The most important overarching story of the week was the emerging market capital flight, which is occurring at startling pace:

Total net capital outflows from the 19 largest EM economies reached $940.2bn in the 13 months to the end of July, almost double the net $480bn that flowed out during three quarters of the 2008-09 financial crisis, according to a compilation of official data and estimates by NN Investment Partners, an investment bank.

The exodus continued through the week. There are several factors driving this move, starting with the decline in Chinese demand for raw materials. The most recent manufacturing PMI was 47.1, the lowest reading in 77-months. Sub-indexes for new orders, new export orders, output and employment are decreasing at a faster rate. Countries that sell those materials are experiencing export declines and capital flight. Compounding potential problems are some companies borrowed in dollars to expand operations. As their respective home currencies decline, these companies may experience interest rate payment shocks. Adding to the problem is the long anticipated Fed interest rate hike, which placed a very strong bid under the dollar towards the end of last year, increasing the dollar index ~15-18%. Traders sold EM currencies to buy dollars, leading to the current EM currency decline. Several stories highlight the issues involved:

- The rubles drop has increased import prices and domestic inflation, leading to internal problems.

- The real’s drop has complicated an already difficult macro and political situation in Brazil.

- EM sell-offs have put pressure on the respective central banks.

- Currencies that may follow the yuan lower.

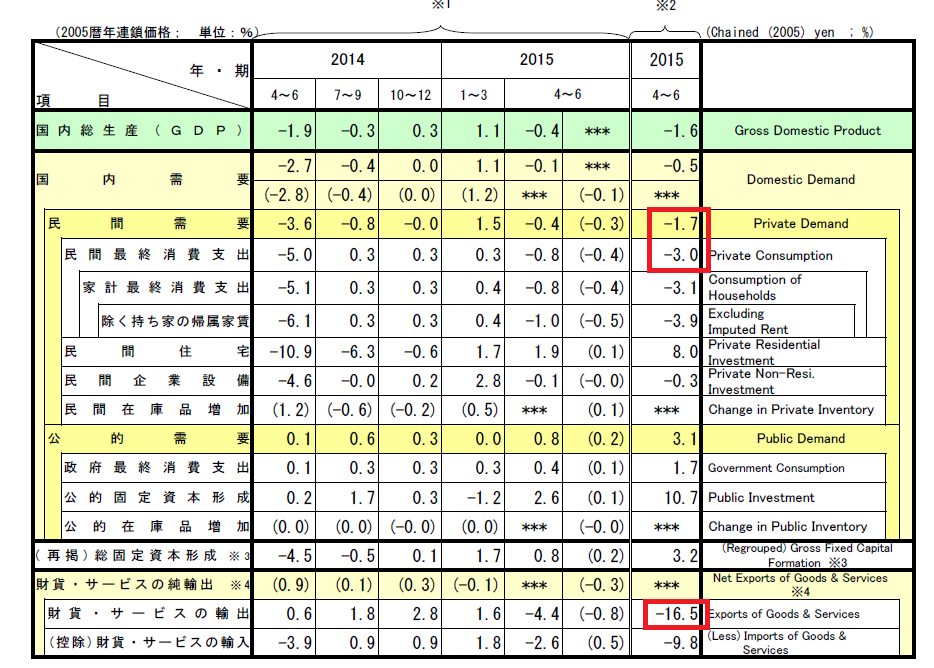

Japanese 2Q15 GDP was a big disappointment. On an annual basis, the top line contracted 1.6%. But private consumption was down 3% annually. Although consumer’s inflation expectations are rising, this increase isn’t translating into an acceleration of purchases. Exports contracted 16.5%, throwing cold water on the BOJ’s yen devaluation strategy. The only good point was an 8% annual increase in residential construction:

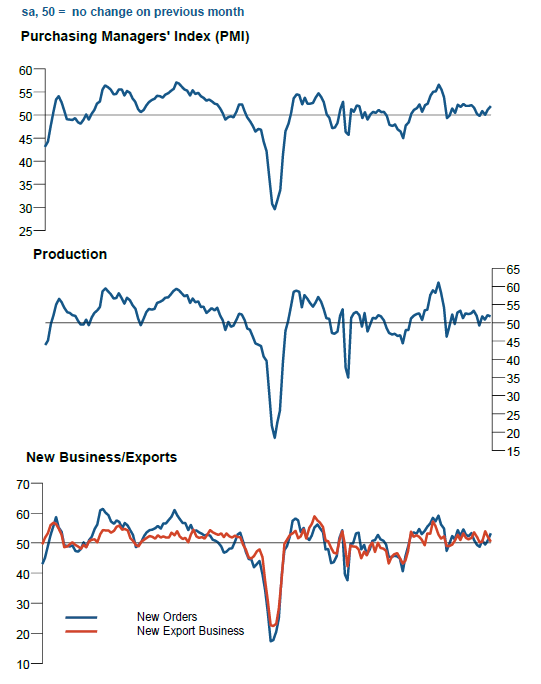

Exports were up 7.8% Y.Y. But while this data set is in a slight uptrend, current levels are still below pre-recession levels. Finally, Japanese manufacturing PMI registered a 51.9, with production, new orders and employment increasing. As these graphs from the report show, Japanese manufacturing is growing:

