The recent slide in oil prices is symptomatic of large fundamental shifts taking place across the energy sector. The current volatility is nothing new to oil markets as their self-correcting nature has frequently resulted in a sequence of deep boom and bust cycles. While we can anticipate and prepare for these cycles, much like with earthquakes, the timing and consequences can still be surprising. In times like these, maintaining a long-term perspective is essential to place current events in the proper context. Occasionally, by making rough sense of the past we can gain credible clues on the path forward. However, most of the time, we simply cannot forecast with any reliable degree of accuracy the price of oil. To compensate for these uncertainties, we rely heavily on the concept of margin of safety. We can apply a margin of safety not only in the price we pay, but also in the strategic positioning of the businesses we own. In this piece, we examine the fundamental shifts taking place in the energy sector and the companies we believe are best positioned to adapt to these new realities.

Structural Change

For oil markets, the single largest event of 2014 may have been the recognition that the shale resource base in the United States was rapidly expanding at the same time that breakeven economics were falling. As discussed in our March 2014 Industry Perspective, Exploration & Production: An Evolving Business Model, some of our holdings, like EOG Resources, Inc. (EOG) and Cimarex Energy Co. (XEC), were at the leading edge of this development. They were very well-positioned to continue to take market share as their production profile was becoming more predictable and flexible, and less capital intensive. The major risks to future production growth were quickly being whittled down to commodity price risk stemming from either a reduction in expected global oil demand growth or a major shift in OPEC policy.

To the shock of the energy sector, both of these events occurred toward the end of 2014 as surprising drops in demand growth and competition from growing non-OPEC supply created a difficult proposition at the November OPEC meeting. Saudi Arabia, the de-facto leader within OPEC, has often played the role of “swing producer” in order to help stabilize global inventory levels. However, after reducing production by around two million barrels per day in 2009 – the last period of major oversupply – Saudi Arabia decided to maintain production this time. The message to the rest of the oil industry has been clear: Saudi Arabia is securing market share while leaving the burden of adjustment on others.

It is instructive to analyze Saudi Arabia’s dilemma to gain insights into the structural changes taking place within oil markets. Upon Saudi Arabia’s realization that a large loss in revenue was nearly inevitable, the key choice came down to either taking a large loss in revenue in the form of lower volumes and managing price, or taking no action and accepting lower prices. However, the progressively faster response time from domestic shale producers was undermining their ability to manage the market by reducing volumes. Any subsequent price rise from a production cut would quickly incentivize additional shale production and ultimately result in further market share loss. Saudi Arabia has painful memories of losing market share when other countries did not match their production cuts in the early 1980s. Then, as now, Saudi Arabia was facing competition from growing non-OPEC supply and lackluster growth in global oil demand. In an attempt to manage oil prices, Saudi Arabia allowed spare capacity to build up to approximately 20% of global demand before ultimately reversing their decision in late 1985. Given this analysis of the market, and a strong recollection of history, we believe maintaining production volumes and allowing the price to fall was a rational choice from a purely economic perspective.

An important implication from Saudi Arabia’s new position is that spare capacity is currently low and will likely remain at historically low levels going forward. This key difference greatly reduces the probability of a repeat 15-year bear market for oil prices. Assuming trend demand growth, adding production capacity through investment would be substantially more expensive than simply increasing utilization rates. However, this does not suggest prices will quickly return to levels observed over the past decade.

Marginal Cost

Marginal cost is a simple, yet fluid, concept that guides commodity prices. The objective is to establish the approximate cost of the highest cost producer needed to match demand. As a result, valuing commodities is fundamentally different than valuing equities and bonds as there are no cash flows to value – only an expected clearing price. To gain insight into the future price of oil, we need to determine the future marginal cost of production. This, however, is a moving target as future conditions change depending on the actions of participants today.

Saudi Arabia’s decision to protect market share, along with expansion of the shale resource base, set into motion a frantic re-shuffling of industry capital investment plans and the market’s search for the future marginal cost of production. Some estimates suggest that more than $500 billion in capital investment plans could ultimately be displaced. The painful process of adjustment has created a negative feedback loop and is having dramatic implications on cost structures throughout the energy sector. To guide our estimates for the future marginal cost of production, we are actively monitoring deflation across the oil service supply chain, potential reversals of punitive fiscal terms, OPEC investment levels, and prospects for further efficiency gains as projects struggle to be economically competitive.

Sticking With Quality

A decade ago, our confidence in a rising marginal cost of production was driven by significant underinvestment in productive capacity while emerging markets had an economic tailwind driven by strong balance sheets. As both of these trends slowly began reversing, our assessment of downside risk to the future marginal cost of production began to grow. From a portfolio management perspective, we gradually reduced our exposure to the energy sector across many of our strategies. At the same time, we maintained, and even increased, our core investments in Cimarex Energy and EOG Resources because we believe their qualitative positioning would best allow them to adapt and create value through a possible industry downturn.

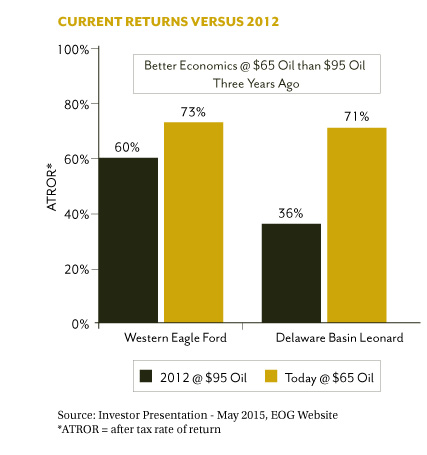

Charles Darwin famously observed that it is not the strongest or the most intelligent who will survive, but those who can best manage change. Likewise, in a highly competitive business where the price of output can double or halve in relatively short order, the ability to manage change is a crucial variable to understand. While commodity price is a significant variable, what is most important to us is a company’s ability to operate profitably under a variety of commodity prices and to allocate capital wisely. We have high confidence that both Cimarex Energy and EOG Resources can execute on both fronts. Their attractive asset positions, dynamic cost structures, and strong balance sheets are key advantages that provide the operational and financial flexibility to quickly adapt to changing environments. As an example, the chart below highlights the staggering progress that EOG Resources has made across two of their large assets, Western Eagle Ford and Delaware Basin Leonard. Over the next five years, we see multiple avenues for further improvement in breakeven economics for both Cimarex Energy and EOG Resources. If true, we believe that their growth potential has only been delayed and will resume as their relative cost advantages grow.

The views expressed are those of the research analyst as of July 2015, are subject to change, and may differ from the views of other research analysts, portfolio managers or the firm as a whole. These opinions are not intended to be a forecast of future events, a guarantee of future results, or investment advice. DIAMOND HILL® is a registered trademark of Diamond Hill Investment Group, Inc.

© 2015 Diamond Hill Capital Management, Inc. All Rights Reserved.

© Diamond Hill Capital Management