Newsletter - September 2015

WALKING DOWN THE STREET IN LONDON

Returning from Iceland, we spent a few days in London. On the way to a play, Deena and I passed a few billboards that really resonated with us as they so closely parallel the spirit and beliefs of Evensky & Katz:

• Turn a profit not a blind eye

• Consequences - Possibly the least used word in the investment world

• Making money has side effects - you control what they are. We like turning your money into more money, but not at any cost.

• Invest for the unknown, not in it

LACK OF PLANITIS

• Excessive worry

• Trouble sleeping

• Poor mental wealth

• Fear you'll have to work forever

• Having to move in with your kids

REALLY DEPRESSING

Investment News headline:

“Bipartisan lawmakers in the House of Representatives are trying to stop a Labor Department rule that would require brokers to act in the best interests of their clients when working with retirement accounts.” Go figure.

WONDER WHAT EVER HAPPENED TO “ABSOLUTE RETURNS?”

From the Wall Street Journal via MarketWatch:

Stock rout hits hedge-fund yearly gains hard

Hedge-fund managers like to promise their investors protection from market swings. In the recent stock swoon, many were caught off guard.

Billionaire managers such as Leon Cooperman, Raymond Dalio and Daniel Loeb are deeply in the red this month, left flat-footed by the quick plunge for stocks worldwide. Cooperman’s Omega Advisors posted a 12% decline this month through Wednesday and 10% this year. Loeb’s Third Point LLC and William Ackman’s Pershing Square Capital Management are also down big, erasing their gains for the year.

GREAT QUOTE

From an executive at a tech company when asked about the future of the computer business: “I’m too smart and I’m too dumb to predict the future.” I think I’ll use it next time a reporter asks me about my prediction for the market next year.

SABOTAGE IN YOUR IRA

I’ve written on numerous occasions about the Department of Labor and the fiduciary debate but I thought these comments by Senators Warren and Booker might help clarify the issues.

It's hard — really hard — to save for retirement. And the stats bear this out: Almost onethird of Americans on the edge of retirement have zero savings. Another third have saved less than one year's income.

That's why it's important to protect every dollar that someone puts away for their retirement. Many Americans rely on investment advisers for guidance on how to save towards retirement, and most advisers have savers' best interests at heart. But not all advisers put their customers first — and that's created a hole that's draining $17 billion in retirement savings every year, money that's going to some investment advisers who are more interested in collecting fees for themselves than helping families build real security.

Thankfully, the hole may soon be plugged. The president and the Department of Labor are meeting with stakeholders and the public to finalize new rules that would require the people who advise customers about IRAs and other retirement savings options to keep the best interests of the customer as their first priority. These proposed rules are still being perfected, but they are a strong step in the right direction.

Today, if employers offer retirement options at all, it's most likely through 401(k)s and IRAs, which put families in charge of ensuring their own returns through a series of often-complex accounts. Instead of a handful of experts managing a company's pension, this shift means that families must rely on retirement advice from financial advisers and brokers.

Most retirement advisers recommend investments that work best for the customer. They work together with their clients to help them reach their retirement savings goals. But some don't. These advisers and brokers recommend investments that boost their own profits through fees and bonuses, while the value of the customer's savings are eroded over time. Some recommend investments in return for being rewarded with free vacations, cars, jewelry, or other perks that the adviser can earn from selling a more expensive product to the customer — one that is plainly not in that customer's best interests. [Good point, it’s not most brokers, it’s the system that lets the bad ones get away with it.]

Because of outdated laws and loopholes big enough to drive a truck through, it is now perfectly legal for brokers and advisers to take payments and boost their own incomes by pushing lousy products. Most customers aren't on the lookout for unscrupulous retirement advisers.

Even if the percentages seem small, over time costs compound to become big numbers. People working hard to put away money lose an estimated $17 billion a year to excess fees. Even a 0.75% increase in fees could cost a retiree over $100,000 in savings over a career. That's a lot of money to lose.

