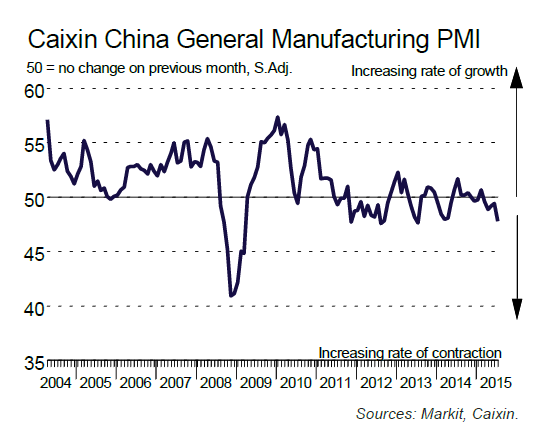

The week started off poorly with the Chinese PMI dropping from 49.4 to 47.8. The overall trend for this indicator is clearly lower:

This release led to a harsh early week commodity sell-off. The Chinese stock market appears to have stabilized around the 200 day EMA, but only after a tremendous amount of interference from the Central government. China remains a large point of concern due to its negative impact on the world economy.

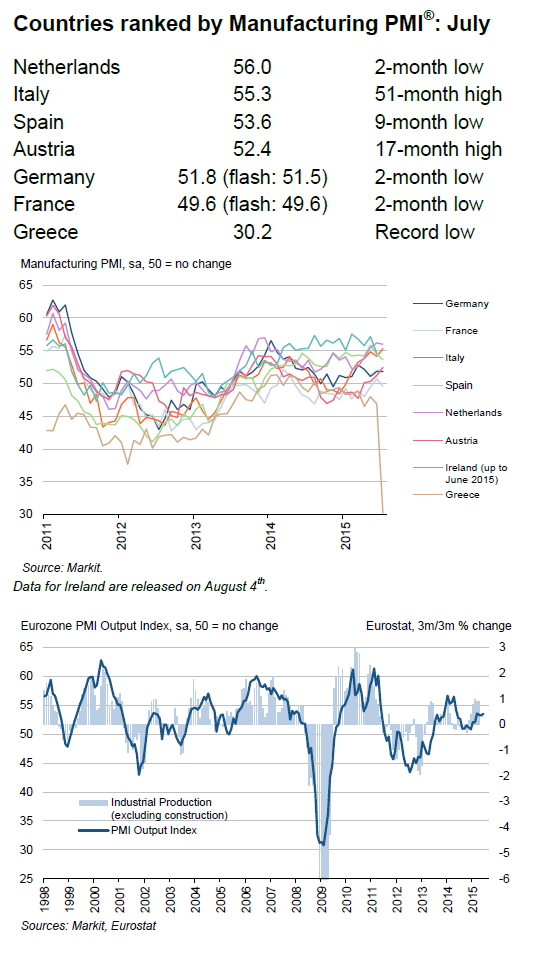

Aside from Greece, EU manufacturing news was positive. The broad EU PMI was 52.4. Overall increases in new orders for consumer, intermediate and investment goods kept the number in positive territory. Three of the four largest economies had positive numbers: Germany’s was down .1 to 51.8, Spain had a positive 53.6 and Italy’s was a very impressive 55.3. Only France saw a contractionary reading, and then just barely at 49.6. Here are the charts and important data points from the report:

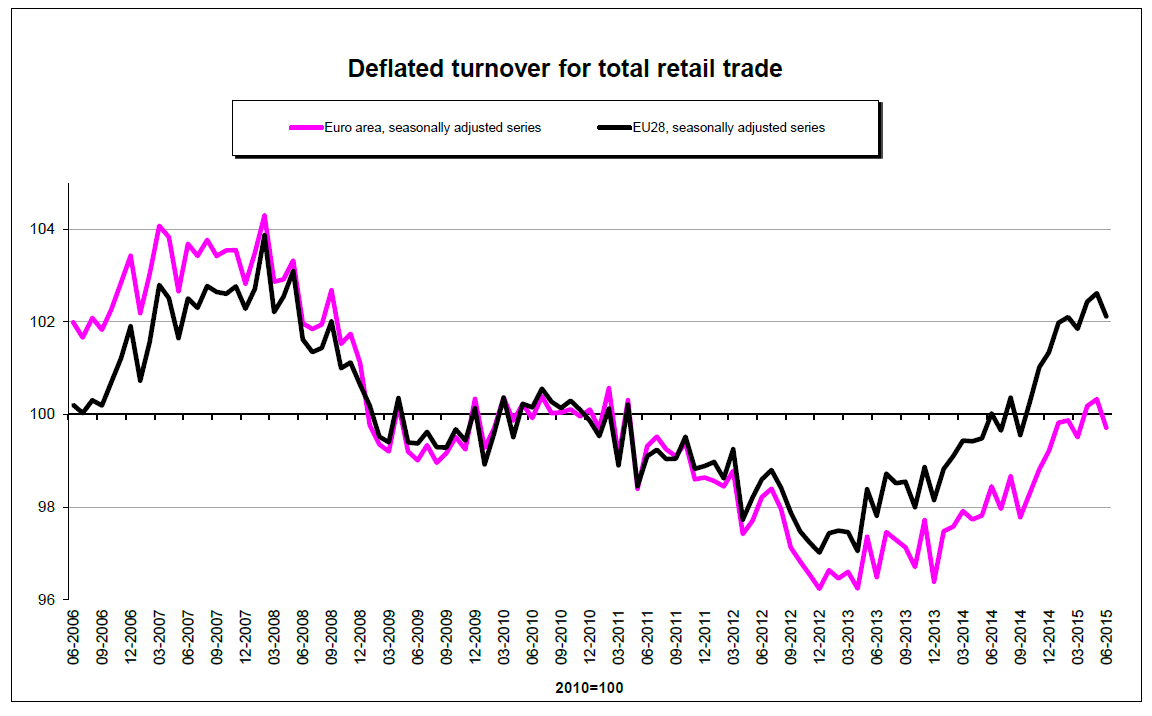

The EU service sector is on firmer ground. The German reading was 53.8, France’s 52, Spain’s a very impressive 59.7 and Italy’s 52. The combined totals of all numbers led to an EU composite reading of 53.9, with employment, new orders and overall activity in positive territory. EU retail sales were off .6% M/M but up 1.2% Y/Y. As this chart from the report shows, the overall trend is very positive:

The Reserve Bank of Australia maintained rates at 2%, offering the following assessment of the domestic economy:

The global economy is expanding at a moderate pace, but some key commodity prices are much lower than a year ago. Much of this trend appears to reflect increased supply, including from Australia. Australia's terms of trade are falling nonetheless.

…..

In Australia, the available information suggests that the economy has continued to grow. While the rate of growth has been somewhat below longer-term averages, it has been associated with somewhat stronger growth of employment and a steady rate of unemployment over the past year. Overall, the economy is likely to be operating with a degree of spare capacity for some time yet. Recent information confirms that domestic inflationary pressures have been contained. That should remain the case for some time, given the very slow growth in labour costs. Inflation is thus forecast to remain consistent with the target over the next one to two years, even with a lower exchange rate.

The unemployment rate increased to .2% to 6.3%, although the trend remains in the low 6% range:

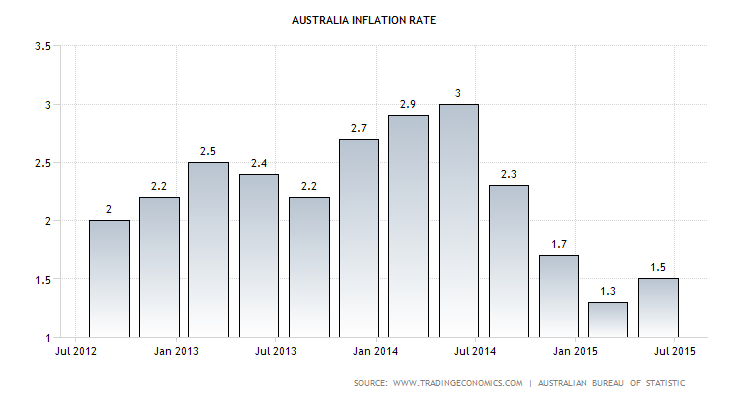

Inflation is benign, giving the bank ample room to maneuver:

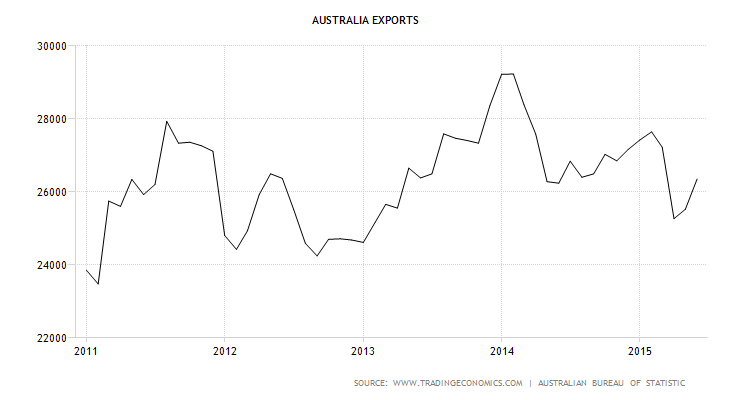

The bank is concerned about overall terms of trade although the Australian dollar is trading near 5-year lows versus the dollar and yuan. This, along with the lackluster rate of growth, indicates a future rate cut may be in the cards. While exports were up 3% M/M, the overall trend is still lower since the beginning of 2014.

The Australian industry groups’ manufacturing PMI was up 6.2 to 50.4. But the positive reading is misleading: only 3/8 subsectors increased with only 4/7 sub-indexes above 50. The service index, which has been positive all year, rose 2.9% to 54.1. All industries were expanding, with sales increasing at the fastest pace since February 2007.

The Bank of England kept rates at .5%. They noted inflation was muted, mostly as a result of low commodity prices. The policy announcement contained the following assessment of the domestic economy:

Private domestic demand growth in the United Kingdom is expected to remain robust. Household spending has been supported by the boost to real incomes from lower food and energy prices. Wage growth has picked upas the labour market has tightened and productivity has strengthened. Business and consumer confidence remain high, while credit conditions have continued to improve, with historically low mortgage rates providing support to activity in the housing market. Business investment has made a substantial contribution to growth in recent years. Firms have invested to expand capacity, supported by accommodative financial conditions. Despite weakening slightly, surveys suggest continued robust investment growth ahead. This will support the continuing increase of underlying productivity growth towards past average rates.

…..

Sterling has appreciated by 3½% since May and 20% since its trough in March 2013. The drag on import prices from this appreciation will continue to push down on inflation for some time to come, posing a downside risk to its path in the near term. Set against that, the degree of slack in the economy has diminished substantially over the past two and a half years. The unemployment rate has fallen by more than 2 percentage points since the middle of 2013, and the ratio of job vacancies to unemployment has returned from well below to around its pre-crisis average. The margin of spare capacity is currently judged to be around ½% of GDP, with a range of views among MPC members around that central estimate. A further modest tightening of the labour market is expected, supporting a continued firming in the growth of wages and unit labour costs over the next three years, counterbalancing the drag on inflation from sterling.

Of particular note is their opening a paragraph noting the Sterlings increased value over the last few years. It’s almost as though they are letting the appreciated currency do the work of slowing the economy and inflation for them as opposed to raising rates. They may also be telegraphing that they more than understand a UK rate increase will naturally appreciate the Sterling, multiplying the impact of a rate hike. The UK’s Markit PMI was 51.9. But only the consumer orders number was positive. The strong Sterling has negatively impacted intermediate and investment goods for about a year as show in this chart from the report. Construction was stronger with a 57.1 reading. While residential and civil activity decreased, commercial real estate was up. Finally, production output increased 1.5% Y/Y.

As always, US data will be covered more completely in the US Equity and Economic Review. The ISM manufacturing number deceased from 53.5 to 52.7. The services number was very strong at 60.9. And employment increased by 215,000. The lack of growth in manufacturing jobs shows the impact of the strong dollar and oil sector decline.

The BOJ maintained their current rate and asset purchase policy. Japanese industry is expanding moderately. The Markit manufacturing PMI increased from 50.1 – 51.2, with production, new orders and exports higher. The weaker yen is clearly helping. Toyota, for example, had a large increase in sales partly as a result of the lower yen:

Toyota, the Japanese carmaker, has eked out a record quarterly net profit as the weaker yen offset a slowdown in vehicle sales in most regions outside of North America.

…..

Excluding the currency benefits, its first quarter operating profit would have fallen 12 per cent instead of rising 9 per cent. During the quarter, Toyota’s average exchange rate was Y121 against the US dollar compared with Y102 during the same period last year.

Services are also contributing, with a 51.2 composite reading. Activity, new orders and employment are all up.

The biggest story this week was the overall commodity decline along with its implications. Chinese demand is slowing, which is lowering trade flows. And developing countries are experiencing a double whammy, as not only are their raw material expoets declining, but the potential for a Fed rate hike is putting a bid under the dollar and a number of sell orders on developing currencies. The EU continues to print encouraging numbers. Weakness in UK's inflation totals is pushing back the potential BOE rate hike. Finally, the US' strength is leading many to conclude the Fed will raise rates this year.