The Fed’s policy statement was the main economic event this week; its opening paragraph began, “Growth in household spending has been moderate and the housing sector has shown additional improvement; however, business fixed investment and net exports stayed soft.”

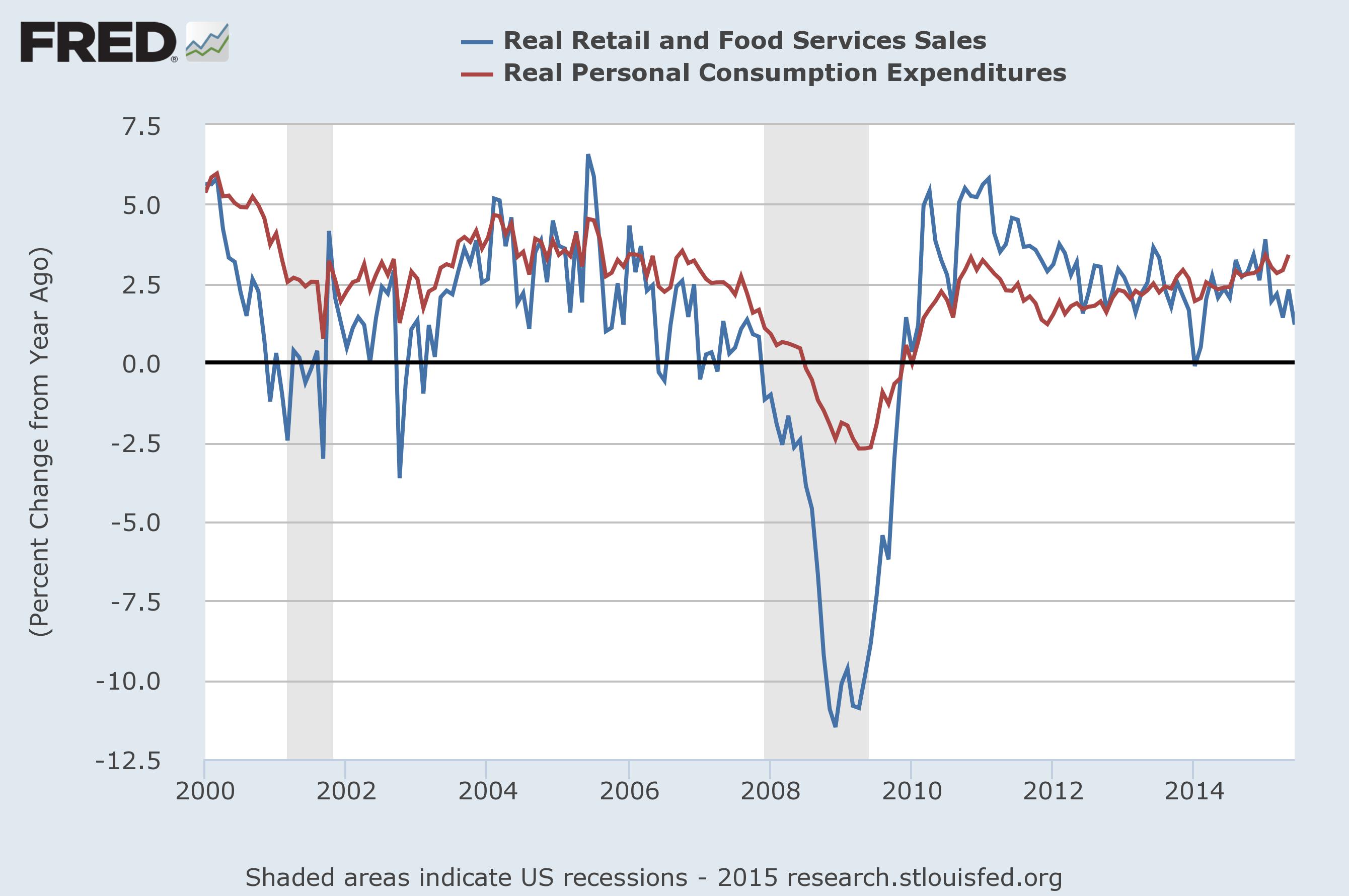

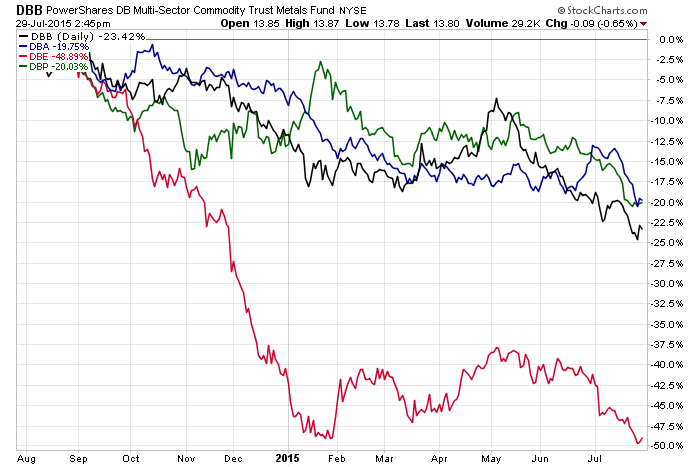

PCEs and retails sales are clearly expanding Y/Y, but at a lower rate than the early 2000’s expansion (which itself wasn’t exactly the strongest period of growth on record). Interestingly, the Fed didn’t mention the causation of lower business investment and exports, namely, the weak oil sector along with the strong dollar. Regarding employment, they noted, “[t]he labor market continued to improve, with solid job gains and declining unemployment. On balance, a range of labor market indicators suggests that underutilization of labor resources has diminished since early this year.” Some indicators are still weak. The percent of the unemployed without a job over 27 weeks is still high while the employment to population level only recently started increasing. Other measures like the unemployment rate and initial jobless claims are strong. The announcement continued, “Inflation continued to run below the Committee's longer-run objective, partly reflecting earlier declines in energy prices and decreasing prices of non-energy imports.” Oil isn’t the only commodity with weak prices; in fact, there is little pricing power in the entire raw materials complex as shown in this chart of the broad commodity ETFs:

All are down for the year. In short, price pressures are more than contained, giving the Fed ample policy room to keep rates low if they choose so.

The BEA reported US GDP increased 2.3% in the second quarter:

Real gross domestic product -- the value of the production of goods and services in the United States, adjusted for price changes -- increased at an annual rate of 2.3 percent in the second quarter of 2015, according to the "advance" estimate released by the Bureau of Economic Analysis. In the first quarter, real GDP increased 0.6 percent (revised).

.....

The increase in real GDP in the second quarter reflected positive contributions from personal consumption expenditures (PCE), exports, state and local government spending, and residential fixed investment that were partly offset by negative contributions from federal government spending, private inventory investment, and nonresidential fixed investment. Imports, which are a subtraction in the calculation of GDP, increased.

The US economy grew a revised .6% in the first quarter. The most recent number showed a marked improvement in consumer spending which rose 2.9% Q/Q in 2Q15 compared to a 1.8% rise in the first. Spending on both durable and non-durable goods increased smartly (7.3% and 3.6%, respectively). And despite the strong dollar, exports increased 5.3% from the previous quarter. But the oil patch’s slowdown was evident in the 4.1% contraction in equipment investment. Commercial real estate investment was also off 1.6%. Overall, the report indicated the first quarter slowdown was in fact weather and port strike related.

