Duration Issues Related to Seasoned Residential Mortgage Backed Securities

Fixed income practitioners traditionally think of duration as a security’s first-order sensitivity to changes in interest rates. Thus, a duration of X years equates – roughly – to a change in price of X% for every 100bp move in rates. And since the discounting formula for bond prices has this “rate” factor in the denominator, an increase in rates represents a decrease in the bond’s price, and vice-versa. Simple, right? Maybe not!

History of Mortgage Backed Securities

In the early 1980s, the first mortgage-backed securities were developed, and a new securities market as well as a new topic for research departments was born. Since the securities passed-through principal and interest payments of underlying borrowers, the bonds’ duration profiles were more akin to sinking-fund corporate bonds, where principal amounts were repaid along the way to a final maturity date. That would probably not have been too big of a change to the formula/analytics, except for the fact that the amount of principal in each period could change: if borrowers moved or sold their houses, their principal was returned early and the loan obligation fulfilled. If borrowers paid incremental principal in a given period for any reason – known as a curtailment – the principal passed-through in that period would be larger, and this would affect the amount of interest due versus principal applied the next period, shorten the ultimate repayment schedule, etc. Further, if interest rates dropped, borrowers might refinance their mortgages, which would cause still more principal to be passed-through, and if rates rose, the dollar amount of mortgages being refinanced could drop, meaning that principal distribution would slow. “Prepayments,” or the collective bulk of principal from curtailments, refinancing activity, or anything else received outside of the planned amortization schedule, and more importantly, development of a model to forecast the borrower behavior which would impact prepayments, became a focus for trading desks, researchers, investors, banks and servicers.

Progression To Modern Day Securitization Market

Fast-forward a few decades, and securitization of different types of underlying collateral such as adjustable-rate mortgages (ARMs), home equity lines of credit (HELOCs), 2nd liens, hybrid mortgages with fixed and adjustable-rate features, negative amortization allowances and many other types of loans has made modeling even more complicated. And on top of ALL of the above, throw in the housing crisis of the mid-aughts, and basically we end up with one big, huge, modeling and predictive behavior mess. Underlying borrower credit, defaults, recoveries, modifications, things that participants over-assumed or did not consider at all: the whole shabang came to the forefront, and many or most parties across the spectrum from originators to investors were caught off guard.

As we all know, the aftermath has resulted in a many difficult lessons learned. But along those lines, many new investors were attracted to the space, since after “the dust settled” there seemed to be much intrinsic value available to be captured. The sector has experienced significant appreciation as the housing market has recovered, bad borrowers have exited pools via default and good borrowers have remained. Bond offerings today reflect some combination of modeling assumptions, investor forecasts and an “anybody’s guess” component as to where rates are headed. So how do we handle the more traditional measure of duration/price sensitivity to interest rates now, after the borrower pools have undergone so much change?

Methods To Calculating Duration Vary Widely

For the last several years, opinions and methodologies for the calculation of duration for seasoned residential mortgage backed securities (“RMBS”) have widely differed. The prevailing theme has been that seasoned RMBS trade with a profile offering the best of both worlds: if rates drop, the profile is stable enough that they will rally as traditional bonds do, since the cashflows will be discounted by a smaller denominator. If rates selloff, the securities will in fact increase in price as well, because rates will be higher only if the economy and asset prices are growing, and since these are tied to asset prices – homes – their value will be higher.

Others have taken the approach that since many of the securities are floating-rate and adjust on a monthly basis, they can be assigned durations of about 0.1, as the coupon will simply adjust each month and keep up with any increase in rates. Conversely, fixed-rate bonds have been assigned durations reflective of longer obligations, since their interest component will not adjust. And as if all of that is not difficult enough to determine, hedges in the form of corporate credit and interest rate futures are employed, in the hope that their moves they will at least somewhat correspond to the duration “guess” being applied to the specific bonds!

Garrison Point’s Different Approach to Duration

At Garrison Point Capital, LLC (“Garrison Point”) we have concluded, for lack of better terms, that there is not a one-size-fits-all answer, to say the least. There are certainly models which seek to capture optionality presented from the structure, the effect of interest rates on borrower activity, and many other more quantitative measures. But here is where years of experience lend themselves to what is definitely more “art” than “science,” and since we have seen what has happened and can apply our own experience to the process, we feel we can discern the proper duration from our overall framework.

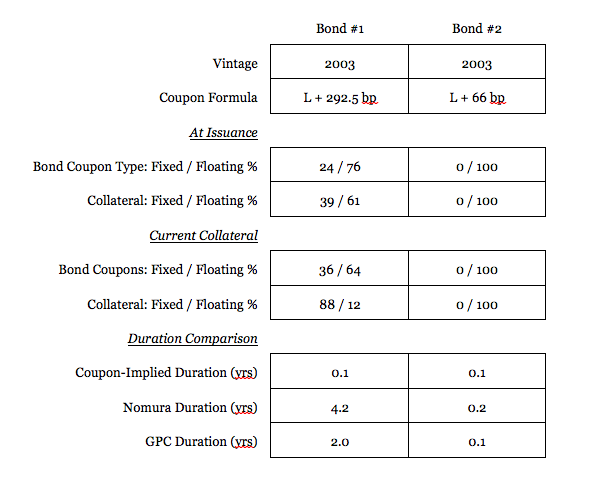

Illustrative Bond Example #1

This is best illustrated by some examples. We recently purchased a 2003-vintage, seasoned subprime mezzanine bond (“Bond 1”). It is one of a stack of mezzanine tranches in the deal, all of which have floating-rate coupons and which provide credit support in a typical “Y” structure. At issuance, the % of floating-rate collateral was basically commensurate with the % of floating-rate bonds, and the same with fixed-rate collateral versus bonds. An interest rate swap was put in place for the deal to (attempt to) cover “all bases” and mitigate any mismatches between collateral type and bond coupon type, ie, fixed vs floating.

