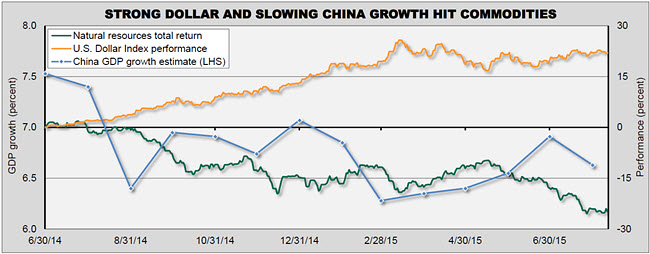

Commodity prices have been under significant pressure over the last year, due to a multitude of factors. Emerging market growth has been disappointing. Decelerating growth in China (see the blue line in Exhibit 1) has led to a shortfall in demand. OPEC has kept their pumps running full speed despite the demand shortfall, in an apparent attempt to slow U.S. fracking, leading to a plunge in oil prices; the strengthening dollar (orange line in Exhibit 1) has also hurt commodity prices. The resulting poor return of commodity-related investments has caused some investors to question both the short-term and long-term merits of natural resources investments. We do have a tactical underweight recommendation (12-month time horizon) for commodities, due to the soft demand outlook and the negative impact of the strong dollar. However, our strategic recommendation (5-year outlook) supports an allocation to commodities as we expect some tightening of supply to improve prices over the longer term. The recent selloff in the commodities complex has improved the current valuations of commodities-related stocks. In addition, we think commodities provide an effective hedge against the risk of inflation. Finally, our strategic recommendation is based on an equities-based approach to investing in commodities, as opposed to a futures-based approach. We believe that investing in the equity of commodity producers (such as energy, mining, chemical, agriculture and water companies) will produce a superior return over a futures-based approach, while still providing good inflation protection.

EXHIBIT 1: DOUBLE WHAMMY OF HIGHER DOLLAR AND SLOWER CHINA

Sources: Northern Trust Investment Strategy, Bloomberg. Data through 8/10/15 (China growth estimate through 7/31/15). Natural resources = Morningstar Global Upstream Natural Resources Index. China growth = Bloomberg estimates.

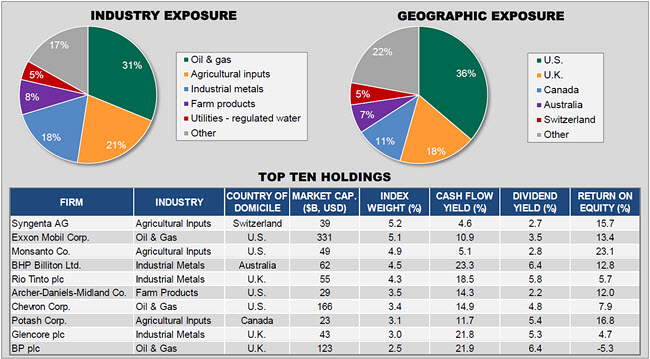

The commodity complex is a heterogeneous one, with respect to both the varied types of commodities and the indexes that measure aggregate performance. Because we believe that inflation protection is one of the primary attributes of commodity investing, we favor a benchmark that highly correlates with inflation trends – the Morningstar® Global Upstream Natural Resources Index. To lend some insight into this occasionally misunderstood asset class, we show some of the key attributes of this index in Exhibit 2. Firstly, it is well diversified amongst industries. Oil and gas (energy) comprises 31% of the index, as compared to over 70% for the S&P GSCI® Commodity Index. Agriculture and farm products comprise another 29%, and movement in the price of these commodities is driven by different factors than the other commodities. The final large component is industrial metals and minerals, which contribute 18% to the index. The geographic exposure appears well diversified, but this is somewhat misleading as it represents the home listing country of the stocks in the index. There is clearly much greater exposure to emerging market growth in the end-demand of these companies than is reflected in their home countries.

EXHIBIT 2: DIVERSIFIED NATURAL RESOURCES EXPOSURE

Sources: Northern Trust Investment Strategy, Bloomberg, Morningstar. Data as of 7/31/15. Index shown is Morningstar Global Upstream Natural Resources Index.

The top 10 companies represent 39.4% of the index, with another 110 companies making up the remainder. We show the largest companies in the index to highlight that this investing approach to commodities involves owning operating companies, as opposed to investing in futures contracts on commodities. We believe an advantage of this approach is that investors are exposed to the economic returns that the operating companies generate, and still retain sensitivity to inflationary trends. This is in contrast to the futures-based approach, where your prime assets are derivatives contracts and the collateral that supports them (usually being invested at de minimis interest rates).

