The Federal Reserve’s rate-setting committee meets next week, and there is more uneasiness than usual surrounding the event. Much has changed in the past few weeks, and the Fed’s likely course of action is being examined from a multitude of angles. Buried in this discussion is the fact that U.S. economic activity is, for the most part, intact.

Real gross domestic product (GDP) grew 3.7% in the second quarter, following a 0.6% increase in the first three months of the year. The second half of the year should show a more-even performance.

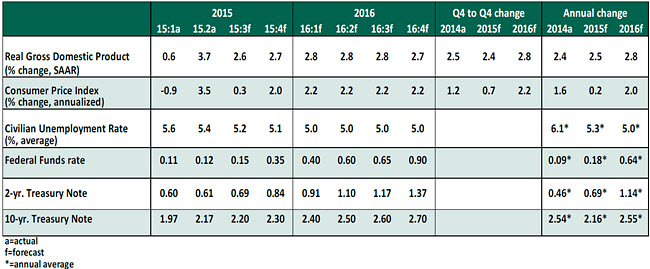

Key Economic Indicators

Key Elements of Forecast:

- Consumer spending accelerated in the second quarter (3.1% versus 1.8% in the first quarter). Auto sales rose to an annualized 17.8 million mark in August, the highest in 10 years. The recent decline in gasoline prices should boost consumer spending. It is unclear if the latest drop in equity prices will offset positive factors supporting consumer spending; much will depend on whether the stock market regains its footing in the coming weeks.

- Overall, the housing market is strengthening. Existing homes sales advanced in July to a new expansion high (5.6 million units on an annual basis). On the supply side, the inventory of existing homes continues to shrink. Sales of new homes also moved up in July to an annual pace of 507,000, but there were downward revisions to past estimates. Housing starts advanced to a new cycle high. The strength of the labor market suggests that home sales and building activity are likely to maintain the current forward momentum.

- Revisions to second-quarter GDP data contained upside surprises for business spending. The weakness in oil and gas industry spending, which we are monitoring closely, has yet to show signs of stabilization. Shipments of non-defense capital goods are an important input for equipment spending in national income accounts. The increase in shipments of non-defense capital goods during July bodes positively for third-quarter equipment spending.

- The U.S. economy is near full employment. The jobless rate (5.1%) is within the range of the Fed’s estimate of long-term unemployment. Despite its flaws, the civilian unemployment rate is the single best indicator of slack in the labor market. By this measure, the labor market is tightening, and wage pressures should be around the corner. Hourly earnings firmed in August, with the largest monthly increase since January. But the underlying trend remains far below historical norms at the current stage of the business cycle. Anecdotal reports suggest that employment compensation is moving up in some industries.

- Inflation readings are holding stubbornly below the Fed’s 2.0% target. The recent drop in oil prices implies overall inflation readings are not likely to approach the target in the near term. Core inflation (excludes food and energy) numbers are also below the Fed’s target rate. Housing costs continue to march higher and could put upward pressure on inflation in the months ahead.

- Economic weakness in China and a fear of the global ramifications haunt financial markets. This is a very important factor that continues to influence 10-year U.S. Treasury note yields. As markets stabilize and come to terms with the fact that the Chinese economy is shifting to a lower gear, U.S. economic fundamentals should once again determine yields of Treasury securities.

- We continue to view that there is a chance the Fed will commence tightening at the September 16-17 Federal Open Market Committee meeting. That assumes market developments do not turn unfavorable in the next few days. Fed rhetoric suggests they may err on the side of caution. Regardless of the Fed’s decision, the key is the path of the federal funds rate in the months ahead and not the timing of the first hike. In this regard, Federal Reserve officials have telegraphed that a gradual tightening of the policy rate is appropriate.