Three Steps to "Good Enough" - In Praise of Simplicity, Common Sense, and Stubbornness

When we discuss stock investments, we usually talk about companies’ sales, earnings, and growth trends. Yet perhaps the main factor moving stock prices in bull and bear markets is not the fluctuation of earnings per se, but the rise or decline in price/earnings (P/E) ratios.

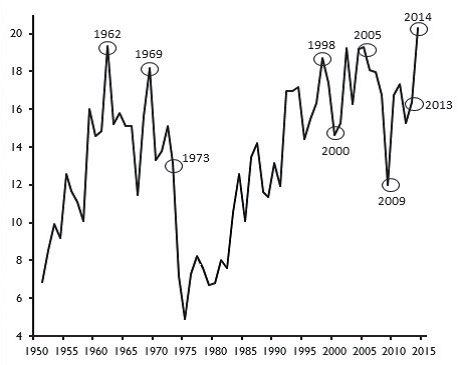

P/E ratios are not an impartial measure of value; they really reflect the investing crowd’s opinion of a price worth paying for current and future earnings. The influence of P/E ratios on stock prices is clearly illustrated by the following chart from Crestmont Research, which uses a 10-year smoothed P/E ratio to reduce the impact of earnings cycles. As can be seen in the lower part of the chart, bull and bear markets (as defined by Crestmont) correspond to periods of expansion or contraction of the S&P 500 index’s P/E ratio.

Since there are different ways to determine the beginning and end of secular market phases, I used the raw database (without adjustments) maintained by Robert Shiller at Yale University to pick the major highs and lows of the S&P 500 index since 1920 and the index’s P/E ratio on the same dates. As the resulting table (below) illustrates, it cannot be argued that fluctuations in the P/E ratio have been solely or entirely responsible for market behavior; but there is little doubt that they have been a significant contributing factor to secular bull and bear markets.

Note: In 1966-1980 and 2000-2014, the markets did show modest gains rather than outright losses; but over such long periods (14 years each), it can be deemed that prices were mostly flat. Students of secular market cycles often classify long periods of sideways prices as bear markets, since the lack of net price movement in the face of continuing earnings progress is largely due to a steady downward adjustment in P/E ratios.

Overall, as can be seen, the real money has been made when there was a significant expansion of the P/E ratio, which, as previously mentioned, is really a matter of opinion. The preponderance of the human factor in driving P/E ratios guarantees that stock prices will always be far more volatile than can be accounted for by economic forces alone. As Howard Marks puts it, “The extremes of greed and fear, and worry over missing out, will never be banished” (The Most Important Thing, Columbia University Press, 2011).

The Importance of Being Contrarian

Thus, investment markets are situated at the confluence of two sets of forces, both cyclical: economic growth and profitability on the one hand, and crowd psychology on the other. These two influences do not necessarily move in concert. Over the very long term, it is hard to argue that the stock market could make progress without the support of higher earnings. But over shorter periods, even ones lasting many years, it is the influence of crowd psychology that prevails, by causing P/E ratios to shrink or expand.

This is why it is important, in my view, to maintain a contrarian bias: If crowd psychology causes the ups and downs of P/E ratios, which in turn are a major influence on stock prices, the more pessimistic investors become about a company or a market, the closer one must be to a bottom – and, of course, vice versa.

This being said, the majority is not always wrong. If most people say that it is raining, for example, even contrarians would be well advised to take an umbrella before going out. In fact, it could even be argued that the momentum-following majority is right most of the time by assuming that what has been going up will continue to go up, and vice versa.

However, with the tendency of both optimism and pessimism to feed upon themselves to reach unreasonable extremes, a contrarian approach is most rewarding around major trend reversals, when momentum followers, at the opposite, are often caught badly unprepared. As University of California mathematician Tom Murphy reminds us in his blog Do the Math, “In almost every case, extrapolation works until it doesn’t.” More graphically, Warren Buffet reminds us that you only discover who has been swimming naked when the tide goes out.

But how do we know when we are approaching a major turning point? The fact that bull markets usually run too high and too long while bear markets usually decline more than reason would justify makes it very hard to time buy and sell decisions precisely under a contrarian approach.

