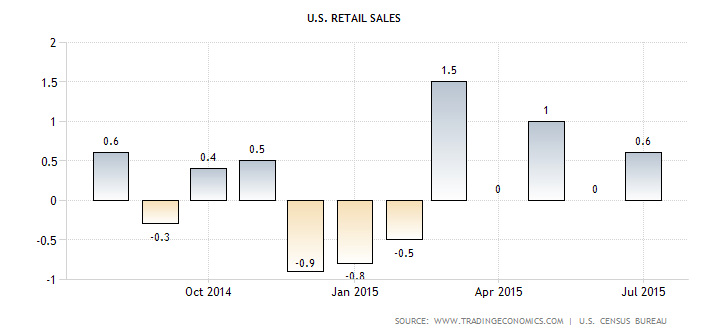

Retail sales increased .6% M/M. But this statistic has shown some weakness over the last year:

The best news in the report was the 6.9% Y/Y increase in auto sales. But over the last 12 readings, 6 have either been negative or 0%. And some of the increases have been small, totaling .4% and .5%. While the .6% was OK, this data series continues to point to a US consumer who is a bit more concerned about the overall economic situation, to the point where he is slowing his purchases.

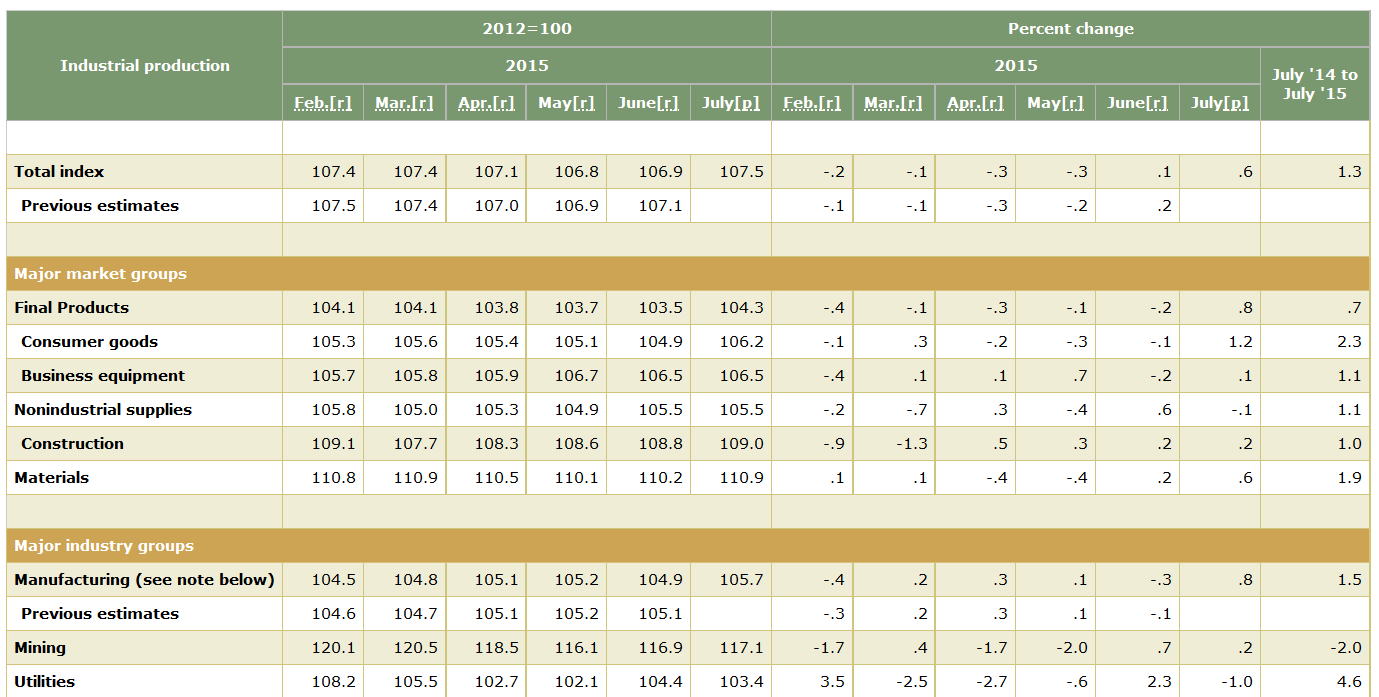

Industrial production had its strongest reading since February, rising .6%:

