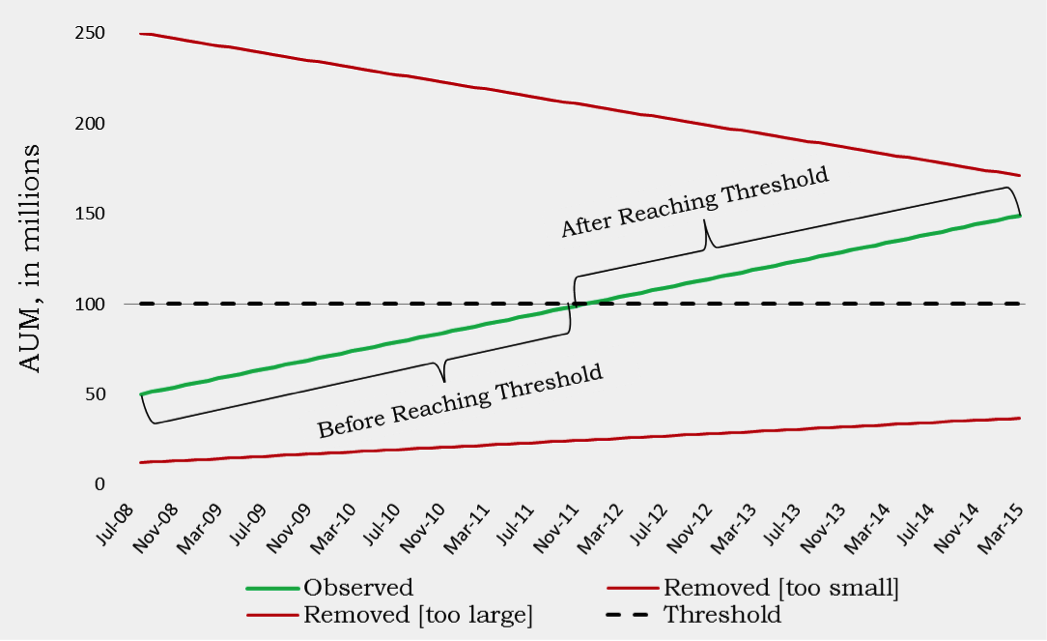

In part one, we looked at the statistics of how difficult it was for hedge fund managers to consistently outperform the universe average. In part two, we wanted to examine the consistency of a hedge fund’s1 performance as its assets grow. We took the HFRI Equity Hedge Fund universe and looked at individual managers’ assets and returns during a recent period. The dataset includes funds reporting at any point between August 2008 to March 2015. With a threshold benchmark of $100 million, we filtered out managers who did not meet the criteria of surpassing the $100 million mark at any point in their track record. We also removed funds that didn’t have at least six months with sub-$100mm returns and post-$100mm returns to remove any insignificant data. Once filtered, we compared the returns vs. the HFRI Equity Hedge Index2 during both relative time periods of pre-$100mm AUM and post-$100mm AUM.

For example3:

1 An investment fund is a way of investing money alongside other investors in order to benefit from the inherent advantages of working as part of a group.

2 The HFRI Index is a fund-weighted (equal-weighted) index designed to measure the total returns (net of fees) of the approximately 2,000 hedge funds that comprise the Index. Constituent funds must have either $50 million under management or a track record of greater than 12 months. The HFRI Index consists only of hedge funds. The HFRI Fund universe is one of the HFRI sub strategies.

3 The source for all data used is Commerce Asset Management. All data was used for a hypothetical example.