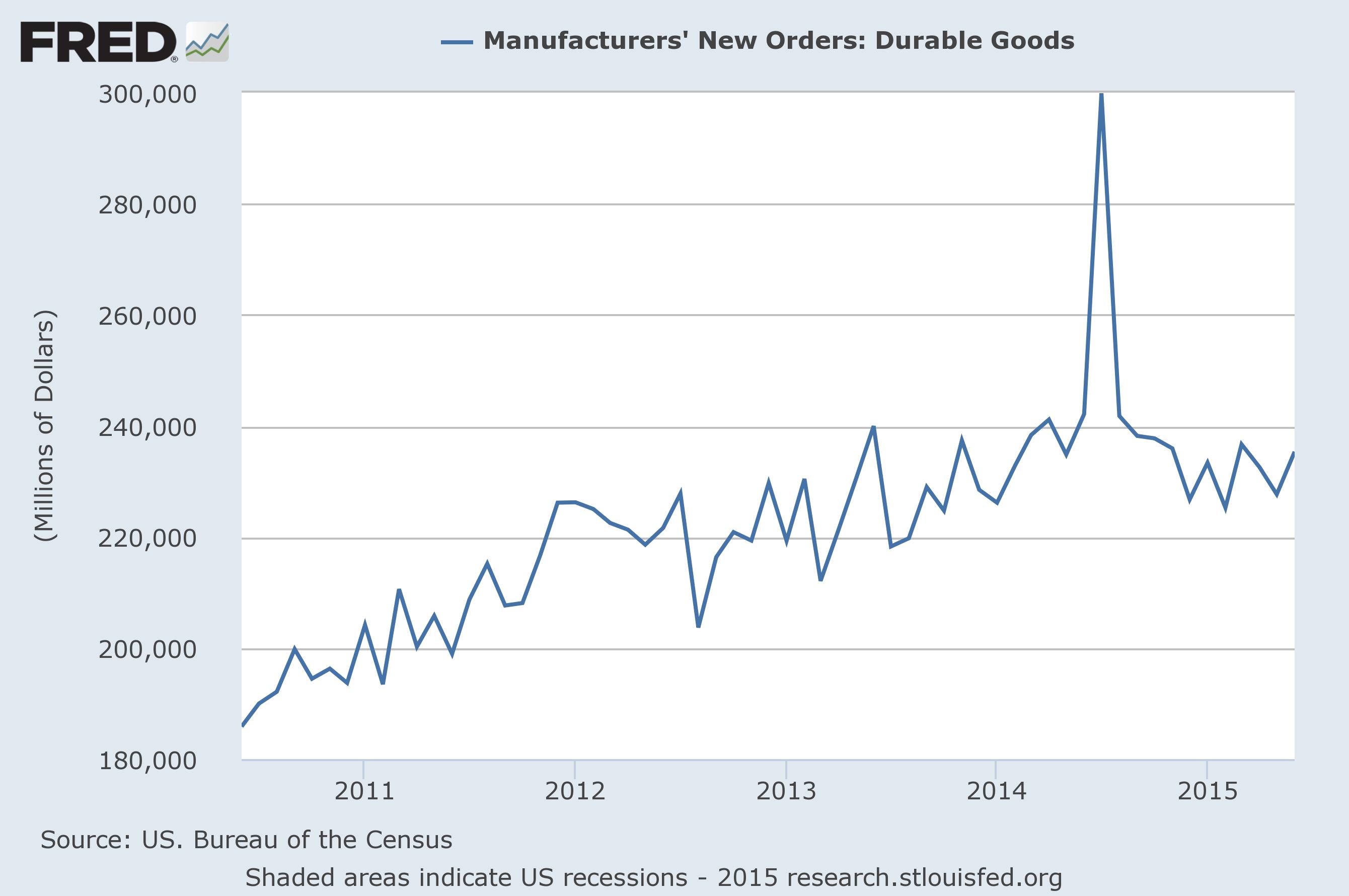

Finally, durable goods orders increased 3.4% from the previous month; they were up .8% ex-transports. Despite the increase, this number has stalled between $220-$240 billion for the last year, save for the large spike in mid-2014:

Conclusion: this week’s news was positive. 2nd quarter GDP and durable goods rebounded while the Fed gave a positive assessment of the economy. The macro backdrop is equity positive.

The Market

This week I want to highlight several internal market issues that are issuing warning signs. This does not mean the market is about to crash or even enter a bear market. But it does mean we should not only be aware of these developments but continue to follow them.

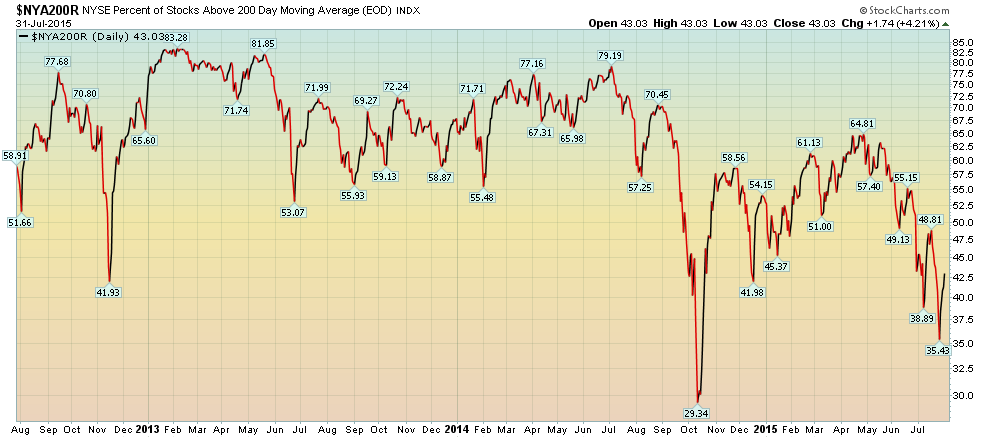

Let’s begin by looking at the number of NYSE stocks above their 200 day EMA:

From 2013 through most of 2014, this number reached highs between 61%-70%. But earlier this year, this index couldn’t get higher than the low 60% range. And in the last few months, the indicator has dropped below 50%.

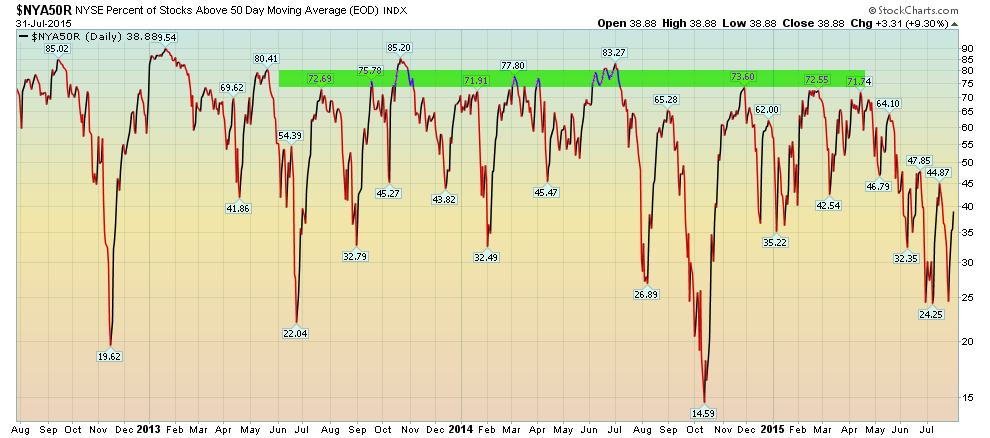

And turning to the number of stocks above their 50 day EMA, the picture dims further:

From mid-2013 through mid-2015, this number peaked from the low 70%s to the low 80%s. But for the last few months, it has vacillated between 25% and 47%, indicating less than half NYSE stocks are trading above their 50 day EMA.

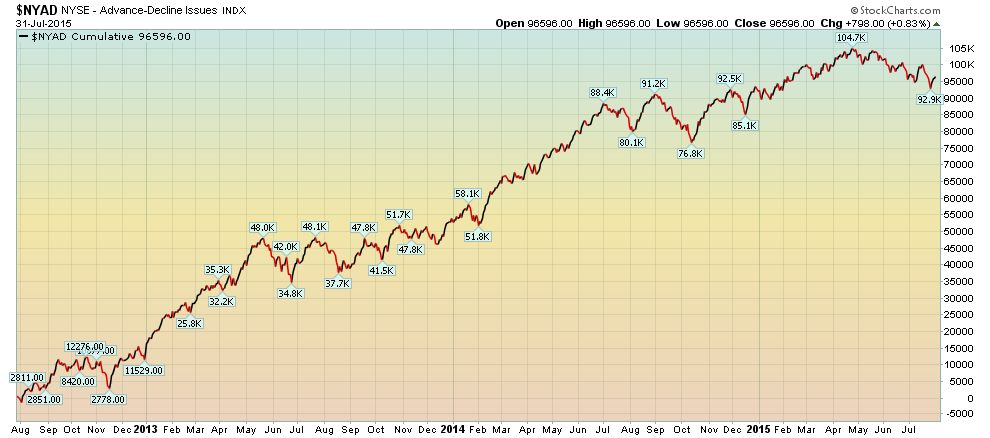

And finally, we have the NYSE cumulative Advance decline line, which shows a drop over the last 3-4 months:

