value of the euro.” China’s slowdown was bound to increase downside economic predictions. Citigroup led the charge last week and now the OECD is following suit. Expect further negative revisions over the next few weeks and months.

The Fed’s policy decision was the main news item this week. While they maintained rates at 0%-.25%, they slightly broadened focus to include international developments. They first noted the US continues to expand: “Information received since the Federal Open Market Committee met in July suggests that economic activity is expanding at a moderate pace.” But the risk from non-U.S. markets increased: "Recent global economic and financial developments may restrain economic activity somewhat and are likely to put further downward pressure on inflation in the near term ... The Committee continues to see the risks to the outlook for economic activity and the labor market as nearly balanced but is monitoring developments abroad.” Finally, the statement tied international weakness into US economic performance when they noted exports were “soft.” Overall, the Fed’s non-action wasn’t surprising, especially considering recent international developments. And as I noted earlier this week, this remains the most over-hyped interest rate in history.

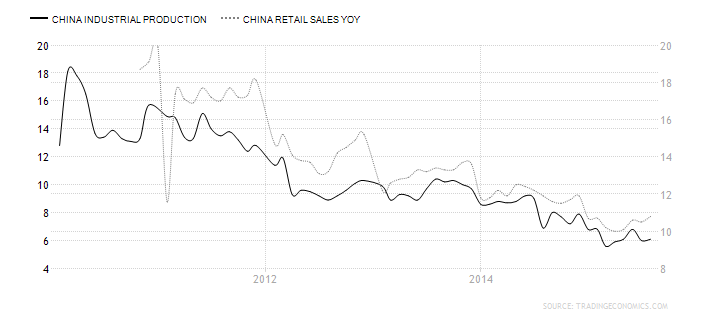

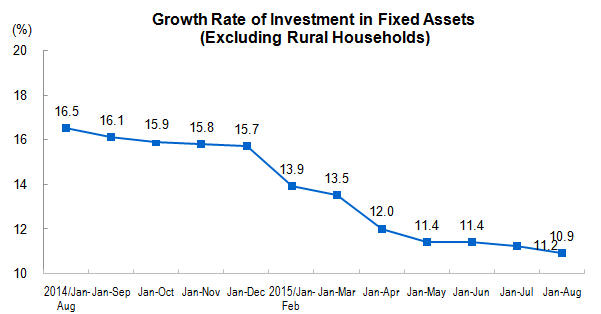

Clearly, China is now the Fed’s top international concern; last week’s economic events didn’t calm any Fed nerves. As noted in a previous column, the Shanghai Index continues stabilizing in bear market territory, finishing a routine sell-off from bubble heights. Last week’s economic releases continued to show a slowing economy. While industrial production, retail sales and capital investment increased (all Y/Y) 6.1%, 10.8% and 11.3% respectively, the long-term trend for all three continues lower:

The Chinese die is cast; their economy is slowing.

Australia changed prime ministers for the fifth time in five years this week. Analysts describe the new leader as a deeper, more nuanced thinker who views China as a key component to Australia’s future. He inherits an economy in transition. As noted in the latest RBA policy minutes, the Australian economy is growing below potential. While other business fares moderately well, mining remains the primary problem:

Members began their discussion of the recent economic data by considering indicators of business conditions. Surveys of business conditions generally had shown further improvement over recent months and conditions were clearly above average levels in the household and business service sectors. Although survey measures suggested that business profits had increased to above-average levels, ABS data showed that, relative to nominal GDP, mining profits had declined further following falls in commodity prices and non-mining profits had remained relatively stable.

The ABS capital expenditure survey had suggested a further fall in mining investment in the June quarter and investment intentions in that sector implied a further sizeable fall in 2015/16, which was consistent with the Bank's current forecasts. Members discussed the implications of the recent emphasis on cost cutting in the mining sector, noting that it would probably lead to mining investment eventually stabilising at a lower level than had previously been expected. The capital expenditure survey also pointed to a decline in non-mining investment in 2015/16, but by less than implied by the survey taken three months earlier. Approvals for non-residential building also remained weak.

As this graph from the latest capital expenditure survey shows, overall capital investment has declined since 2012:

In contrast, consumption growth is positive: “Members observed that recent indicators of consumer sentiment and retail sales had been consistent with some increase in consumption growth.” Retail sales have consistently increased for the last two years:

And housing remains a strong source of growth.

The Australian economy continues to change from an export to a consumer growth modality. Export industries, which were largely raw material extraction companies, decreased capital expenditures in 2012. Ancillary industries slowed their spending in response. These events created economic headwinds, but not to the point of contraction. Unfortunately, no new sector sufficiently fills the economic void nor provides broad enough stimulus to hasten the desired transformation. Housing has partially replaced the lost growth, but as the U.S., U.K. and Europe will attest, housing can’t sustain an economy over the long term.

