In the Bible, Jesus said, “I am the Alpha and the Omega, the first and the last, the beginning and the end.” While Jesus infers that he is at both the beginning and the end of time, we as investors can only operate in the present with a knowledge of what has come before. To better understand today's commodity market circumstances, we believe investors should examine the herd mentality and the psychological backing that may lead to contrarian investment opportunities.

As contrarians, we believe that booms don’t end in anything but a bust. Historically, the excitement at peaks is too much for investors to resist. In 2011, we viewed commodities as an end all to institutional and individual investors of the world (to refresh read “Dot-Commodities”). We believe China was an intoxicating conversation to the investment community and the belief in a small group of people deciding the economics of a multi-billion person population was “oh so the rave.”

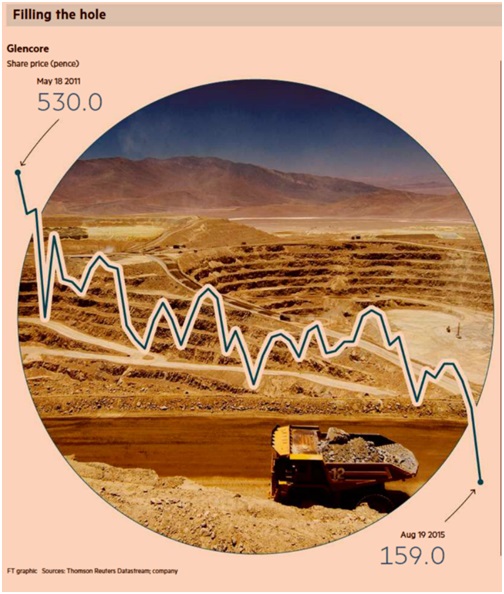

As this excitement raged in 2011, a reputable commodity producing and trading firm by the name of Glencore went public. It was a truly magnanimous IPO in the commodity world with the great story line of partners pouring in blood, sweat and tears over decades, culminating with a liquidity event for publicly-traded shares on the London Stock Exchange, the non-US epitome of status. Back then, we viewed this as a watershed event in the popularity of commodity-related investments.

The Wall Street Journal highlighted the enthusiasm in 2011 in an article titled “Glencore IPO Moves to Next Test.” The article noted that “A loyal and supportive shareholder base would enable Glencore and its chief executive, Ivan Glasenberg, to use equity later on for acquisitions and other expansion projects.” It further noted, “Mr. Glasenberg has made no secret of his desire to expand the company's scope. At the top of his agenda is to fully acquire Xstrata PLC, which Glencore helped build into a $70 billion mining colossus and in which it already holds a 34% stake.” The Xstrata deal culminated in 2012 for $41 billion.

What the wise man does in the beginning, the fool does in the end

On the morning of August 20, 2015 we were skimming through the Financial Times and found a cacophony of articles that began to pull the plug on the accolades of 2011. Below are titles and excerpts from that day’s print of the paper:

Glencore shares plumb new depths”: Equities fall 70% since IPO price

Against a challenging backdrop for many of our commodities we have taken a range of pre-emptive actions in respect of our balance sheet, operations and capital spending in order to preserve our current credit rating,’ Ivan Glasenberg, chief executive, said in a statement.

Pre-emptive actions come about when the animals are already out of the barn. The media always seems to explain that after the fact.

“FT BIG READ. CHINA”

Facing an economic slowdown, Beijing has found that its once-reliable tools to stimulate growth are losing their power. With policy options running low, its leaders broke an old taboo and devalued the renminbi.

There are scores, if not hundreds of ‘ghost cities’ across the country. It seems perverse that developments such as these should exist in the world’s most populous nation...

“Glasenberg apportions blame as Glencore sinks”

…Trading is not as large a problem for Glencore as its exposure to the downturn in a mix of commodities. This has provided the stiffest test yet of the logic its 2013 takeover of miner Xstrata…

In two years, Glencore’s share price decline has effectively wiped out the whole market value of the Xstrata deal.

The Wall Street Journal mirrored these stories with titles like “Bad Bets Sock Mining Giant”, “Why China’s Yuan ‘Reform’ Merit Skepticism,” “On the Brink: Oil Nears $40 Mark” and “Commodity-Exporting Countries Hurt as Prices, Currencies Plunge.”

What happened to the “loyal and supportive shareholder base” from 2011’s IPO? Why were they not more critical of the Xstrata deal that now looks to be valueless? Only the Alpha and Omega can perfectly know these tipping points in the pendulum of time as it pertains to investments. It must be noted that the media can do a great job of telling which extreme of the pendulum you are getting close to (in a contrary way, of course).