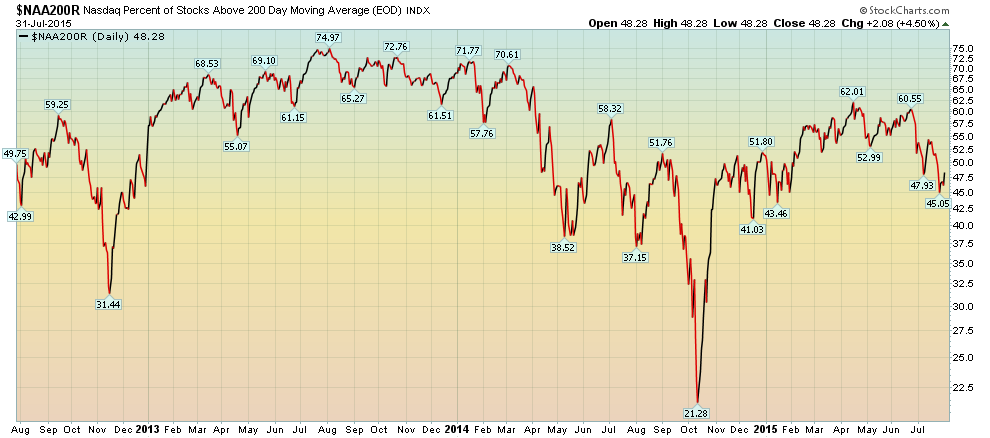

Let’s turn to the NASDAQ by starting with the percentage of stocks above the 200 day EMA:

From 2013 through early 2014, this number peaked in the high 60s to low 70s. But since, the best it can muster is the high 50s/low 60s.

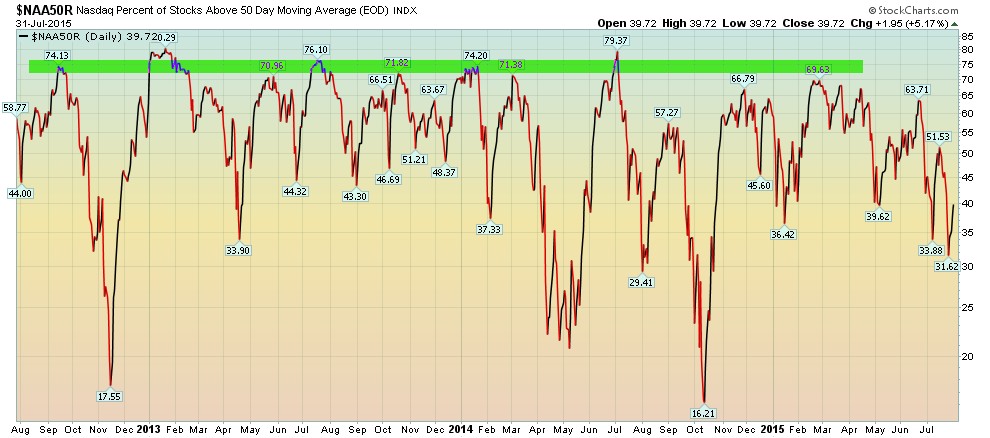

The number of stocks above the 50 day EMA is a bit different:

This index shows that the number of companies above their respective 50 day EMA peaked in the upper 60s/lower 70s for much of the last few years. Recently, however, it has dropped as low as 30%.

And finally there is the NASDAQ’s cumulative advance decline line:

This number actually started moving lower in 2014, and continued to drop that year. It moved sideways in 2015 until just recently, when it started moving lower again.

There is only one conclusion to draw from these indicators: the number of stocks supporting the market has been declining for some time. As fewer and fewer stocks provide a foundation for the market, the natural conclusion is indexes will start to move lower. At minimum, declining breadth explains the lack of meaningful advances in the market for most of this year. To a certain extent, this is the natural result of an expensive market; as more and more traders look at valuations and conclude the market is pricey, they are more inclined to sell at least some of their positions to take some profit off the table.