This loophole is also unfair to the thousands of honest advisers and brokers who put their clients first and work hard every day to help Americans build a secure retirement.

Right now they have to compete against unethical advisers who rake in money just for themselves. That's not a level playing field — it's a broken system. It's time to fix it.

While several industry leaders have stepped out in support of a rule, many of those who benefit from maintaining the status quo are arguing that the industry can police itself, that the Securities and Exchange Commission should regulate retirement advisers instead of the Department of Labor, and that requiring advisers to disclose conflicts of interest should suffice. But none of these arguments pass the smell test: the retirement industry and the SEC could have fixed this problem years ago, but failed to do so — resulting in lost billions for today's retirees. The Department of Labor, which has clear authority to act, has stepped up. It's about time.

Middle-class families face many challenges trying to save for a secure retirement, but high fees and hidden payments shouldn't be among them. Hard-working Americans who manage to scrape together some savings for their retirement should be able to trust that their advisers are working for them — not against them.

LOVE and MARRIAGE

From REP magazine

• Factor by which the risk of early death is higher across a lifetime for single men and women compared to married men and women, respectively …..32%/23%

• Estimated number of years that the average married man outlives the average unmarried man in the U.S. …..8 to 17 years

• Factor by which people who get married and stay married accumulate more wealth after 15 years than single or divorced people do in that period ……4

• Cost of the average American wedding in 2014 ….$29,848

• Cost of the average wedding in New York City ….$86,916

TALK ABOUT A HOBBY

Here’s how Nathan Yau explained why he recreated the Statistical Atlas of the United States. “Ever since I found out about the Statistical Atlas of the United States, historically produced by the Census Bureau, it annoyed me that there wasn't one in the works for the 2010 Census due to cuts in funding. The last one was for 2000. Actually, the 2000 edition was called the Census Atlas.

The first Atlas, by Francis A. Walker, was published in 1874 using the data from the prior 1870 Census. Counting cover, credits, and all that, it was 56 pages. I got to thinking, hey, I could do that. And if I did, I wouldn't have to be annoyed anymore. So I recreated the original Statistical Atlas of the United States with current data. I used similar styling, and had one main rule for myself. All the data had to be publicly available and come from government sites.

Here’s where you can find the complete file. I didn’t count but there are dozens and dozens of fascinating maps.

http://flowingdata.com/2015/06/16/reviving-the-statistical-atlas-of-the-united-states-with-newdata/

Thanks to my associate Clay for telling me about it.

WE’RE NOT THE ONLY ONES

We occasionally get asked about the changes in our long-term market return assumptions. Unfortunately, the future is uncertain. We’re always looking forward (not backward) and have an obligation to make changes when the world changes. We’re in good company; all professionals do. For example, Northern Trust’s recent Investment Strategy Commentary reported, “…our developed-market equity total return forecast [5-year] of 6.1% (versus last year’s 7.2% expectation).

BOB’S BLOG

http://bobkronish.blogspot.com/

My friend Bob’s blog incorporates in-depth columns on a single major issue with wide ranging subjects from investing, to politics, to government measures, to economics.

Just in Case You Missed It

Greed: Getting Grimmer and Grimier

In early January, the CFA Institute issued a report on a survey it conducted with its members on the state of the financial industry. The results are disappointing. For example: “It's clear that recent scandals and the regulatory reforms they provoked have not sufficiently changed how some participants in the financial industry conduct their business. As participants in that industry, we're doing the public – and ourselves – an injustice if we write the litany of scandals off “as just a few bad apples" or even worse, as the price of doing business.”

Grimmer

The report then claimed, ”We are making it too easy for the public to equate the finance industry with self-dealing, dishonesty and corruption. Trust, not cash, is the fuel that makes the financial system function, and when investors, big and small, start to regard the system as one rigged against them, the risk of collapse will never be far away.”