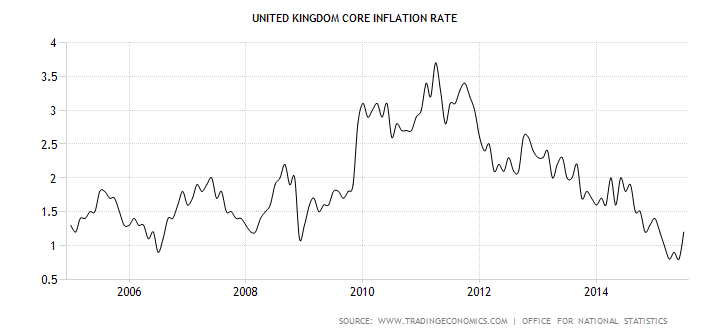

UK inflation was low (again) with total CPI up a paltry .1% M/M. Some analysts pointed to the 1.2% Y/Y rise in core inflation as a justification for a faster pace of rate increases. And, the Sterling jumped in response to this news. But when this increase in placed into context, it’s difficult to argue the rise is somehow meaningful from a policy perspective; the overall core rate is still very low and in a clear downtrend:

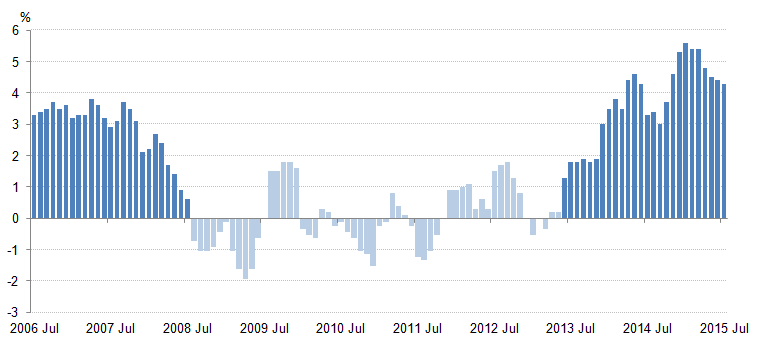

UK retail sales were up 4.2% Y/Y. As this graph from the report shows, the three months rolling average of comparisons continues to be strong:

A broad range of UK retail prices continue to decrease. From the report: “Average store prices (including petrol stations) fell by 3.0% in July 2015 compared with July 2014; the 13th consecutive month of year-on-year price falls. All store types except textile, clothing and footwear stores reported decreases. Petrol stations again made the largest contribution, falling by 10.9%, the 23rd consecutive month of year-on-year falling petrol prices.”

The RBA released the minutes from their latest meeting, which contained the following observation about the domestic economy:

The Board's discussion of the domestic economy commenced with the observation that GDP growth over the next couple of years was expected to be slightly lower than forecast in May, although the revision was minor relative to the usual range of uncertainty. A downward revision to population growth had contributed to lower forecast growth in consumption and non-mining business investment. The forecasts for growth in public demand and business investment had been revised lower in light of new data. In contrast, the recent exchange rate depreciation had led to an upward revision to net exports. Aggregate growth was expected to remain moderate for a time before strengthening. Members recognised that the period of significant structural change for the Australian economy associated with the winding down of the mining investment boom would continue for some time.

There were no new revelations regarding the Australian economy in the minutes. It continues to grow at a below trend pace, largely as a result of the drop in Chinese economic growth. In other news, auto sales were up 3.7% from a year earlier. But as this graph of the data shows, new cars sales, while growing, are doing to at a very slow rate.

The main news from the EU was the Markit flash survey. The EUs composite number was 54.1, with manufacturing at 52.4 and services at 54.3. New business, employment and backlogs all increased. Germany saw solid numbers with the services, manufacturing and composite numbers printing at 54.6, 53.4 and 54, respectively. Like the macro numbers, new orders, production and employment all increased. While France’s service sector continued to expand (PMI of 51.8), manufacturing contracted again (PMI of 49.3).

Overall the EU region continues experiencing the strongest numbers and overall performance in the last four years.

Canada – which needed good news – got some. Prices were up 1.3% Y/Y. With the exception of transportation, all sub-indexes increased. And core prices remain near the 2% level:

Retail sales increased 1.4% Y/Y, which continued this data series recent increases after a sharp drop at the end of last year.

US news will be more fully covered in the US Equity and Economic Review on Sunday. News was mixed, but with an important caveat. Building permits dropped sharply and the LEIs were down .2%. But both were negatively impacted by the expiration of a NY tax credit encouraging the building of apartment buildings. This pulled sales forward the last few months, leading to a sharp decline on its expiration. However, the smoothing impact would be far more moderate. Housing started were virtually unchanged while existing home sales were up 2%. The total impact of housing news was of a sector that was still growing. Finally, prices remain contained, increased .2% Y/Y.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis