Infrastructure is an integral part of your daily life. You drive on it, depend on it for electricity and water, and use it to communicate on your cell phone. But have you considered investing in it? Infrastructure investment can offer several potential benefits to an overall portfolio.

Established track record

Infrastructure comprises long-lived assets in industries with high barriers to entry, typically supported by resilient demand for essential services. While “infrastructure as asset class” is a comparatively new concept in the US, it has an established track record in other countries. In the UK, Canada and Australia, infrastructure has been considered its own asset class for some time. Consider two successful examples:

- England and Wales privatized their water assets in 1989 by selling 10 publicly owned water companies and launching a new regulator. Nearly a decade later, The World Bank Group summarized the results: “These reforms have delivered an impressive volume of new investment, full compliance with the world’s most stringent drinking water standards, a higher quality of river water, and a more transparent water pricing system.”1

- In Australia, many toll roads, ports and airports are privatized. A study conducted by the Allen Consulting Group and the University of Melbourne found that infrastructure built through public-private partnerships tended to have fewer cost and time overruns when compared with traditional public-only projects.2

Dynamic, growing asset class

Over the past 10 years, total net assets in Lipper’s Global Infrastructure Funds Category have swelled from below $150 million to over $15 billion currently.3 Overall investor interest in infrastructure could continue to grow for several reasons, including:

- The possibility for increased securitization of infrastructure assets resulting from the pervasive public funding gap confronting many nations today.

- The current shift toward including alternative investments, such as real estate and infrastructure, in traditional stock/bond portfolios.

- Investors’ search for alternative sources of yield and diversification in a low interest rate environment.

Benefits for investors

Global infrastructure has historically provided competitive total returns relative to broad markets. For the 10 years ended June 30, 2015, the Dow Jones Brookfield Global Infrastructure Index returned 10.4% in average annual returns versus the MSCI World Index return of 6.4%.4 Equally compelling, a significant portion of infrastructure returns comes from recurring income. The current dividend yield on the Dow Jones Brookfield Global Infrastructure Index is 3.7% versus 2.5% for the MSCI World Index.5

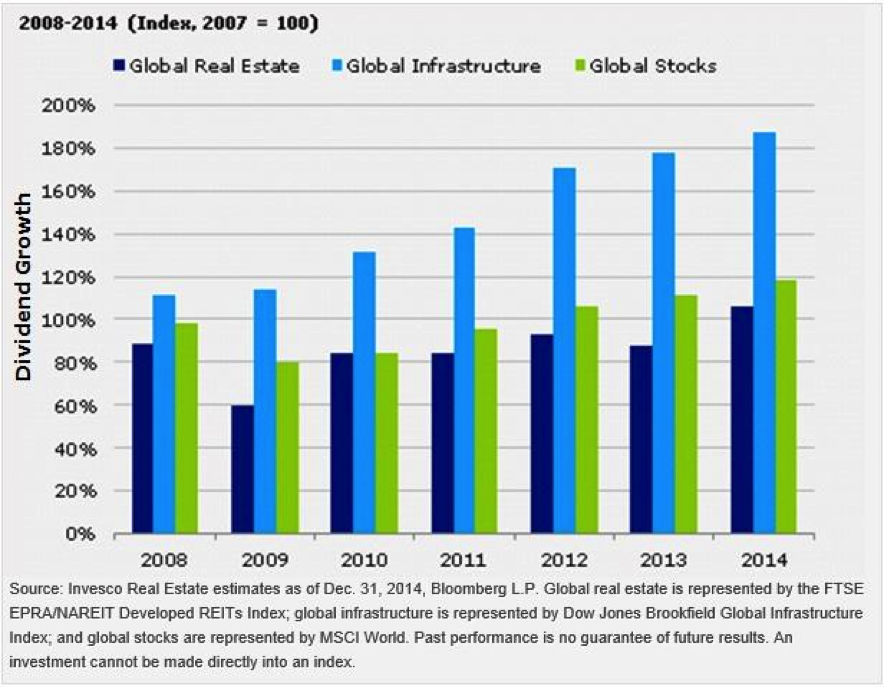

Moreover, the contractual nature of infrastructure cash flows tends to both enhance their predictability and lower financial risk, thus potentially boosting the risk-adjusted performance of the asset class. Global infrastructure has experienced 13% annual dividend growth in the years following the Great Recession, compared with 3% and 1% annual dividend growth for global stocks and global real estate, respectively.6 The path of dividend growth is important as well. As the chart below shows, infrastructure has experienced annual consecutive growth since 2008 — even in 2009, when dividends on both global stocks and global real estate shrank.

Infrastructure has experienced annual dividend growth since the Great Recession

Finally, Infrastructure has provided inflation-hedging and diversification characteristics historically. In a review of inflationary periods — defined as the US consumer price index above 2.5% — US infrastructure stocks outperformed US stocks by 6.5% annualized.7 Additionally, correlation of global infrastructure relative to US fixed income is low at 0.27.8

I believe these potential benefits make a compelling case for considering an investment in the infrastructure that you likely take for granted every day.

This two‐part series examines the expanding capital requirements for infrastructure globally as developed markets confront ongoing replacement needs, and the urbanization of emerging markets places additional stress on the existing foundation. This second part explores what this macro trend may mean for investors. The first part: Bridging the gap in global infrastructure funding.

1 Source: The World Bank Group, Public Policy for the Private Sector, “Water Privatization and Regulation in England and Wales, May 1997

2 Source: Infrastructure Partnerships Australia, “Performance of PPPs and Traditional Procurement in Australia,” November 2007

3 Source: Lipper, as of June 30, 2015

4 Source: Invesco Real Estate, Zephyr StyleADVISOR, as of June 30, 2015

5 Source: Bloomberg L.P., as of June 30, 2015

6 Source: Invesco Real Estate, Bloomberg L.P., as of December 31, 2014

7 Source: Invesco and Zephyr, as of December 31, 2014. US infrastructure average calculated using a simple average of annual returns of the S&P 600 Water Utilities, the S&P 500 Utilities Sector, and the S&P 500 Road and Rail indexes. US stocks represented by the S&P 500 Index.

8 Source: Zephyr StyleADVISOR, from January 2003 to June 2015, based on the Dow Jones Brookfield Global Infrastructure

Index correlation relative to US equities (the S&P 500 Index) and US fixed income (Barclay’s US Aggregate Index)

Important information

Dividend yield is the amount of dividends paid over the past year divided by a company’s share price.

Correlation is the degree to which two investments have historically moved in relation to each other.

The FTSE EPRA/NAREIT Developed Index is an unmanaged index considered representative of global real estate companies and REITs.

The MSCI World Index is an unmanaged index considered representative of stocks of developed countries.

The S&P 500® Index is an unmanaged index considered representative of the US stock market.

The consumer price index measures the prices consumers pay for a basket of consumer-based goods and services.

The Lipper Global Infrastructure Funds Category represents all funds Lipper deems global infrastructure funds.

The Dow Jones Brookfield Global Infrastructure Index measures the stock performance of companies that exhibit strong infrastructure characteristics.

Barclay’s US Aggregate Bond Index is an unmanaged index considered representative of the US investment-grade, fixed-rate bond market.

The S&P 600® Water Utilities Index is a float-adjusted, market-capitalization-weighted index representing the US small-cap market water utilities industry.

The S&P 500® Utilities Sector Index is an unmanaged index considered representative of the utilities market.

The S&P 500® Road Index is an unmanaged index considered representative of US toll road stocks.

The S&P 500® Rail Index is an unmanaged index considered representative of US rail stocks.

Diversification does not guarantee a profit or eliminate the risk of loss.

Investment in infrastructure-related companies may be subject to high interest costs in connection with capital construction programs, costs associated with environmental and other regulations, the effects of economic slowdown and surplus capacity, the effects of energy conservation policies, governmental regulation and other factors.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2015 Invesco Ltd. All rights reserved.

An alternative asset class you may take for granted by Invesco Blog