KEY TAKEAWAYS

· Fighting the Fed may be a winnable battle for EM.

· EM valuations are compelling and, in our view, have priced in a fair amount of risk.

· We see sufficient upside potential to maintain modest EM equity allocations despite significant growth challenges.

· We expect the Fed to hike rates in December 2015, although it could come earlier — as soon as this week — or potentially slip into early 2016. For our latest thoughts on the Fed, please see our latest Weekly Economic Commentary and Bond Market Perspectives.

Emerging market stocks have not won much lately, but the Fed may be a winnable fight. The Federal Reserve, which announces its policy decision on September 17, 2015, is on the verge of starting a rate hike cycle for the first time in more than 10 years. We have previously written that the start of Fed rate hikes has not marked an impending end to bull markets for U.S. stocks (despite the popular Wall Street adage “don’t fight the Fed.”) In reality, the first rate hike has told us we are about halfway through the cycle as discussed in our Weekly Market Commentary of August 25, 2014.

But what about emerging markets (EM)? Aren’t these markets more dependent on low interest rates and stimulative monetary policy? Here we look at how EM has performed leading up to and after the start of prior Fed rate hike campaigns. While historical data are limited, we believe this exercise may steer EM investors to consider “fighting the Fed.”

WALK DOWN MEMORY LANE

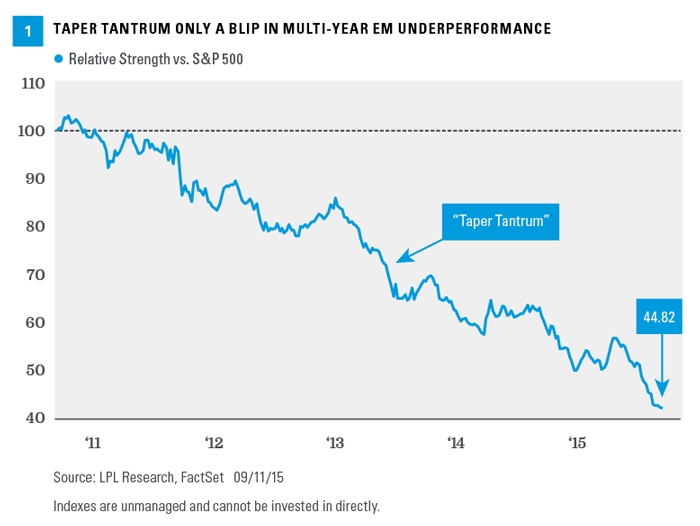

Before we take a walk down memory lane to assess how emerging markets equities might handle Fed rate hikes, some context is important. EM has performed poorly for five years now, having underperformed the S&P 500 by more than 50 percentage points during that period [Figure 1]. Tighter expected monetary policy is among the factors that contributed to this weakness. But we would argue that EM’s struggles go much deeper than that and can mostly be explained by other factors as we discuss below.

It is evident from looking back at performance during the “Taper Tantrum” during May through July 2013 (annotated in Figure 1) that Fed fears contributed to EM weakness. In May 2013, the Fed announced it would taper bond purchases associated with its quantitative easing program, which caused rate hike fears to intensify sending the 10-year Treasury yield more than 100 basis points (1%) higher in only about eight weeks. This period, during which EM underperformed the S&P 500 by about 12 percentage points, provided a reminder that EM had become somewhat dependent on low interest rates associated with quantitative easing. But as the figure shows, this was just a blip within a prolonged and much more significant period of weakness.

International and emerging markets investing involves special risks, such as currency fluctuation and political instability, and may not be suitable for all investors.

