Business Insider and Barry Ritholtz both had posts in the last few days contributing to the same big idea that time is a valuable asset not just in and of itself but also as part of a financial plan and an investment strategy.

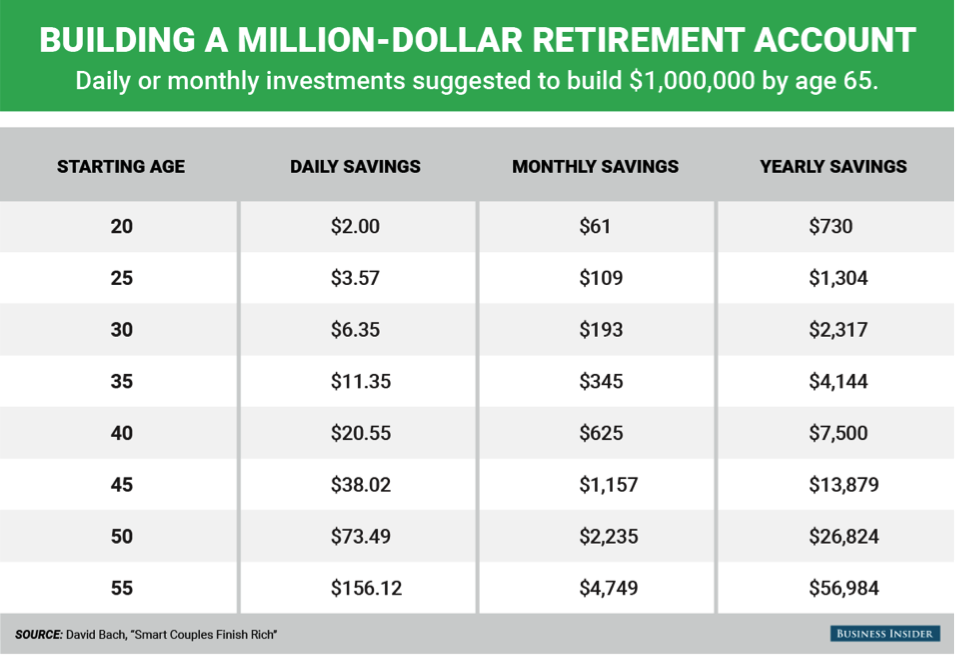

The graphic is obviously from Business Insider. The positive message here is that there is hope for people who take a while to start saving for their retirement. One issue with the table is that unfortunately it assumes 12% annualized returns. A 50 year old putting away $26,000 and annualizing at 6% (even that may require some luck) would have a little over $413,000 at 65.

The income safely generated from that amount plus Social Security would not equate to a lavish lifestyle but would be enough for the basics and at least a little fun, all the more so with some sort of part time income like from a successfully monetized hobby.

Barry’s post was about the inability to predict the future or more specifically once you realize you can’t predict the future you are in a better position to understand that time and a simple investment strategy that ignores the short term can be the difference maker to a successfully executed financial plan.

The way I try to put the issue of time and the advantage of longer term perspective is to ask “without looking, how did your portfolio do in the 4th quarter of 2013 and how did that compare to the market?” No one knows, without looking, because it doesn’t matter, it is just some random quarter in the past just as the current quarter will soon be some random quarter from the past.

Zooming out then to focus on the longer term, because that is the more important time frame, can hopefully serve to avoid unnecessary risks like chasing a lottery ticket biotech stock. I first used the term lottery ticket biotech a long time ago and sure enough a reader shared that he put a quarter of his portfolio in some unnamed (by him) lottery ticket that did not get a favorable FDA ruling, imploded and then went to zero. How old are you, how much do you have, how much will you need and how long would it take to recover from that type of hit?

Reading this you might snicker at having 25% in a lottery ticket but what about the investors (or mutual fund) that had 15-20% in names like Fannie Mae or Wachovia? Net net it’s not much different.

Not that investors should not use individual stocks or that advisors shouldn’t include single names in client portfolios I believe in including holdings (but of course there is no single right answer on this that is right for everyone) but a portfolio of ETFs broadly diversified combined with an adequate savings rate, the ability to remain disciplined along with the understanding that the only way this quarter (and likely this year) will play a large role in determining your financial future is if you do something truly stupid.

Your strategy is unlikely to be the best performer in a given year but that is not a prerequisite for success. There will be a few years where your portfolio is a top performer but not year in and year out because no strategy can do that but again, you don’t need it to.