The best run of these companies will focus on maximizing shareholder value and maintaining dividend payouts, even during a downturn in commodity prices. The major oil and gas companies have a strong record of dividend payouts, during oil bear markets. The bear market in oil prices in the mid-1980s was comparable to the current environment, and neither Exxon nor Chevron cut their dividends back then. Should Brent crude prices stick near the current level of $49/barrel, the focus on dividend sustainability will rise. However, in the current environment, we would expect capital expenditure cuts to occur before dividend cuts, and we think crude prices could fall toward $25/barrel before we’ll see dividend cuts at the top-tier producers. The agricultural input companies should also have a relatively stable dividend outlook. Their balance sheets tend to be stable and pricing is better than in the industrial metals space. Industrial metals company dividends have the most uncertainty, and further price weakness would materially raise the risk of dividend cuts.

Exhibit 3 highlights the longer-term realized return differential between the two approaches to commodity investing. While the excess return year-to-date has been minor, the annualized differ-ential over all other periods has been considerable. On a 3-year and10-year horizon, the equity-based approach has outperformed the futures-based approach by roughly 10 percentage points per year.

EXHIBIT 3: THE EQUITY-BASED RETURN ADVANTAGE

Sources: Northern Trust Investment Strategy, Bloomberg. Year-to-date (YTD) returns through 8/10/2015; 1/3/5/10-year returns through 7/31/2015. Periods longer than one year are annualized.

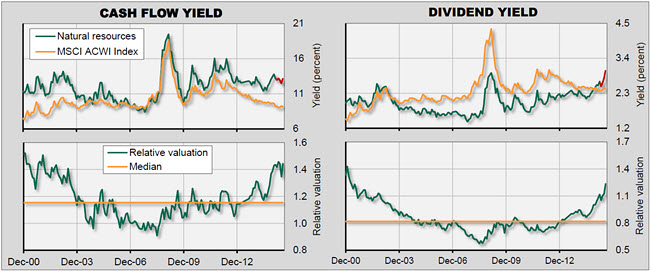

Our strategic positioning in commodities (or referred to as natural resources when using an equity-based approach) is a reflection of our belief that the next five years will differ from the past year. As readers of our annual capital market assumptions whitepaper (Five-Year Outlook: 2015 Edition) know, valuations play a big role in our longer-term expectations for asset class returns given their predictive power over a five-year time frame. Exhibit 4 shows the current discounts in the natural resource sector vs. the broader equity markets given the recent sell-off.

EXHIBIT 4: SELL OFF HAS CREATED SOME VALUATION SUPPORT

Sources: Morningstar, MSCI, Northern Trust Investment Strategy. Data through 7/31/15. Northern Trust estimates in red for natural resources valuations begin after 3/31/15.

We estimate the current cash flow yield for natural resources to be 13.2%, above the median level of 12.0% since late 2000. Relative to global equities, natural resources stocks have a cash flow yield of 144% of the market yield, compared with a median level of 115%. The dividend valuation is similar, with a current yield of 3.0% and a relative yield of 124% compared with a median of 82% over the last 15 years.

Since these valuation measures are based on trailing values of cash flow and dividends, they are subject to pressure should earnings continue to fall. Currently, consensus estimates for both energy and materials are for an earnings rebound in 2016 of 29% and 14%, respectively. While there is clearly risk to the 2016 estimates, we do think that current valuations provide some cushion for longer-term returns, so long as the fundamentals within the space do not deteriorate further during that time frame. Per our “Slow Burn of Low Growth” theme, we do not expect – nor does our forecast require – a surge in demand for natural resources over the next five years.

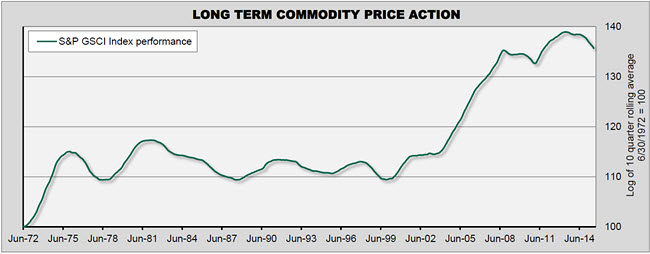

If we felt that a demand surge would occur, we would have increased our five-year total return forecast; we instead kept it steady at 7.0% (though it did make the asset class more attractive in asset allocation modeling as most other risk asset forecasts fell). Rather, we believe a demand profile consistent with our low growth (but not recessionary) five-year outlook – combined with longer-term supply issues – will be sufficient to induce a modest cyclical upswing in commodity prices over the next five years. This expectation is consistent with the cyclicality witnessed in commodity prices going back to the early 1970s, which was only interrupted by the emerging market-driven commodity super cycle during the late-2000s (Exhibit 5).

EXHIBIT 5: NOT CALLED CYCLICALS FOR NOTHING

Sources: Northern Trust Investment Strategy, Bloomberg. Data through 7/31/2015. Price movement measured using the natural log of average trailing 10 quarter price levels.

The difference between our cautious tactical outlook and our more constructive strategic outlook for underlying commodity prices comes down to the economics of commodity extraction. In the near term, fixed costs are sunk costs and producers will continue to produce so long as they are cash flow positive (revenues exceed the direct costs required to produce those revenues). Longer term, new projects will not be taken on unless they also cover the fixed costs. This will require higher commodity prices to overcome the higher cost hurdle. It is important to remember that most commodities are consumed. Thus a slow growth (or even no growth) environment does not remove the need to discover new resources for commodities that have finite supplies readily accessible.