Sell decisions, for example, are challenging because it is very difficult to tell at what level of a rising market people are becoming a little bit crazy, totally nuts, or raving mad. Acknowledging the futility of trying to time the end of speculative excesses, both Bernard Baruch and Baron de Rothschild, iconic market fortune-makers, claimed that they became rich by selling too early.

On the buy side, Jim Rogers, the famous “Investment Biker” who co-founded the Quantum Fund with George Soros, wrote in Adventure Capitalist (Random House, 2004):

If I do have a strength, it is the ability to look at Industry X or Country Y, on which everybody is really down, and exercise the courage, the sense, the stupidity, whatever it is, to buy it, even though everybody is telling me I am nuts to do so. If people become hostile when you say you are buying, it’s probably the right thing to do. Hostility is a great indicator. Everybody has lost so much money that they have sold the disgusting thing, and as a consequence it is really cheap.

What makes real contrarians successful is not necessarily that they dare to be different or to be wrong, but that they dare to look wrong, sometimes for quite some time. And that not only requires skill; it requires character.

The Value of Value

A contrarian bias is useful in order to be prepared for the reversal of excesses and to identify out-of-favor investment opportunities or dangerously over-loved market favorites, but it is of little help in fine-tuning the timing of long-term investors’ buy and sell decisions. Fortunately, there is some anchor for the would-be rational investor: “intrinsic value,” which is why we often describe our approach as “contrarian/value.”

Many investing icons, from Ben Graham to Phil Fisher, have deplored that “the stock market is filled with individuals who know the price of everything but the value of nothing,” as Fisher has stated. In spite of this, many investors still believe – wrongly most of the time – that stock prices reflect some kind of truth about the worth of their underlying companies. In fact, a stock really represents the ownership of a small piece of a company. When buying or selling a stock, therefore, one must keep in mind, as a reference, what price a savvy entrepreneur would be willing to pay to acquire the whole company. That is the anchor for a value investor.

Calculating the value of a business usually involves, first of all, some accounting adjustments. Some assets, such as real estate, for example, may be worth more or less today than the historical cost at which they are carried on the balance sheet. Similarly, there may be unquantified potential liabilities that may be mentioned in the footnotes to the financial statement but have not yet materialized, such as the possible outcome of pending lawsuits.

After the necessary adjustments have been estimated, the total of the company’s stock market capitalization can be compared to its net worth (total assets minus liabilities), reported earnings, sales, cash flow, and other similar measures. Depending on the company’s activities, some valuation measures are more relevant than others; but the goal is always to determine if a savvy entrepreneur or a competitor would consider acquiring the whole business at current prices.

Personally, I lean against incorporating into analyses of value too many assumptions about the future growth of the business, unless current measures have been abnormally depressed or inflated by unusual factors.

So, determining stocks’ values involves hard work. Yet, I must still warn that, while hard-nosed analysis is indispensable to effective value investing, not one of the criteria it uses can be estimated with exact or even near precision. Morgan Housel of The Motley Fool recently wrote (7/20/2015):

Some fields work with amazing precision. They are governed by pure math and physics, and aren't burdened by the whims of human emotion…investing is not one of these fields…. Find me one person who has gotten rich investing with his mathematical chops and I will show you nine who blew themselves up, plus 20 bumpkins who became rich using simple rules of thumb.

The plain truth is that in the practice of investment, “good enough,” combined with a solid dose of common sense, usually beats precision and faith in mathematical models. So, if a careful analysis has given us a “good enough” idea of a company’s worth, we can assume that its market-traded shares will fluctuate – sometimes wildly – around that fundamental value. And that may be the value investor’s salvation.

When the “Mean” Is Forgiving

Everything I have experienced or studied has convinced me that we live in a cyclical world. Real-life cycles do not exhibit precise circular or wavy patterns that could easily be used to predict the future, however. I believe the following graph is a good illustration of the famous statement, often attributed to Mark Twain: “History doesn’t repeat itself, but it does rhyme.”

In this graphic interpretation of historical progress, point B will display enough similarities with point A that economists with a good memory will experience a strong sense of déjà vu. Yet, between these two periods, many structural changes will have taken place – in societies, in world trade flows, and in technology, for example. As a result, point B will resemble point A, but it will also be different in enough respects that precisely forecasting what B will look like or exactly when it will occur is all but impossible. The only near-certainty is that there will be a point B.

