Does a Higher Retirement Bogey Call for a Different Club?

If investors planning for retirement are a bit skittish these days one can hardly blame them. Stocks have turned volatile yet bond yields remain low. These aspects of today’s markets no doubt have investors wondering if their retirement portfolios will be sufficient to provide a reasonable standard of living.

For years, the rule of thumb was that 4% of a retirement portfolio could be accessed each year with a limited risk of depleting the nest egg. That is, a retiree could expect to spend $40,000 each year if invested in a $1 million portfolio. Or viewed inversely, if one wanted an investment portfolio to deliver $40,000 a year in retirement, $1 million should be accumulated for the job.

New research, however, suggests that a 4% spending rate is far more likely to exhaust the portfolio than generally believed. In a recently published white paper, “Rethinking Retirement – Sustainable Withdrawal Rates for New Retirees in 2015,” Wade Phau and Wade Dokken argue that retirees should consider taking no more than 1.3% to 1.7% of their nest egg each year.1

The original 4% “safe withdrawal rate” was the result of research by William Bengen and published in the October 1994 issue of the Journal of Financial Planning. Bengen examined all possible rolling 30-year periods of US financial market returns since 1926 to reach this conclusion: A 50% stock/50% bond portfolio could survive each of those 30-year return scenarios if no more than 4% was taken for living expenses each year. (Withdrawals were adjusted for inflation).2

Bengen also helped to popularize the idea of “sequence of return risk.” Bengen realized that two portfolios could experience an identical set of returns, but the portfolio incurring losses early in the distribution period (a.k.a. retirement) would be depleted more quickly than if those same negative returns occurred later in the sequence. So while a 4% withdrawal rate could result in a portfolio “living” well beyond 30 years, the 4% rate was just enough to allow the portfolio to survive the worst of the scenarios reviewed. (For the record, that worst case 30-year period began in 1966.)

While the 4% rule is obviously more of a starting point for discussion than a blueprint for distributions, the sub-2% withdrawal rates suggested by Phau and Dokken are shockingly low. This is partly due to the authors’ inclusion of investment advisor fees and fund expenses. Since the 4% rule doesn’t incorporate this fact of life, this dose of reality alone should shrink the 4% benchmark, they argue.

Phau and Dokken also suggest that because US stocks are unusually expensive today, valuation headwinds are likely to reduce returns from equities, particularly over the near to intermediate term. As a result, it is inappropriate to include some of the more bullish 30-year periods typically used in testing withdrawal rates

As evidence the market is unusually expensive, the authors refer to the Shiller P-E ratio. The Shiller measure of stock valuations compares stock prices to 10 years of historical earnings to reach a valuation metric. The measure, while nowhere near the record highs posted in 2000, is well above average and consistent with levels that historically have resulted in below average stock market returns.3

The premise of the Shiller P-E is that it is less susceptible to short term earnings blips that can distort valuations. For example, during a recession when earnings are low, stocks appear expensive. Yet, this is precisely when stocks are cheap compared to their long term earning power. In contrast, today’s trailing 12 month P-E benefits from a denominator several years into an economic expansion and is arguably inflated by unusually high profit margins. Further, per share earnings have been boosted by stock buybacks given companies’ recent preference for buying back their own shares over R&D and capex.

Detractors argue that the Shiller PE includes earnings (or lack of them) during the once-in-a-generation financial crisis. Thus, the measure understates a more normalized view of the earning power of US stocks. Stocks are not so expensive after all, they claim.

Phau and Dokken also suggest that today’s low bond yields should take a bite from the 4% distribution rate. Because retirement portfolios are generating little income from fixed income investments today, bonds are a drag on total returns. Further, if interest rates do rise, bond portfolios face downward pricing pressure as rising yields equate to lower bond prices. Given the three-decade bull market in bonds, retirees have been largely able to rely on bonds as a source of funds. With the relentless decline in rates, odds have been good that a 10-year bond would boast a capital gain five years down the road. The ability to sell bonds at a gain, particularly after stocks had a sinking spell, made the asset allocation/distribution puzzle a bit easier over the last three decades.

With bond yield near historic lows, once today’s retirees find themselves in need of cash, they may find that selling either stocks or bonds will result in a capital loss. Should this occur in the years immediately after retirement, the sequence of return risk mentioned earlier comes into play.

Phau and Dokken have even more bad news for retirement planners. While Bengen considered 30 years a reasonable objective for portfolio life, today’s investors are living longer. The downbeat duo present this statistic from a 2012 Society of Actuaries publication: There is a 43% chance that at least one member of a couple turning 65 will live to the age of 95. More often, Phau and Dokken argue, investors will need portfolios to last 40 years, not “just” 30.

We find it interesting that the search for the appropriate distribution rate often assumes a portion of the portfolio must be sold each year for living expenses. This tactic makes the value of the portfolio in any given year of primary concern. As a result, much time is spent devising asset allocations and investment strategies to limit changes in the market value of the portfolio. We wonder if too little attention is given to generating income and too much to guessing the price of stocks and bonds years down the road.

We have already established that traditional fixed income assets offer little in the way of income today. Further, we fear that investing in lower quality bonds to generate a bit more income will work less well going forward than was the case during the strong bull market in bonds. Yet, focusing on income may yet be the key to successful retirement planning. In fact, we think dividend paying equities can play an important role in retirement portfolios for a number of reasons. These include:

- A carefully selected portfolio of equities can generate more income than a high quality bond portfolio. A global approach to stock selection can increase the opportunity set for higher yields even further.

- A growing dividend stream increases the odds for long term capital gains, even during periods of rising interest rates. For example, a stock selling for $100 and paying a $4 dollar dividend is not likely to remain at $100 should the dividend eventually grow to $8.

- Investors still accumulating assets can always reinvest dividends in fixed income instruments should yields become attractive.

- Generating a growing income stream shifts the focus from market value to annual income. The former is far more volatile than the latter, tougher to predict, and more stressful to embrace.

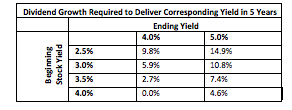

With the Fed seemingly on the verge of shift in monetary policy, investors may be tempted to wait for higher rates in an attempt to lock in a higher income stream. However, an important aspect of dividend-focused investing is dividend growth. A stock with a yield of 3.5% that manages to grow its dividend 7.4% annually will deliver a 5.0% “yield on cost” in five years.

The table below presents other examples of how quickly dividends must grow over five years to deliver a 4% or 5% yield on cost when starting from various levels of initial yield. The key point here is that a growing dividend income stream could well be one key to the retirement puzzle by providing more income than is available through today’s traditional fixed income alternatives. Dividend paying stocks also provide the opportunity for capital appreciation should some asset sales eventually be required.

It seems that the alternative to increased exposure to dividend paying equities is much worry over market values and much lower assumptions regarding retirement income.

1 “Rethinking Retirement: Sustainable withdrawal rates for new retirees in 2015,” Wade Phau and Wade Dokken. Published by WealthVest, 8/28/15.

2 “Determining Withdrawal Rates Using Historical Data,” William P. Bengen, Journal of Financial Planning, October 1994.

3 Professor Robert Shiller provides the data used in calculating the Cyclically Adjusted Price Earnings Ratio (CAPE) at his website www.econ.yale.edu/~shiller/data.htm