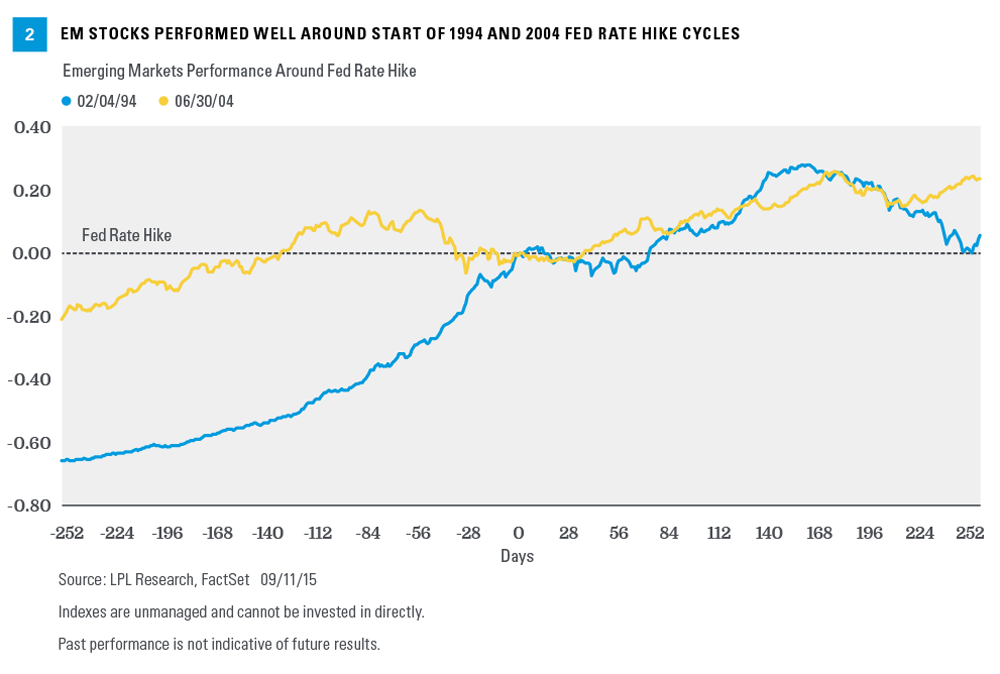

So should investors sell EM because of the Taper Tantrum? Not necessarily. We have two Fed rate hike cycles to assess (1990s and 2000s) for a more complete picture and EM generally performed well around both of them as shown in Figure 2. (Note that the MSCI Emerging Markets Index only goes back to the late 1980s.)

· February 1994 – The Fed rate hike in February of 1994 (on February 4, 1994) was proceeded by a roughly 70% rally in EM over the prior 12 months (all performance data in U.S. dollars), compared to just a 4% gain in the S&P 500 during that period despite the U.S. being in the early part of its economic cycle.

Chinese economic growth was at its peak (gross domestic product increased at a 14 –15% annual pace in 1994) and EM investing was beginning to gain popularity with U.S. investors.

In contrast, EM sold off after the February 2004 rate hike, suffered an 18% correction between September 19, 1994 and the one-year anniversary of the rate hike on February 4, 1995. During this period the S&P 500 actually managed a 1.6% gain. The EM selloff actually went quite a bit further, eventually becoming a 27% bear market decline by early March 1995. Even those EM losses only erased less than half the gains during the 12 months before the rate hike. It is also worth noting that this EM selloff failed to slow the U.S. market down as the S&P 500 went on to post a 34% gain in 1995.

Before worrying about a repeat of that EM decline in 1994 after a potential rate hike this fall, we would argue that the Fed had little to do with the EM losses in 1994. Late 1994 was the start of the Mexican peso crisis that brought a 50% currency devaluation (far from the mere 3% devaluation of the Chinese yuan a few weeks ago).

Also consider that EM just endured a bear market decline of 25% from May 1, 2015 to September 4, 2015, so the market has likely priced in a fair amount of interest rate (and currency) risk.

· June 2004 – EM performed very well in the 12 months ahead of the start of the Fed rate hike campaign that began on June 2004, with a 23% advance. While that trailed the pre-rate hike EM performance in 1993-1994, EM performed better one year after the hike in 2004 than in 1994, posting a 23% gain from June 30, 2004 through June 30, 2005. That performance outpaced the S&P 500, which gained 17% during the 12 months before the hike and just 5% during the 12 months after. China’s economy was still growing very rapidly during this period (about 10% GDP growth) and the China-fueled commodities boom was well underway and helped attract capital into emerging markets.

Although this generally good EM performance during these periods came with some volatility, and in the case of 1994 preceded a Mexican currency crisis, it should provide at least some comfort for those with EM positions who may be worried about the Fed. That said, the EM environment is quite different today.

SLOWER GROWTH

China is no longer growing at the double-digit rates of the 1990s and 2000s. Its growth rate is likely closer to 5 – 6% today (though they continue to report 7%). Because of China’s key role as a growth engine for EM, matching the strong performances of 1994 and 2004 may be difficult. Growth is also slower in the U.S. and Europe than it was then, limiting EM export opportunities.

COMMODITY BEAR

We are also in a severe commodity bear market today. Based on the Bloomberg Commodity Index, commodity prices have fallen 63% from their July 2008 peak. Many of the largest EM countries that rely on commodity exports, such as Brazil and Russia, have been hurt by the significant commodity price declines in recent years. The absence of commodity price gains, due largely to less demand from China as it transitions to a more consumer-oriented economy, is a big difference between the EM environment today and that of 1994 and, especially, 2004. Broadly, the benefits that lower oil prices have brought to EM commodity importers have not been enough to offset the drag on EM commodity producers.

BUT THERE ARE POSITIVES

While these key differences suggest more modest returns ahead from EM, we would also highlight several factors suggesting EM is better equipped to manage the risk of impending Fed rate hikes. First, more countries have floating currencies (rather than U.S. dollar pegs) with bigger foreign currency reserves, and are therefore less susceptible to currency crisis. Second, current account balances have improved, reducing reliance for many EM countries on foreign capital (capital that would be more expensive at higher interest rates) and keeping external debt levels manageable. And third, budget deficits are well contained (only a small handful including India and South Africa are worse than the U.S.). There are a few trouble spots, but EM countries in aggregate are generally in good financial shape.

UPDATED EM VIEW

EM is facing a lot of challenges. In addition to slowing economic growth and the risks surrounding tighter monetary policy, the asset class faces other headwinds:

· Earnings declines. Earnings are falling about 20% year over year, far worse than flat performance in the U.S. (and there are certainly headwinds we are facing here at home). Slower economic growth and commodities weakness are a big reason for this, but until EM can deliver some earnings stability and market participants see brighter days ahead, it will be difficult for these markets to get much going.

