The Federal Reserve released the latest Beige Book on Wednesday which showed a modestly expanding economy. While construction, aerospace and the auto industry led to manufacturing growth, cheap imported substitutes and the strong dollar continue providing headwinds. Retail, tourism and service sectors reported moderate growth. Housing sales and construction continue growing, but low inventory is driving prices higher. The imminent Fed rate increase is pulling some projects forward. The overall trend of loan growth and declining delinquencies continues.

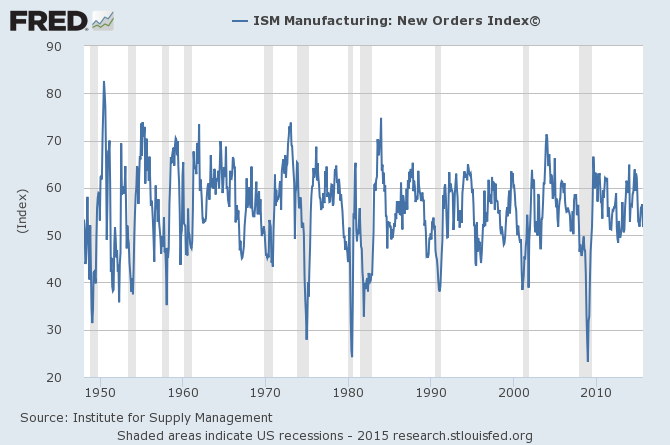

This week the Institute for Supply Management released the manufacturing and non-manufacturing PMI indexes. The manufacturing index dropped 1.6 points to 51.1. Of slight concern was the 4.8 point new orders decrease. But this is a noisy data series:

While the report offers no specific reason for the drop, the strong dollar (see below) and the third consecutive month of sub-50 readings for export orders probably contributed. The anecdotal comments are strong:

- "Falling crude oil prices are benefiting all resin based purchases as well as positively impacting fuel surcharges for inbound products." (Food, Beverage & Tobacco Products)

- "We are oversold." (Paper Products)

- "Business is still strong but has slowed slightly." (Transportation Equipment)

- "Modest growth slightly ahead of GDP. Optimistic for the remainder of the year as we have little international exposure." (Chemical Products)

- "FX [Foreign Exchange] continues to be a challenge, especially in Europe. Overall though, the mood is fairly upbeat regarding H2 [second half of 2015] as we ramp up for a new product launch." (Computer & Electronic Products)

- "Our business is good due to the increase in commercial construction." (Fabricated Metal Products)

- "Raw metals price decreases will impact our business favorably."(Miscellaneous Manufacturing)

- "Business is guarded but steady. Margins are tight. Markets are very competitive. China is lackluster." (Wood Products)

- "Automotive companies are investing heavily in upgrading their equipment." (Machinery)

- "Business is strong and doing well. Labor continues to be a struggle to find." (Furniture and Related Products)

The notes contain only two weak points: transportation orders dropped slightly and the strong dollar continues hurting on exports. Although the headline service number dropped, it remains an impressive 59. Like the manufacturing comments, the anecdotal comments are positive:

- "Overall business is increasing." (Health Care & Social Assistance)

- "Business in commercial real estate and management thereof continues to be strong. Companies want to get out of directly managing brick and mortar structures and the systems that support those assets." (Management of Companies & Support Services)

- "Business is good and do not see anything to slow it down." (Construction)

- "Trending towards a positive year-end." (Finance & Insurance)

- "Avian influenza has impacted the egg market taking 40 percent of the raw material out of the supply chain. Prices have doubled and shortages of liquid eggs have emerged." (Accommodation & Food Services)

- "Some slowdown in business activity mostly due to vacations. Despite this, the variance still meets Q3 forecasted business level expectations." (Professional, Scientific & Technical Services)

- "Business and our market sector continue to be strong with continued growth and stability." (Retail Trade)

- "Sales continue to increase and port congestion on the East Coast is easing up. Intermodal transit time has increased by two days because of rail repairs." (Wholesale Trade)

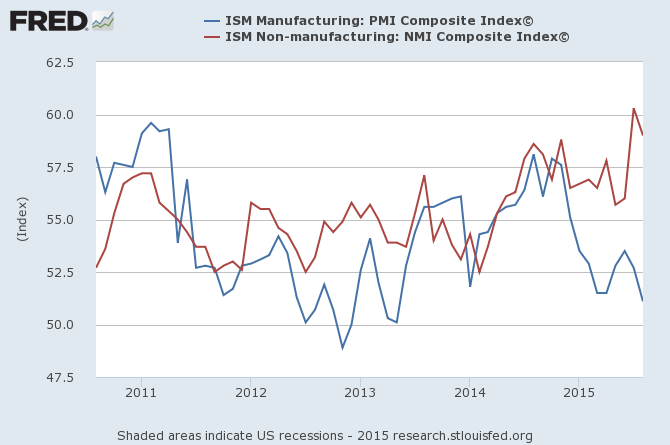

All sectors except the egg industry noted strength. The indexes activity and new order numbers both printed above 60. As this graph shows, service sector strength currently counter-balances manufacturing weakness:

The BLS reported job gains of 173,000 in August, which compares to a 216,000 average rate for June and July. The strong dollar and weak energy sector most likely caused the decline. Manufacturing jobs – which produce exports and oil and gas machinery -- decreased 24,000. Oil industry layoffs totaled 100,000 this year, which partially explains August’s weaker growth in professional/business service employment. Earnings growth remains weak, up only 2.2% Y/Y. But the BLS revised June and July higher by 44,000 and there are reasons to believe the same will happen in the next few months.