The Smart Money Buyer Near the Bottom

Our discipline has also taught us that there are some smart money investors that tell you a great deal about where you are in the pendulum. Exceptional money managers like Warren Buffett and Bill Miller are in this group, along with the officers and directors of publicly-traded companies, as well as a few other wealthy investors we admire. One firm that we admire very much, Oakmark Associates, has amassed a 4.5% stake in Glencore and is now the largest institutional owner of the company. This firm’s track record speaks for itself.

We have all been in a situation where we have been blistered and excoriated while historically astute investors are backing up the truck on their stock and buying in the open market. Being early and losing money initially on a company that may make you multiples on what you invested could be a great problem to have. Once again, only the Alpha and Omega knows this in advance. At Smead Capital, we wait patiently for these kinds of circumstances to show up in publicly-traded common stocks.

Adding it all up

The commodity world has become more contentious and is viewed to be riskier by individual and institutional investors. Smart money investors are buying stocks in the arena. What else do common stock investors need to be aware of?

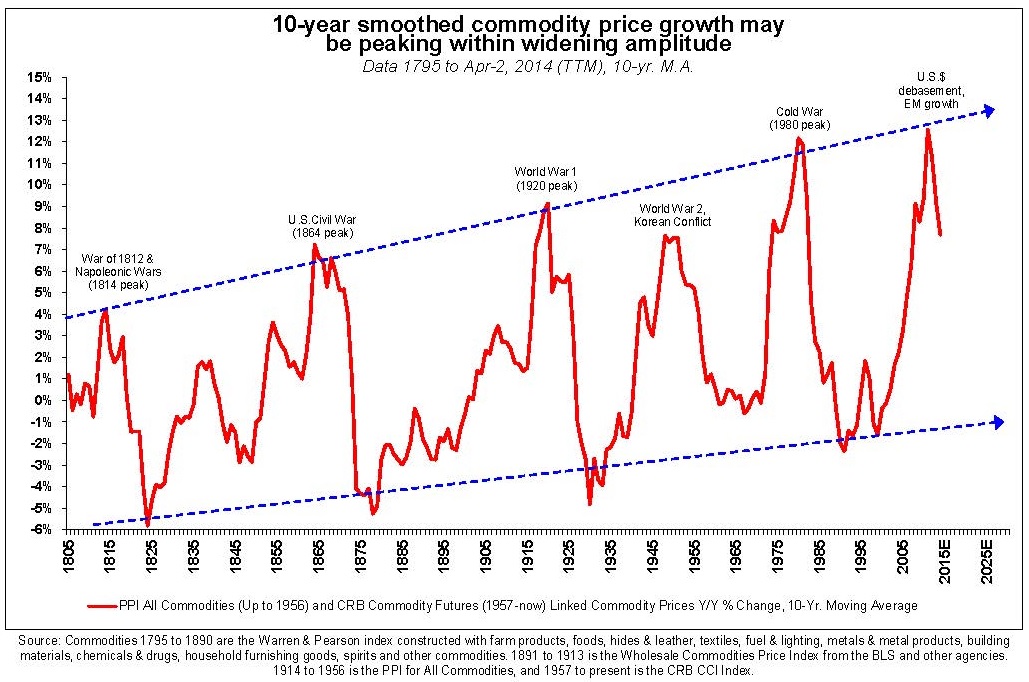

Despite these good circumstances, we must remind investors that picking the winners and losers in thecommodity industry is incredibly tough. To the right is a chart of the 205-year 10-year rolling return of broad-based commodities. We believe the prolonged price swings for businesses in this arena are torturous in comparison to other industries and sectors. Broadly speaking, many of the businesses in this arena boom for 10 years and then see the stock price go dead for another 10 to 20 years before the positive cycle begins again.

We believe most companies dealing in raw materials and cyclical industries are capital-intensive, produce inconsistent free-cash flow, and require more of an Alpha and Omega level of wisdom. Bloomberg just reported on Sunday, September 6th, 2015 that Glencore was seeking to sell assets and raise new equity to curb its debt, including eliminating their dividend: “By suspending its dividend Glencore has taken the risk of alienating investors who have traditionally viewed mining companies as safe bets.” Glencore’s dominant position in a very tough industry, that was perceived at one time to be “safe,” highlights how careful investors must be in an arena like commodities. At Smead Capital Management, we know our spots and these are tougher ones.

If we can find businesses that fit our eight criteria in the commodity-related investment arena, we want to find big discounts in the price of these businesses in relation to what we believe they are worth. If we can’t find those businesses, we will continue to cheer from the sideline for the companies in our portfolio and let the rest of the marketplace compete with the Alpha and the Omega.

Warm Regards,

Cole Smead, CFA

The information contained in this missive represents SCM's opinions, and should not be construed as personalized or individualized investment advice. Past performance is no guarantee of future results. Cole Smead, the Managing Director, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. A list of all recommendations made by Smead Capital Management within the past twelve month period is available upon request.

This Missive and others are available at www.smeadcap.com.

Follow us on Twitter @SmeadCap