But a funny thing happened over the last 12 years: prepayments and defaults cleared out disproportionate amounts of floating vs fixed collateral, and modifications likely changed some loans from floating to fixed as well. As a result, the pool is 88% fixed rate and 12% floating, while the proportion of fixed rate bonds is now only 36% versus 64% floating – quite a mismatch. This could cause problems as interest rates rise, since the floating-rate bonds will be due a higher coupon payment but most of the borrowers in the pool will be remitting interest payments at their same, usual fixed rate. If ever there is insufficient cash available to pay full coupons, a reduction in the payment due to the bondholders could occur based on an Available Funds Cap (AFC). This of course would mean that the various bonds’ coupons would not have fully risen as expected, based on their floating-rate formulae, and thus they did not receive sufficient interest, and thus they should drop in price. If these bonds had been assigned one-month durations, but then in fact experienced a noteworthy drop in price on account of hitting the AFC, the bonds would underperform their duration.

At the same time, we see that other pieces are involved with the valuation of this bond: a sound remaining borrower pool and solid credit enhancement. 35% of the mortgagors made it through the entire time since origination, despite the worst credit crisis of the last 75 years, without missing a payment. All borrowers are now 12 years into their payment history on these loans, and are “still standing” after the crisis. The bond itself has 10% credit enhancement, and is unlikely to take losses. Why or how do those impact credit metrics such as duration? It is possible that there could be AFC issues, but we think an overriding outlook for this bond is that because of the credit story, it will be attractive to buyers who want solid credit, and thus it will move towards par over time. This should counter a wide range of possible AFC-related outcomes.

Many of today’s large broker-dealer models try to account for collateral type composition, i.e., fixed- versus floating-rate underlying loans, and work this into their scenario analysis. Other considerations might be the likelihood of mods in the underlying pool, state of delinquency and number of years of consistent payments. This bond actually appears on the shorter side, at 4.7 years weighted average life (WAL), on one analytics provider’s runs, in a “base case” scenario. We think that the collateral pool will yield a slower profile, which resulted in our own base case of 6.4 years WAL. Since the WAL is related to the timing of principal payments, any duration considerations will be affected as well.

Illustrative Bond Example #2

We can look at an example of a more straightforward situation for additional insight as well. We purchased another 2003 vintage bond, this one a senior floater (“Bond 2”). Borrower credit is higher, at least on a nominal basis, so there are less outside considerations as to collateral versus structure for the duration application. This one has floating-rate senior bonds as well as subs, and even more to the point has 100% ARM collateral. Most of the pool has not been modified, and we do not think this will come into play, i.e., becoming fixed rate loans via mods. Thus, this bond more fully represents a “true” floating-rate bond, as its collateral will adjust, which will support the adjustment of the coupon, and AFC/cap issues are unlikely to come into play.

These two situations show the range of duration issues even for two bonds which have floating-rate coupons. In the first case, the bond could act much more like a fixed bond, and thus duration needs to be longer, whereas in the second, we can be comfortable assigning a low duration reflective of the floating coupon. At Garrison Point we employ several hundred scenarios to analyze securities of this type, and then apply our own experience and trading slant to the analytics, to achieve an effective duration which will represent appropriate risks borne by the overall situation. We assigned a duration of 2 years to the first bond, despite what appears to be a longer cashflow profile; we determined that there would be more price support and sponsorship to that particular bond, even if rates were to backup to levels which might dictate more price loss on an analytical basis. For the second we match most analytical calculators which tabbed the duration at around 0.1 year, or basically, a monthly adjustment bond.

Cross-checking Our Approach to Street Research

To “sanity check” our methodology we discussed these issues with Nomura’s Head of Research, Paul Nikodem. Their systems captured the same effects in the first case, in particular, AFC issues and lengthened cashflows in a backup. While their calculated duration of just over 4 years differed from ours, we captured the same analytical tenets and then revised ours down based on our own trading experience and viewpoint. In that sense we feel that we adequately matched their “science” standpoint, despite differing on the “art.” In the second case, we both arrived at the same conclusion in the sense that the bond’s coupon should float and the price should remain steady in any rate environment, all things considered. Naturally, we are thankful for research counterparts like Paul and Nomura and the chance to navigate these issues with a second set of eyes.

Conclusion

Obviously nobody knows the future, but strict reliance on one set of assumptions and original forecasts alone is also wholly inappropriate for seasoned RMBS trading. Since those original models 30 years ago, econometrics, probability and statistics have all contributed to modifying and refining loan and borrower analysis, prepayment forecasting, and their effects on securities valuation, but at Garrison Point we seek to take the best of all worlds for analytics and research and overlay depth of market knowledge to manage duration and interest rate sensitivity as prudently as possible.