Economic Conclusion

With the exception of strong dollar and oil sector weakness, the Beige Book again reported the US economy expanded “moderately.” Both ISM numbers support this conclusion: manufacturing remains positive but slowed due to oil prices and a decline in export orders while the service sector more than offset manufacturing weakness. Although the BLS reported a weaker than anticipated jobs numbers, there’s a decent possibility we’ll see upside revisions in the coming months, as per the June and July 44,000 upward revision. So far, the US economy remains mostly insulated from Chinese weakness.

The Markets:

Recent price action did a fair amount of damage to the daily SPYs chart:

The MACD and RSI declined over the last 12 months, indicating the market merely needed a selling catalyst. Prices are now below the 200 day EMA – bear market territory. They are also below all EMAs, which will continue pulling them lower. The 10 and 20 day EMA dropped below the 200 day EMA and the 50 is about to crossover. “Death Cross” hyperbole notwithstanding, this is an unwelcome development for the bulls. The market closed below the support levels between 195-197 and 202-204. The only good news is the possible formation of a consolidation triangle comprising the last two weeks price action. The declining volume somewhat confirms this, but, given the extreme recent volatility, we’ll need further confirmation.

The advance decline lines confirm bearish sentiment:

Both the NYAD (top chart) and NAAD (bottom chart) are declining; the former since May and the latter since June.

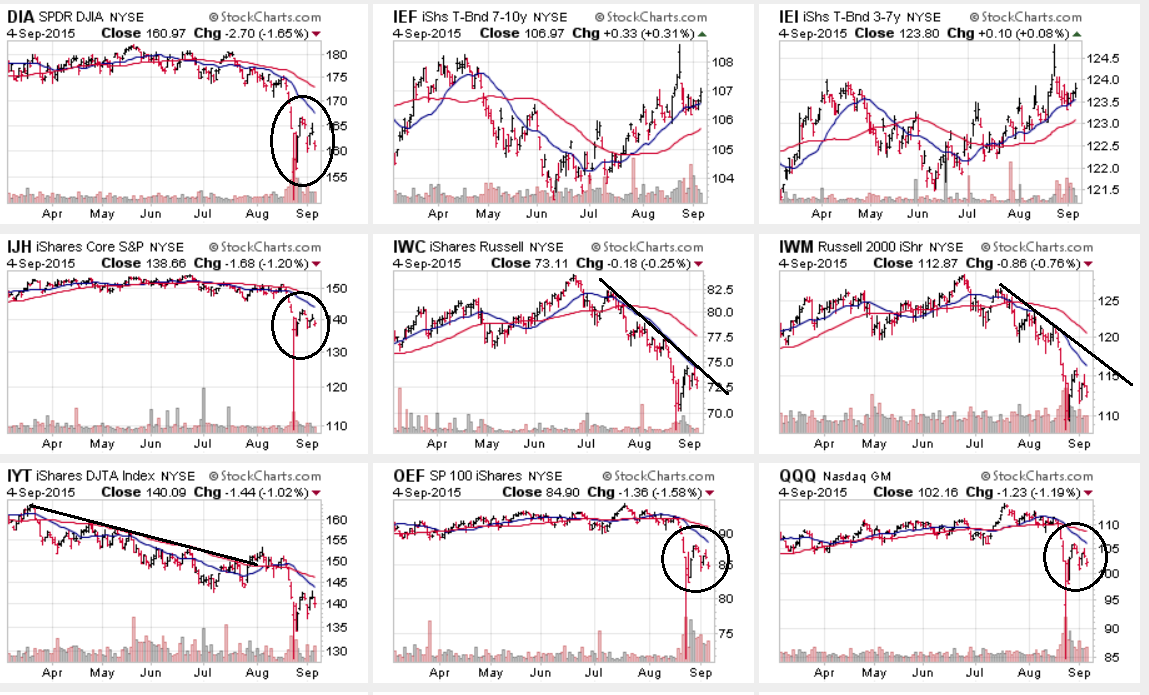

And no other average is providing any bullish indicators:

The DIAs, IJHs, OEFs, and QQQs continue consolidating below the 200 and 50 day EMAs while the IWCs, IWMs and IYTs each remain in a downtrend. Put more generally, averages comprised of larger companies are potentially stabilizing at lower levels, but averages comprised of growth companies (a good proxy for equity risk capital) continue moving lower. Finally, the averages remain expensive: the current and forward PEs for the SPYs and QQQs are 20.35/21.35 and 16.55/21.60, respectively. Weak top line revenue growth – even ex-oil – persists. And thus far, 3Q projected GDP growth projections disappoints:

Market Conclusion

Overall, the bears currently control the market. Risk based capital is fleeing higher beta indexes and treasuries have moved higher. Negative Chinese market and economic events lead traders to sell at a moment’s notice. Companies are barely growing top line revenue, which is starving an already expensive market of much needed earnings growth. In this environment, a move through previously established highs seems a remote possibility.