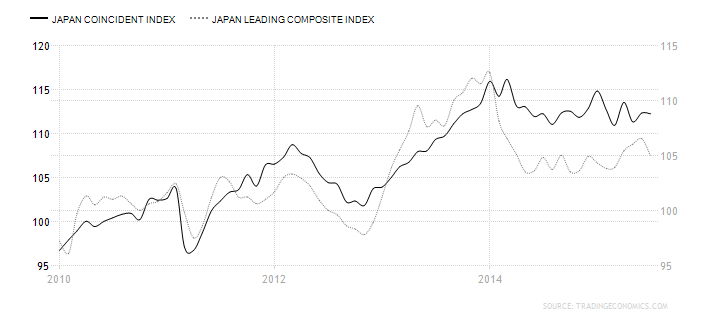

The BOJ maintained their current interest rate and asset purchase policy. They also released their latest meeting minutes. While the minutes contained moderately positive descriptions of the Japanese economy, the statistical story provides a less hopeful picture. Both the leading and coincident economic indicators compiled by Statistics Bureau of Japan paint a zero sum economic picture of the economy:

The LEIs moved sideways for most of 2014, then rose in early 2015. But the latest readings are down, indicating a loss of momentum. The coincident indicator continues in a sideways pattern for the last two years. The Conference Board’s LEIs and CEIs paint a similar picture:

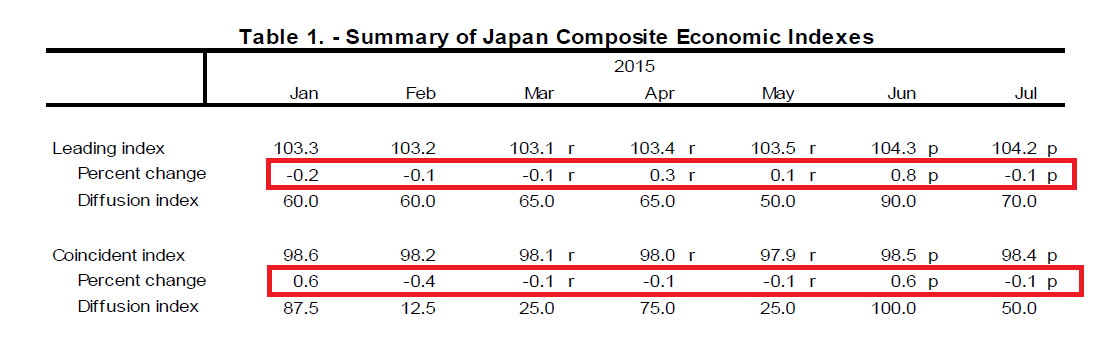

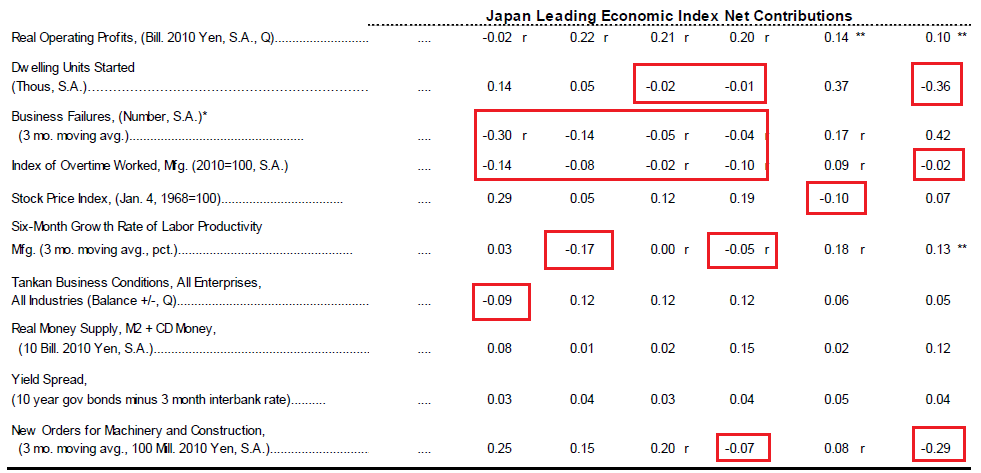

The CB LEIs decreased 4 of the last 6 months while the CEIs dropped 5 of the last 6. A variety of LEI index components contributed to recent declines:

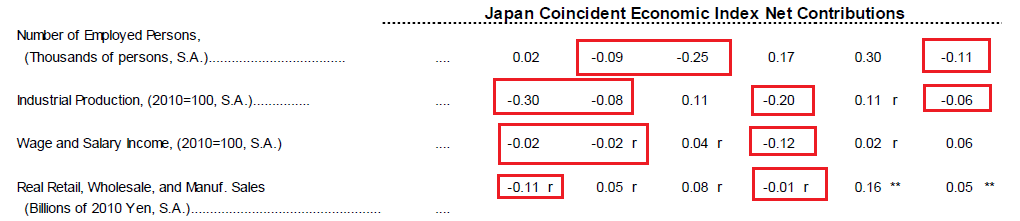

Only money supply and yield spread contributed positively to the index over the last six months. In contrast, dwelling investment dropped 3/6, business failures were down 4/6 and overtime worked decreased 5/6. The Conference Board’s Coincident Indicators show a similar problem:

Employment and wages are down 3/6 of the preceding months while industrial production is down 4/6. Retail sales decreased 2/6 month. When combined into a coherent statistical picture, the above data show an economy that, at best, is standing still, unable to achieve enough systemic momentum to move forward.

Analysts’ recent adjustments lowering global growth projections are in line with recent events; China’s economy continues slowing. This lowers commodity prices, which decreases economic growth of commodity exporting countries. Hence, the primary causation of Australia’s below trend growth and Japan’s weaker economic performance. The US is somewhat immune; Chinese trade accounts for a fraction of US GDP, limiting the impact. The EU is a bit more exposed, due to their increased reliance on trade. But the longer this trend continues, the higher the probability of increasing negative feedback loops hurting a larger percentage of economies, lowering overall global growth.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis