If you think equity markets are more volatile this year than in recent years, you aren’t imagining things. In the U.S. market, 24% of trading days have seen a move of 1% or more, compared to just 15% of the days in both 2014 and 2013. We’ve now experienced corrections in most stock markets of 10% or greater, after an extraordinary period of calm. It is our current view that the market downturn is more likely a correction than the start of a new bear market. We think the concerns started with China’s slowing growth, and have increased due to concerns over the lack of “dry powder” at developed market central banks with monetary accommodation already viewed to be near its limits. However, when we examine the internals of market action, we do not see worrying signs out of the fixed income markets. In addition, our discussions with company management teams highlight steady growth in the developed markets but continued mixed trends (strong consumer, weak industrial) in the emerging markets. The current heightened volatility could easily continue – later this week we will receive the August U.S. non-farm payroll report, the last major data point before the Fed meets on September 17. As our outlook for global growth has moderated, we have reduced our recommended tactical risk substantially over the last 10 months, moving to a roughly neutral risk position in July 2015. A major shift in our assessment of the global economic cycle would be the most likely catalyst for us to either further reduce risk or to recommend an increase in risk positions.

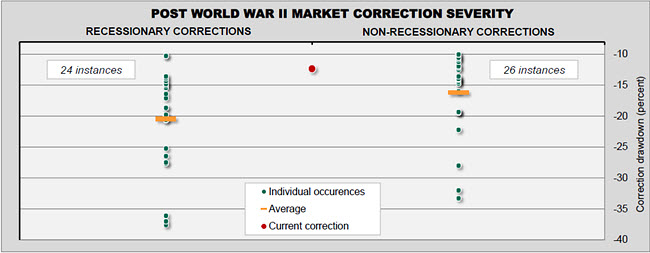

EXHIBIT 1: CORRECTIONS ARE MORE SEVERE IN RECESSIONS

Sources: NT Investment Strategy, Bloomberg, Ned Davis Research, NBER. Current correction 5/21/15 - 9/1/15. Recessionary correction = economic recession occurred during correction or during six months after trough.

Exhibit 1 shows the history of corrections in the U.S. market (using the S&P 500 Index) post World War II. The average correction (defined as a decline of at least 10%) in non-recessionary periods was 16%, while it was 21% in recessions. In addition, bear markets (declines of at least 20%) occurred in 38% of the recessionary corrections, but just 15% of the corrections that occurred outside of recessions. The current correction has lasted 103 days, versus an average duration of 138 days. Interestingly, recessionary corrections have lasted an average of 164 days while non-recessionary corrections have been shorter at 115 days. Recoveries also take much longer from recessionary corrections, as the market has taken 22 months to reach prior peaks after recessions but just 9.5 months after non-recessions. Relatedly, we have seen a spike in volatility as captured by the CBOE Volatility (VIX) Index. In our study of volatility last year (see “Mood Swings,” Investment Strategy Commentary, November 11, 2014) we showed there is little correlation between starting volatility levels and subsequent 12-month returns in the stock market. However, every time the VIX index exceeded a level of 40 in the past the markets generated a positive return over the subsequent 12-month period. The VIX index has exceeded 40 seven times over the last 25 years, with the most recent episode occurring on August 24, 2015.

Given the fact that market corrections are more severe in a recession, and a bear market much more likely, a review of the current growth outlook is in order. In Exhibit 2 we show the Citigroup Economic Surprise Index, which measures data surprises relative to market expectations. A positive and rising number means the studied economy is gaining steam relative to market expectations. We think it is important to look at current data in the context of one of our long-term themes – the Slow Burn of Low Growth. Due to high debt levels, worsening demographics and maturing emerging markets, global growth is likely to remain sluggish over the next five years.