Grimier

The survey also found, “The greatest area of concern for the health of the global economy, however, remains the same as it has year after year: the lack of trust in the industry. Over half of our members (63 percent this year, up from 54 percent last year) blamed this on a lack of ethical cultures within financial firms, suggesting the problem stems more from flawed (unethical) internal firm culture than from poor government regulation and enforcement [Hello Gordon Gecko!]. Nor are members seeing any improvement in the level of integrity of global capital markets, with a majority expecting the state of integrity in 2015 to stay about the same as its level in 2014.”

TRAVEL TRIP

According to CheapAir.com via AARP, the best time to book domestic flights is 47 days before takeoff and the cheapest day is Tuesday. For Latin America it’s 96 days, Europe – 276 days and Mexico – 251 days.

GURUS

Alternatives and hedge funds sound sexy and sophisticated but they are not for the fainthearted. At the top of the heap is (or at least was) the Carlyle Group. According to a 2015 ranking called the PEI 300 and based on capital raised over the last five years, Carlyle was ranked #1 as the largest private equity firm in the world.

Fast forward to late June this year when the headline in the Wall Street Journal was “Investors Warned on Carlyle Fund Unit.” The story went on to say “It wasn’t clear why Cliffwater [a consultant] made its recommendations, though the move followed a 4.9% loss in June by Claren Road’s flagship fund [Carlyle’s hedge-fund firm] and a 10% loss by the fund last year [vs. 13.7% for the S&P 500].

BIG MONTHS

July 26 - 25th anniversary of the Americans With Disability Act

July 30 – 50th anniversary of Medicare and Medicaid

August 1 – 80th anniversary of Social Security

August 19 – Beatles kick off their first U.S. tour 51 years ago

Thank you AARP Bulletin

WHAT’S NEXT? NO KRISPY KREME?

PLEASED AND PROUD

Evensky & Katz/Foldes Financial was listed in the Financial Times 300, “The FT300 top registered investment advisors in the US.” There were only 14 in Florida and 4 in Miami.

THE FUTURE IS NEAR

From my friend Rick:

https://www.youtube.com/watch?v=Vj2kuZm-aCA&feature=player_embedded

Based on the work of a team consisting of a biologist, physicist, chemical engineer and microbiologist at Columbia, this video explains the extraordinary potential of Renewable Energy from Evaporating Water.

IT’S A GOOD GIG

From my friend Skip, brokerage firm payout grids: http://www.onwallstreet.com/global/payout_grids.html

FROM THE INDUSTRY THAT COMPLAINS REQUIRING A FIDUCIARY STANDARD WILL MEAN SMALL CLIENTS DON’T GET SERVED

From the Wall Street Journal

“Merrill Lynch Wealth Management next year plans to tweak its financial advisers’ compensation to push them to continue shedding smaller accounts, while offering bigger payouts on client-asset growth.”

“Advisers with affluent clients--or those with more than $250,000 in assets--consisting of 80% or more of their book will receive a 20% payout on smaller accounts. But those that don’t meet that book threshold won’t receive any compensation for so-called mass affluent clients. Previously, Merrill didn’t distinguish client sizes among existing accounts when calculating an adviser’s payout.”

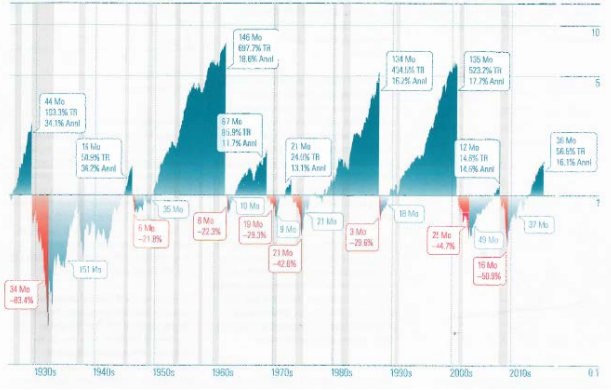

HISTORY

Of Bull Markets from Morningstar Markets Observer

INTERESTING (SCARY?)

