With rocky equity markets and concerns about economic growth in China, there seems to be a growing chorus in the market calling for the Fed to hold off on raising rates in September. In fact, many are now saying (hoping?) that the Fed holds off raising rates until 2016. Bill Dudley, president of the New York Fed, came out today saying that the case to raise rates is “less compelling” than it was just a few weeks ago. Generally, the short-term reaction to any dovish talk out of the Fed is positive for the stock market but is this a psychological phenomenon or something that is backed up by actual market returns?

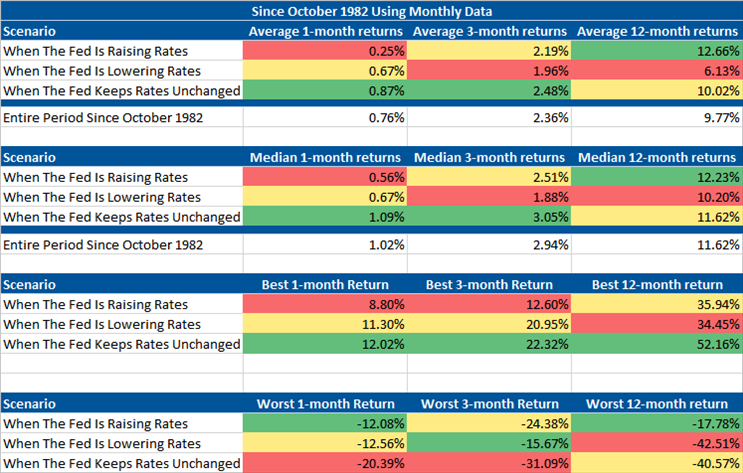

According to this Federal Reserve working paper, the Fed quietly began targeting the Fed Funds Rate in October 1982. So we are using October 1982 as our starting date for this analysis. In the tables below, we used monthly data on the S&P 500 provided by Robert Shiller. We looked at forward returns for three different circumstances: 1) when the Fed Funds Target Rate was higher than in the previous month (Fed is raising rates) 2) when the Fed Funds Target Rate was lower than in the previous month (Fed is lowering rates) 3) when the Fed Funds Target Rate was the same as in the previous month (Fed keeps rates unchanged).

The worst scenario for investors with a time horizon of at least a year is when the Fed is easing. This probably shouldn’t be surprising given that the Fed is usually easing when the economy is slowing, however, we think most investors would assume that the best stock market returns come when monetary policy is easing. Average 12-month returns are half of what they are when the Fed is raising rates and median 12-month returns are two percentage points lower as well. Also, three-month returns are worse when the Fed is easing. It does seem that easing does provide a short-term boost to market psychological since 1-month returns are slightly higher than when the Fed is raising rates.

The best scenario for 12-month returns is when the Fed is raising rates. The US stock market averages 12.66% in months when the Fed has raised the target rate for the Fed Funds Rate. Median returns are also at its highest at this point. And perhaps most importantly, the worst 12-month return during a period when monetary policy is tightening is -17.78%. While painful, it is not nearly as painful as the -42.51% drop experienced when the Fed is easing.

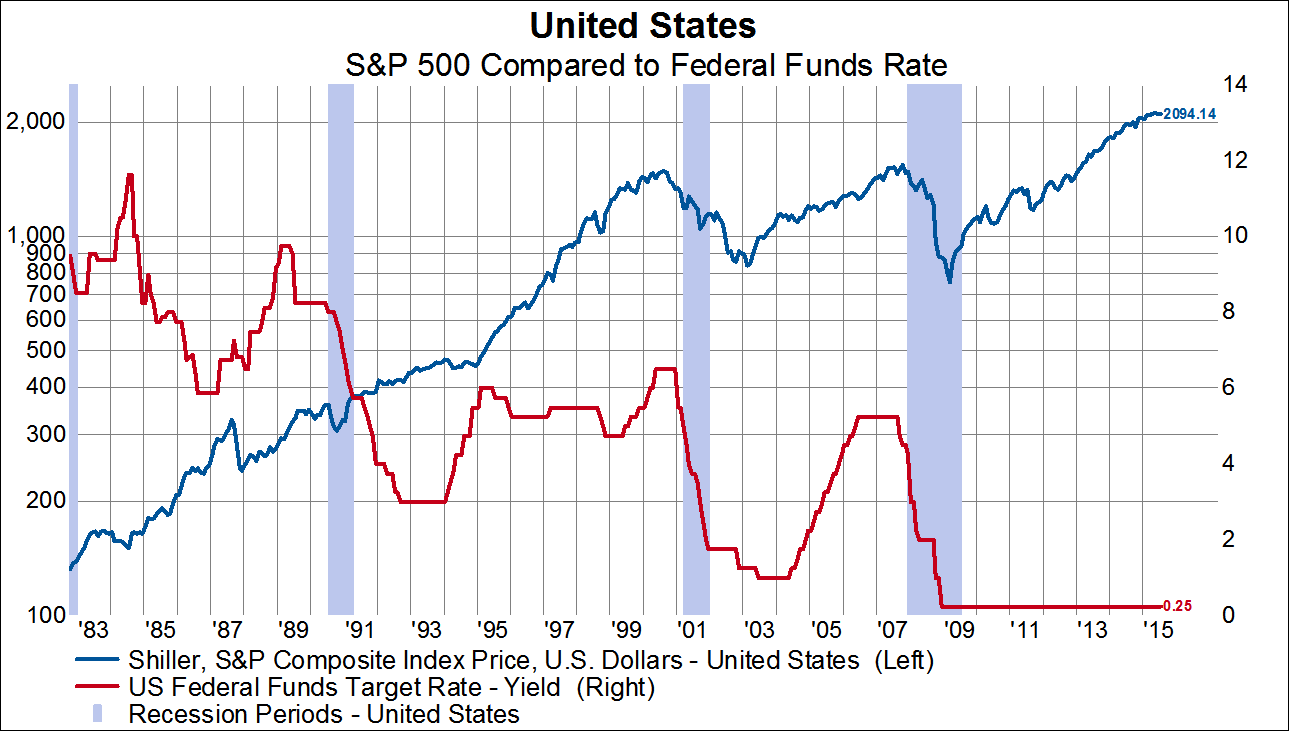

Stock market returns since 1982 have been strong no matter what monetary policy has been up to. This is the case even though we have experienced two major stock market drawdowns during this period. Overall, investors should be hoping that the Fed raises rates in September because if they do, more likely than not, equity markets will be significantly higher come September 2016.