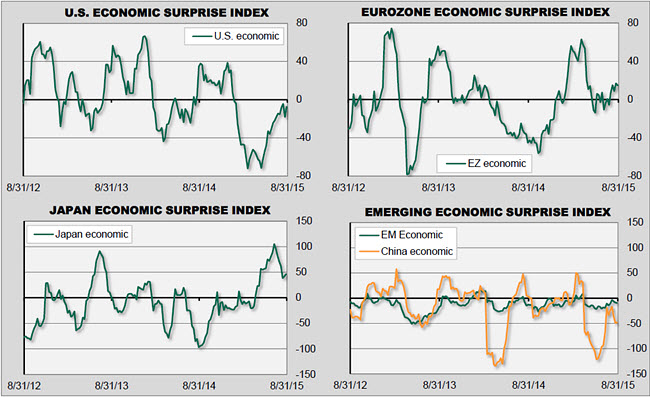

EXHIBIT 2: DEVELOPED GROWTH STURDIER THAN EMERGING

Sources: Northern Trust Investment Strategy, Citigroup, Bloomberg; data through 8/28/15.

U.S. economic data has been on a positive upswing since the poor first quarter growth figure, and growth averaged 2.2% for the first half of 2015. While this isn’t great growth, it is right in line with the average growth realized since the end of the global financial crisis. We expect durable growth to continue from the United States, as there are little excesses in the real economy and no inflationary pressure to push the Fed to raise interest rates faster than market expectations. European growth has also seen some improvement of late, while their second quarter growth was modestly disappointing. European growth averaged 1.1% in the first half of the year, and should continue to benefit from a cyclical upturn in spending. Europe was in recession for most of 2012 and 2013, so has considerable room to expand at a moderate pace.

Japanese growth has been highly volatile, regularly moving in and out of mild recession, over the last five years. Japan is disproportionately affected by slower Chinese and emerging market (EM) growth, relative to Europe and the United States. More recent data gives some signs of hope, including July consumption and labor data, along with a strong Purchasing Managers Index (PMI) release. While overall EM growth data hasn’t been that volatile, headline PMI releases are below 50 in China, Korea, Taiwan, Malaysia, Singapore, and Indonesia. Chinese data has recently shown some weakening after a solid improvement. Export data was particularly disappointing in July, and the recent PMI reports have also been soft. As always, transparency into China’s economic data remains low, and the stock market continues to be highly volatile. To that end, a stubbornly high 18% of Chinese stocks continue to have their trading halted. We have been forecasting disappointing Chinese, and emerging market, growth over the next year and continue to see that as the right conclusion. To cushion a hard landing, Chinese policy makers remain engaged through interest rate reductions and easing of bank capital requirements. We expect them to remain focused on generating short-term growth at the expense of long-term reform – a long-term setback but one that reduces short-term risks both socially and financially.

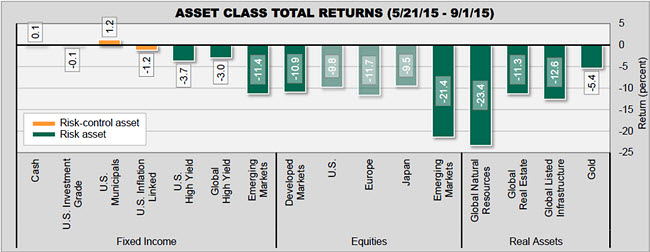

EXHIBIT 3: DISCRIMINATING AGAINST EMERGING & COMMODITIES

Sources: Northern Trust Investment Strategy, Bloomberg. Gross total returns in USD, 5/21/15 – 9/1/15.

Is there a message in asset class performance during the correction? Risk assets broadly have underperformed (see Exhibit 3), but the relative performance of corporate credit gives some comfort that this decline is more of an adjustment in risk appetite than a precursor to recession. While credit spreads have widened from last summer, we think this has been a result of both increased supply and some discounting of a slowing economy. Investment grade and high yield spreads have performed well of late, and are not signaling signs of new concerns about economic growth. The high coupon of high yield bonds has offset spread widening, leading to modestly positive returns in active high yield strategies. We also have seen orderly trading in the bond market, a constructive sign for risk taking. Sovereign spreads across Europe are also exhibiting relative calm, a sign of investor comfort. Finally, we think the relative stickiness of the U.S. 10-year yield (currently at 2.16%) is another sign that economic growth is not faltering, and that the Fed is still expected to raise rates by around 0.50% over the next year.