Fortunately, the value investor who believes in cycles, as I do, can rely on a well-known tendency of markets: the tendency to “regress to the mean.”

In life, there are measures that can only fluctuate within a horizontal range, between an upper and a lower limit – for example, ratios that can only potentially fluctuate between 0 and100, such as stocks’ P/E ratios. To cycle periodically from the upper to the lower levels of their historical range, these measures need to cross their historical average level, which is called “regressing to the mean.”

Many cycles can be better pictured as broad fluctuations, not around a horizontal average line, but around a rising or declining trend line. This is the case of a country’s GNP, for example. In such cases, the cyclicality is referred to as “regression to trend.”

In investing, regression to the mean and regression to trend have the same implication: If you are only wrong on the timing of an investment (not on its fundamental attractiveness), the next cycle will usually bail you out.

Howard Marks wrote in Oakmark’s January 9, 2009, letter:

Situations in which mean reversion does not happen are rare enough as to make a mean reversion assumption a consistent friend to the investor.

James Montier added, in a December 2010 letter from the investment firm GMO:

In order for mean-reversion-based strategies to work, it is not required that the mean be realized for long periods of time…. As long as markets display such bipolar disorder and switch from periods of mania to periods of depression, then mean reversion should continue to merit worth as an investment strategy.

In a cyclical world, and equipped with only “good-enough” tools, it would be unrealistic and possibly dangerous to expect to make money quarter after quarter or even year after year. The realistic key to successful investing is to make more money in good times than you give back in bad times. This means that, if you believe my earlier description of markets, all you need to succeed is patience or, if you prefer, stubbornness.

An added advantage of this attitude is that when a stock that you purchased falls further below its mean, you can buy more of it, thus lowering your average cost and increasing your potential ultimate gain.

A Current Reality Check

Using Shiller’s database as earlier, I calculate the P/E ratio of the S&P 500 index to be about 21 currently vs. 30 at the 2000 top, so one could argue that the market valuation has become more reasonable since the peak of the last secular bull market. On the other hand, the long-term mean of the P/E stands lower, at around 15. The interesting thing about regression to the mean is that stock prices rarely stop there: The nature of their cyclical fluctuation is that they regress to the mean on the way to the next cycle, high or low. This would imply that the downward adjustment in the S&P 500 P/E ratio still has some way to go.

Another intriguing factor is that the median P/E of stocks listed on the NYSE is at a record high, as illustrated by the Wells Capital Management graph below (1/8/2015). Other graphs in the same report show different measures of value, such as the median ratios of Price to Cash Flow or Price to Book Value, to be in similarly extended situations.

*Based on all NYSE stocks with positive earnings for the last fiscal year calculated in June of each year since 1951 through 2014

A median is a number for which there are as many measures above it as below, which implies that many stocks are even more overextended than the median but also that, perhaps, not all stocks are overextended.

Intrigued by that thought, I checked some of the past year’s purchases in the portfolios we manage. Many were bought at prices 30 to 50 percent below their five-year highs, and quite a few are still selling well below these highs.

Stubbornness and Opportunism

After the strong recoveries since the 2009 lows, the major stock markets hardly look to be propitious ground for bargain-hunting, particularly that of the United States. But the way that leading indexes are constructed can make them very misleading. For example, The Wall Street Journal recently pointed out (8/3/2015) that six stocks – Amazon, Google, Apple, Facebook, Gilead, and Disney – accounted for more than the entire gain in the capitalization-weighted S&P 500 year-to-date. Admittedly, that total gain has been less than 2 percent, but such instances of index performance traceable to only a few stocks are not that rare, and they often indicate a worrisome narrowing in the breadth of a market trend.

To further investigate, I asked one of our interns to compare the current price of all the stocks in the S&P 500 index to their five-year highs. For background, the S&P 500 has recently been hovering around an all-time record (2098), which is 56 percent above its 2011 high of five years ago (1364). What we found out, however, is that almost one-fifth of the stocks making up the index are currently down 30 percent or more from their five-year highs, which would qualify as a fairly major bear market if it could be said of the whole index!

This seems like an ideal time to exercise what Howard Marks calls “patient opportunism”: to wait for bargain levels in the general markets while we opportunistically seize investment opportunities in out-of-favor and attractively priced individual stocks.

(c) Tocqueville Asset Management