Our firm often cites a paradox in the hedge fund industry: hedge fund of funds lag the mean hedge fund return. Represented below, the HFRI Fund Weighted Composite Index is composed of individual hedge funds of all types that are equally weighted while the HFRI Fund of Funds Composite Index is a separate index composed of equally weighted funds of hedge funds.

Source: eVestment

Source: eVestment

We would be able to casually dismiss this paradox to fee differential, however, the excess performance of individual funds over funds of funds is above 3% annualized since inception, far above the added fee layer for fund of funds managers. If fund of funds managers can hand-pick top quartile all-stars why do they perennially provide subpar returns…hence the paradox.

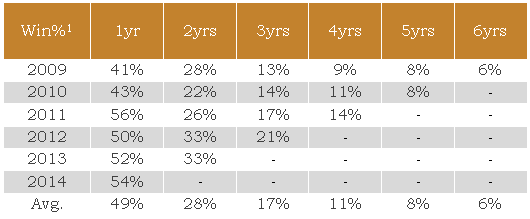

In the above example, fund selection actually detracts from the outcome. How can this be? There are multiple hypotheses that can be made about why fund selection is challenging. We wanted to focus on performance-based fund selection. We conducted a strict performance based study. Very simply, can an individual fund outperform the mean two years in a row?…how about three years in a row? We analyzed equity hedge funds that outperformed their index in a given year and tracked how they performed in subsequent years. The results are, what we believe, representative of the challenges of performance-based manager selection.

Source: eVestment

On average, if you were selecting from the previous year’s winners, you would be back to a coin-flip as to whether they were going to outperform after your investment. If your turnover is low, you will most likely succumb to subpar returns. On average about 49% of the managers will beat the index in a given year (due to the effects of skew on the mean vs. median). About 28% of the managers were able to produce above average returns 2 years in a row and only 17% for three years in a row.

There are many reasons that individual hedge fund managers cannot consistently beat the average return of the universe of their peers. Many of the reasons lie in the fact that each universe is very diverse with multiple underlying styles and disciplines (growth bias vs. value bias, large cap bias vs. small cap bias, U.S. vs. Non-U.S., trader vs. long term investor, sector bias vs. generalist, etc.) and these styles and disciplines come in and out of favor as market dynamics and prices change. In addition, net exposure levels matter greatly. In falling markets, lower net exposure managers (as in 2008) outperform while in rising markets (as in 2009) higher net exposure managers outperform. As the performance data shows, hedge funds of funds face the daunting task of not only selecting the best managers they can find, but also trying to predict which styles or disciplines will at least not be out of favor going forward. The last reason for the difficulty in consistently outperforming the average is the asset growth of a hedge fund. We will save this topic for our next paper. Stay tuned…