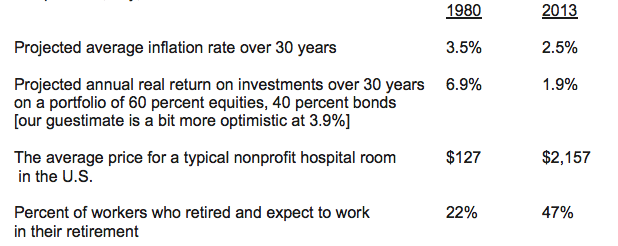

From Money Magazine’s Retirement Then and Now, “How did 2013 stack up for retirement compared to, say, 1980?”

THE SHOCKING TRUTH MUTUAL FUNDS DON'T WANT YOU TO KNOW From Forbes…

“The vast majority of mutual funds have more in common with one-hit wonders than they would want you to know. The shocking truth is that most mutual funds that rank in the top performance quartile one year don’t do it again the next year nor the following year. And no funds stay in the top quartile over five years. Even worse, about a third of mutual funds die or get merged with another after five years.

Among 682 domestic stock funds whose performance ranked in the top 25% of their peer groups in 2013, only 5% managed to stay in the top quartile in March 2015. That’s according to S&P Dow Jones Indices’ Persistence Scorecard released Tuesday. Only 4% of large-cap funds, 5% of mid-cap funds and 5% of small-cap funds that ranked in the top quartile stayed at the top.

Among the funds that ranked in the top half among their peers for the three years ended in March 2015, only 17% of large-cap funds and 17% of mid-cap funds managed to stay in the top half. Small-cap funds were slightly more persistent. Some 23% of small-cap mutual funds held their ranking in the top half over three years. In a randomly selected universe of mutual funds, you would expect 25% of funds to rank in the top quartile over three years.

Only 5% of large-cap funds, 3% of mid-cap funds and 8% of small-cap funds managed to rank consistently in the top half over five consecutive years.

Random expectations would suggest a repeat of the 6.25% result from the previous period,” Aye Soe, senior director of global research and design at S&P Dow Jones Indices, wrote in the report. “No large-cap, mid-cap, or small-cap funds remained in the top quartile at the end of the five-year measurement period. This figure paints a negative picture regarding the lack of long-term persistence in mutual fund returns.”

Now you know why we spend so much time doing research on the funds we utilize for our clients.

http://www.forbes.com/sites/trangho/2015/06/23/the-shocking-truth-mutual-funds-dont-wantyou-to-know/

SPEAKERS BEWARE

You’re speaking at an event and get up and say, “Can you hear me in the back?” A guy says, “No.” And a lady up front says, “I can. I’ll trade places with you.” Senator Robert Dole in the AARP Bulletin.

I now know not to ask that question when I’m speaking.

GLOBAL IS REAL

Fidelity Investments reported that as of December 31, 2014, 75% of the world’s publically traded companies are located outside the U.S.

GOOD STUFF

On Open Culture you can find a Master List of 1,150 free courses from top universities: 35,000 Hours of Audio/Video Lectures. 133 free philosophy courses, 85 free history courses, 120 free computer science courses, 71 free physics courses and 55 free literature courses in the collection, and that’s just beginning to scratch the surface. You can peruse sections covering Astronomy, Biology, Business, Chemistry, Economics, Engineering, Math, Political Science, Psychology and Religion.

TRUTH? IN ADVERTISING?

From my friend and respected professional guru’s Newsletter (Michael Kitces’ The Nerd’s Eye View). https://www.kitces.com/blog/9-out-of-top-10-cnbc-fee-only-advisory-firms-not-actuallyfee-only-according-to-cfp-board-compensation-disclosure-rules/

“Earlier today, CNBC released its second annual list of the ‘Top 100 Fee-Only Wealth Management Firms’ to the public. In cultivating the list, CNBC noted that consumers should ‘make sure you understand how that [advisor] gets paid, and that means [understanding] fees vs commissions’ and that ‘fee-only financial planners... do not accept any commissions or other compensation based on product sales.’ Independent RIAs were then ranked based on a ‘proprietary formula’ including assets under management, having staff with professional designations like CFP or CFA, average account sizes, growth of assets, years in the business, and comprehensiveness of advice (even on insurance solutions).

Yet a deeper look at the Form ADV Part 2 disclosures of just the top 10 firms on CNBC's ‘fee-only’ list reveals that 9 out of 10 of them share in insurance commissions, own an insurance agency, or are under common ownership alongside an insurance affiliate to which advisory clients are referred. In other words, 9 out of 10 of CNBC's ‘Top Fee-Only’ firms would not actually be fee-only under the CFP Board's compensation disclosure rules.

Notably, the CNBC list does focus exclusively on registered investment advisers (RIAs), and in most cases the RIA firm does not receive any insurance commissions directly (though it does happen in at least one situation, as RIA status does not technically ban commissions). Nonetheless, in 9 out of 10 cases, the RIA does have a clearly related entity or relationship that generates commissions - to the point that ironically, those ‘fee-only’ firms themselves actually disclose those commissions and the conflict of interest it creates in their own Form ADVs!”

Caveat Emptor!

WHAT? ME WORRY?

As I’m a bit late in getting this issue out I can’t ignore the exciting recent market events, so here are a few items.

• First and foremost, our clients get an A+ for remaining so calm and collected. As one family wrote (republished with their permission), “Thank you for the e-mail. We are in XXX, have been watching CNN in between operas, galleries, and other positive experiences, and are not panicking. Somebody on air quoted Bogle on the order of ‘You shouldn't be doing daily agonizing anyway,’ and we haven't been. We very much appreciate your being in touch, and we reiterate that we are in for the long haul. Our immediate goal is going to tonight's opera.”

Of course no one was happy. As her spouse added, “I will echo XXX but would prefer the market go up instead of down.”

• A tweet I saw … “Did your robo-advisor give you a robo-call today to talk about the market?”

WHO KNEW

According to an excellent story, “Cut the Cost of College Tours,” in Money Magazine, “The price of skipping the tour [due to the cost], though, can be higher: not getting in. Three out of four schools say ‘demonstrated interest,’ such as visiting campus, meeting an admissions officer, or at least calling, is considered in admissions, according to a 2012 National Association for College Admission Counseling survey.”

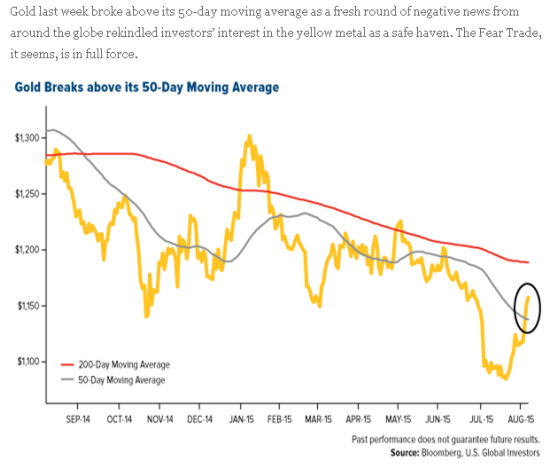

ALL THAT GLITTERS

From Frank Talk. While I agree with the observation that the Fear Trade is in full force, this seems a bit optimistic to me.

CHECK IT OUT

Two most excellent whiteboard videos prepared by two of our most excellent associates – Michael Walsh & Clay Ranck:

https://www.youtube.com/watch?v=dzyPMldzssw – How will I be able to meet my expenses when I retire?

https://youtu.be/t8EeyR2wvWk - What’s your financial story?

HARD TO IGNORE

Kind of hard to ignore the elephant in the room (i.e., recent market volatility), so I thought I’d close by sharing a few recent headlines

Good luck market timers.

All my best,

Harold R. Evensky, CFP®, AIF®

Chairman

Evensky & Katz / Foldes Financial Wealth Management

© Evensky & Katz / Foldes Financial Wealth Management

© Evensky & Katz / Foldes Financial Wealth Management