On the equities front, we think the decline in prices is more a reflection of a repricing of risk than a downgrade in fundamentals. Our discussions with company management teams over the last several days do not indicate cause for concern. Demand and new orders in developed economies remains stable to slightly better of late, while emerging markets remain mixed. Industrial demand in EM remains weak (not a new trend), while consumer demand remains positive (e.g. Apple’s commentary on phone activation data in China).

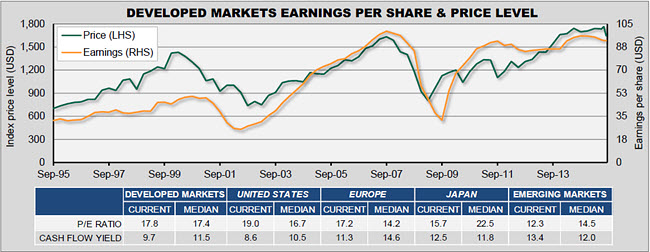

EXHIBIT 4: DEVELOPED STILL ELEVATED WHILE EM IS CHEAPER

Sources: Northern Trust Investment Strategy, MSCI, Bloomberg. Data through 9/1/15. Median = monthly data back to 1970 (1995 for emerging markets).

Has much value been created in the recent sell-off? The answer: some, but not a great deal. This evidence supports our Cyclical Meets Structural theme, whereby high valuations are challenged by slow structural growth – thereby moderating longer-term equity returns. Exhibit 4 shows current valuations for major regions relative to their historical medians. U.S. equities, at 19 times trailing earnings, are down from 20 times as of the end of April, but still above median of 17.4. Similarly, European equities have seen their p/e ratio fall from 19.3 to 17.2, compared to a 14.2 median level. Japanese stocks have seen a decrease in valuations from 17.9 to 15.7, well below their bubble-inflated historical levels. Finally, EM equities have fallen from 14.6 to 12.3 times earnings, below median levels of 14.5 times.

CONCLUSION

The markets are coming out of a period of extraordinarily low volatility, where central bank largesse backstopped risk taking. While we only expect small moves in policy rates over the next year, these changes are happening in a period of mediocre global growth. Our research on stock market declines indicates that the current decline could be an average correction in a non-recessionary period, and the major spike in volatility has historically been a precursor to positive returns. Long-term investors with a strategic asset allocation and an appropriate liquidity plan in place are in a position to ride out this volatility. Our approach to tactical asset allocation over the last decade has been based on a disciplined philosophy, with set meeting dates to reduce the risk of over-reacting to short-term market events. In fact, we have only called two formal intra-period meetings over this entire period. We did have a teleconference with members of this committee this week to discuss whether any action was warranted ahead of our September 11 Investment Policy Committee meeting. After a review of the fundamentals and market action we decided our current recommendations remained appropriate. Regular readers of our research know that we have reduced our recommended tactical asset allocation risk from a near-maximum overweight to risk last Fall to near-benchmark risk in July. Within these recommendations, we continue to favor U.S. dollar-denominated assets like U.S. equities and high yield, while underweighting emerging market equities and debt, developed ex-U.S. equities and natural resources. While we are positioned for slow but steady growth, a further deterioration in the global growth outlook is the most likely catalyst for us to further reduce risk, while greater confidence around an upturn in growth is the most likely reason we would recommend increasing risk exposure.

Special thanks to Tyler Bullen, Investment Analyst, for data research.

IMPORTANT INFORMATION: This material is for information purposes only. The views expressed are those of the author(s) as of the date noted and not necessarily of the Corporation and are subject to change based on market or other conditions without notice. The information should not be construed as investment advice or a recommendation to buy or sell any security or investment product. It does not take into account an investor’s particular objectives, risk tolerance, tax status, investment horizon, or other potential limitations. All material has been obtained from sources believed to be reliable, but the accuracy cannot be guaranteed.

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS. Periods greater than one year are annualized except where indicated. Returns of the indexes also do not typically reflect the deduction of investment management fees, trading costs or other expenses. It is not possible to invest directly in an index. Indexes are the property of their respective owners, all rights reserved.