The accompanying notes indicate a sharp increase in auto and auto parts production was a primary reason for the overall increase. But it wasn’t the only reason. The report also noted, “[a]mong the nondurable goods industries, the indexes for apparel and leather, for paper, and for plastics and rubber products each advanced 1.0 percent.” To a certain extent, this report can be viewed as a “catch-up” report, where one month’s orders make up for weaker previously occurring production. But overall, this was the most encouraging industrial production report since February.

However, the Atlanta Fed’s GDP Now forecast has actually moved lower, now predicting Q/Q growth of between .6% and .7%:

Conclusion: the US economy is still in slow growth mode. Although US consumers are spending, they are doing so at a slower rate than previous expansions. This month’s industrial production number can easily be read a “one-off” number. And the GDP Now’s prediction is anything but encouraging.

Market Overview

The market is expensive. The current and future PEs of the SPYs and QQQs are 21.70/17.65 and 22.62/19.85, respectively. The markets need revenue and earnings increases to continue making gains.

As to earnings, we’re getting mixed signals from some analysts. First comes Zacks, who are downbeat:

We know that the picture emerging from the Q2 earnings season is one of overall weakness – growth is non-existent, with revenue gains particularly hard to come by and companies struggling to meet even the lowered top-line estimates. The outlook is no better for the current period either, with Q3 estimates following the by-now familiar downtrend that we have been seeing for the last many quarters.

However, they also note that several sectors such as medical, finance and retail are posting solid increases. And had it not been for oil, total earnings would have been near all-time highs.

Let’s calculate the y/y percent change in the 10 S&P 500 sectors during Q2 based on the blend of the available actual and analysts’ estimated earnings. Here is what we find:

Consumer Discretionary (12.0% vs. 7.1% at the start of the Q2 earnings season on July 1st), Consumer Staples (0.2 vs. -2.9), Energy (-56.2 vs. -62.8), Financials (20.7 vs. 14.8), Health Care (11.5 vs. 4.1), Industrials (-1.3 vs. -1.1), Information Technology (5.5 vs. 2.1), Materials (8.5 vs. 4.9), Telecommunication Services (9.3 vs. 5.5), and Utilities (4.5 vs. 0.5).

Three of the sectors are up with double-digit gains. All but Industrials are turning out to be better than was expected at the start of the earnings season.S&P 500 earnings was expected to be down 3.0% y/y during Q2 at the start of the season. The latest numbers show a gain of 1.6%. Excluding Energy, it is up 10.2%. That’s impressive and follows a similar pattern as during Q1, when S&P 500 earnings rose 1.5%, but 11.5% excluding Energy.

While these two points of view may seem to be polar opposites, they’re really not. Top line revenue growth is still slow; companies are still manipulating their expenses to arrive at higher earnings numbers. While this is an obvious short-term positive, we’re still left with the need to increase revenues to ultimately increase earnings. And finally, oil and the strong dollar continue to weigh on indexes that involve larger companies.

In looking at the markets, let’s start with the IWMs and IWCs:

Both are below their respective 200 day EMAs and have been in a downward trend since mid-July. Shorter EMAs are all moving lower. And with prices below the EMAs, this trend will continue. Overall, these averages – which are a good proxy for risk capital – are bearish.

And now the DIAs are following them down:

Dow prices have now moved below the 200 day EMA, and have the same technical characteristics as the IWMs and IWCs. But in blunter terms, this index is becoming bearishly aligned.

Only the SPYs remain in neutral territory, and there only because they continue to trade in a narrow, 10 point range.

Conclusion: part of the market’s overall weakness can be attributed to the summer doldrums. But traders are clearly concerned enough about the market’s overall situation to sell speculative issues (the IWMs and IWCs) below the 200 day EMA. And now the DIAs have followed, leaving only the SPYs and QQQs in positive territory. While the deterioration is disciplined, it’s still a bit concerning.