· Technical weakness. The MSCI Emerging Markets Index is exhibiting downward momentum based on the index price being below the downward sloping 50- and 200-day simple moving averages. Our assessment of the EM index chart, without consideration for fundamentals or valuation, tells us to wait for a better entry point.

· Geopolitics and governance. This headwind has always been there and is largely reflected in valuations, in our view, but is worth highlighting. There are conflict of interests between the corporate sector and the public sector, and poor accounting transparency (China, for example). There is political instability, such as we have seen in Greece in recent years. Corporate scandals are more prevalent, with Brazil’s largest energy company a recent example. And we all know about the risks of military conflict, e.g., Russia, and terrorism in the Middle East and beyond.

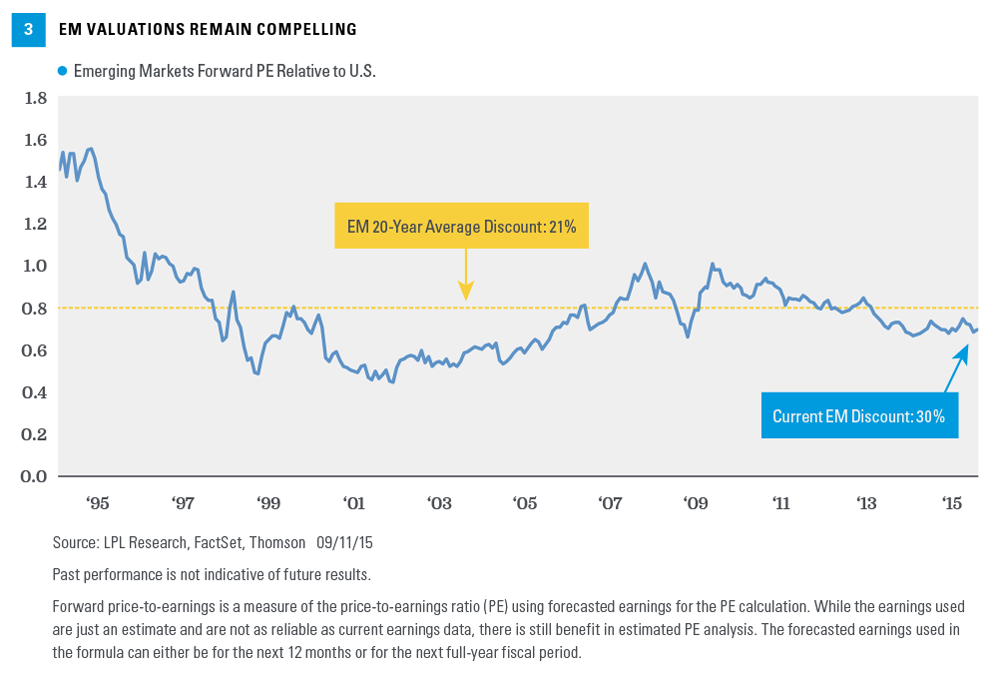

Bad place to invest, right? Not necessarily. We believe valuations are compelling enough that a modest allocation to EM equities as a diversifier to a predominantly U.S.-centric equity portfolio still makes sense. EM is now trading at about a 30% discount to the U.S. based on the forward price-to-earnings ratios of the MSCI EM Index and the S&P 500 [Figure 3]. We would also note that we expect China economic growth and therefore commodities prices to stabilize over the next 3 – 6 months, which should help buoy EM sentiment. While governance is still not up to developed market standards, market friendly reforms have been implemented in some markets such as India and Mexico, and even China. Finally, although the technicals tell us EM is in a clear downtrend, this discipline also tells us that when EM turns around, there may potentially be an attractive upside opportunity if the index can retrace some of its latest decline.

CONCLUSION

Fighting the Fed may be a winnable battle for EM. A lot of rate hike risk has been priced in following significant recent underperformance. EM performed quite well during prior Fed rate hike cycles in the 1990s and 2000s, while most of EM is better positioned financially to weather rate hikes than in the past. Valuations are compelling and, in our view, have priced in a fair amount of risk and earnings weakness. Growth challenges are significant, but we see sufficient upside potential to maintain modest EM equity allocations.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

All investing involves risk including loss of principal.

A simple moving average is calculated by adding the closing price of the security for a number of time periods and then dividing this total by the number of time periods. Short-term averages respond quickly to changes in the price of the underlying, while long-term averages are slow to react.

Commodity-linked investments may be more volatile and less liquid than the underlying instruments or measures, and their value may be affected by the performance of the overall commodities baskets as well as weather, disease, and regulatory developments.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The MSCI Emerging Markets Index captures large and mid cap representation across 23 emerging markets (EM) countries. With 822 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country. The Bloomberg Commodity Index is calculated on an excess return basis and composed of futures contracts on 22 physical commodities. It reflects the return of underlying commodity futures price movements.