Beyond the long-term, valuation-driven opportunity, we believe a strategic allocation to natural resources is supported by the risk management attributes it brings to the investment portfolio. Many economic disruptions are caused by events that actually benefit the natural resources asset class. Weather aberrations may push food prices up, hurting consumer spending and overall economic demand but benefitting those companies with agriculture exposure. Social unrest may lead to emerging market energy production disruptions, impairing economic functioning but benefitting oil producers.

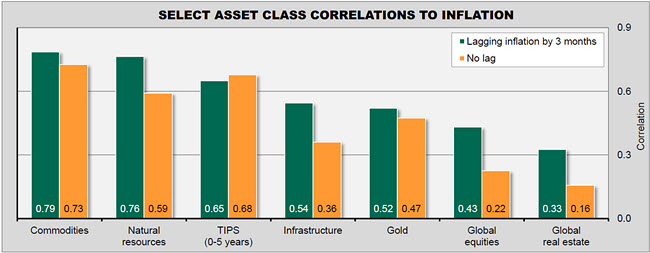

Overall, futures-based commodities and equity-based natural resources remain the best protection against inflation as seen in Exhibit 6, which shows the correlations over the past 10 years of year-over-year asset class returns to year-over-year inflation – both on a coincident and three month-lagged basis (to account for the market discount mechanism). Our other primary real assets, global listed infrastructure and global real estate, provide cash flows that can adjust for inflation, but at the total return level, do not exhibit the same levels of correlation to inflation that commodity strategies do. While neither we, nor the markets, anticipate major inflationary pressures in the near term or longer term, we believe a well-structured strategic portfolio should provide protection against unexpected events and would remind strategically oriented investors that the best (i.e. cheapest) time to take out an insurance policy is when you don’t think you need it.

EXHIBIT 6: COMMODITIES EXCEL AT INFLATION PROTECTION

Sources: Northern Trust Investment Strategy, Bloomberg. Data 6/30/2005 through 6/30/2015. Inflation = U.S. CPI year-on-year change.

Going beyond our top-down outlook for natural resources, the three major natural resource sectors (energy, industrial metals and agriculture) have specific long-term considerations. The energy sector is currently oversupplied due to some slowdown in demand and the increased supplies from fracking in the United States. However, excess supplies from fracking activities are not expected to persist longer term given expected depletion rates that are much higher than conventional oil fields (upwards of 25% per year in some cases vs. the broader 4% level). Even when assuming just a 4% depletion rate, a 1% demand growth expectation (a conservative estimate, in part due to potential substitution to other forms of energy) means 36% of current oil production will need to be replaced by 2020. This will require new investment – and higher prices to justify that investment. Industrial metal production benefitted from a massive infrastructure buildout as company management teams simply extrapolated high Chinese demand growth into the future. Chinese demand has, of course, slowed leaving an oversupplied situation. However, as companies reduce investment in the wake of slower Chinese demand, the industry is setting itself up for a cyclical rebound; many industrial metals are already priced below estimated marginal costs, let alone higher total costs should new investment be needed down the road. Industrial metals are not “consumed” the same way energy and agricultural commodities are (a bridge lasts for decades, a meal lasts for a few hours); therefore, new demand will need to play a bigger role. Some potential areas of incremental demand include global infrastructure needs and China’s “One Belt, One Road” initiative, but the slowdown in the industrial metal needs of broader China needs to be remembered.

Agriculture demand over the next five years is more certain than either energy or industrial metals demand, given the fact that agriculture is consumed and there are few substitutes (the transition in emerging market diets from grains to protein only increases the demand for agriculture products given the grain-intensity of raising livestock). Agriculture supply will be driven by weather aberrations (which cannot be predicted, but it can be reasonably assumed that they will continue) and genetically modified organism adoption (wherein some factions are throwing up roadblocks but it may be the only way to feed a growing population).

CONCLUSION

The short-term picture for commodity investing remains challenging. Our expectations for disappointing emerging market growth and strengthening in the U.S. dollar both point to the potential for further commodity price weakness, leading to our tactical underweight to the asset class. We view the recent decision by China to devalue the Renminbi as further justification for our tactical positioning. However, with the sell-off in commodities comes a better valuation picture and an improved long-term return potential. We think commodities improve the risk/reward characteristics of a diversified portfolio by providing the best inflation protection of the major asset classes. In addition, we think the fundamental case for the supply/demand picture for the major commodities should improve over the five-year strategic timeframe, supporting their performance. Finally, we strongly favor an equity-based investment approach to commodity investing, as it has generated superior returns to a futures-based approach.

Special thanks to Edward Trafford and Jackson Hockley, Senior Equity Research Analysts, for their insights into the commodity complex; and also to Tyler Bullen, Investment Analyst, for data research.