The End of U.S. Sovereign Debt as a Near Perfect Protection Asset

For the past 30 years, the paradigm portfolio holding 60-percent stocks and 40-percent government debt seemed to exhibit a reasonable mix of both growth and protection, being a simple allocation the market beta of two very liquid asset classes with low (occasionally negative) correlation.

Low fees, broad diversification, and regular rebalancing produced reasonable returns with about half the drawdowns of investing wholly in equities. Most important, sovereign debt was the source of cash in a crisis providing investors with strong total returns and the ability to easily sell and generate cash for rebalancing. In other words, when equity markets suffered, investors were usually able to harvest gains on bonds to buy more stocks at lower prices. Investors had confidence in bonds.

In fact, we believe U.S. intermediate term government debt1 in the post-Volcker era was very close to a perfect asset, particularly within the context of modern portfolio theory. Dan Ferris of Stansberry & Associates Investment Research offers a description of a perfect asset that we have slightly modified here with respect to the allocation of bonds jointly with equities. We believe a perfect protection asset in a portfolio also holding equity securities for growth would:

• Have rates of return always in excess of inflation

• Have little or no default risk

• Be completely liquid

• Be negatively correlated with equities, particularly in times of crisis

• Require little active management other than rebalancing

To achieve portfolio balance when holding growth assets, we believe investors need very liquid assets that go up in value when growth falters. Key to portfolio balance is the ability to harvest cash from assets that have risen in value and use it to purchase additional growth assets when their prices collapse. For the past thirty years, U.S. government debt, in our opinion, met this requirement better than most alternatives. However, in our opinion, one of the five features of a perfect protection asset may be missing for intermediate term sovereign debt as we move forward. We believe rates of return on intermediate debt will not exceed inflation as readily as occurred over the past thirty years. We also believe that a high negative correlation will not prove favorable in this regard, and that holding U.S. treasury bills will prove a better source of protection than longer duration instruments.

THE ACTIVE MANAGEMENT OF FINANCIAL CRISES BY THE FEDERAL RESERVE

Most investors’ experience over the period from about 1987 through the present provided regular evidence that the 60-percent stock / 40-percent bond portfolio offered both a balance between growth and protection. We believe this was the result of the Federal Reserve’s monetary policy.

Alan Greenspan was confirmed as Chairman of the Board of Governors of the Federal Reserve on August 11, 1987. Roughly two months later, as U.S. equities declined more than 22 percent in a very short time, the Federal Reserve issued a short statement in which it affirmed the readiness of the Federal Reserve “to serve as a source of liquidity to support the economic and financial system.”2

For most of the years since, we have seen the Federal Reserve respond similarly to six or seven spasms of broad market volatility and the subsequent evaporation of system liquidity. After the 1987 stock market crash, we witnessed financial engineering gone awry with the 1994 failure of Orange County, California; the 1995 Mexican peso collapse; LTCM’s too-big-to-fail crisis on the heels of the Russian default; a tech bubble that burst in 2000; accounting frauds in 2002; and a real estate bubble that collapsed in 2007, morphing into the ultimate too-big-to-fail crisis in 2008. Each spasm generated continuing evidence supporting the role of equities and U.S. sovereign debt in the 60/40 portfolio: First, equities could be extremely volatile but always recovered, and second, in a market crisis, regardless of origins, the Federal Reserve would lower short-term interest rates. But it is our opinion that interest rates have now gone about as low as they can go, and it’s time to find another near perfect asset.

If we examine the long-term performance of fixed income, we see that inflation, and the central bank’s early battles to manage rates, paint a much different picture of total returns in the period from 1942 to 1982 than in the thirty or so years that followed. During this time span, total real returns of U.S. intermediate government debt were often negative. The first ten years of low or negative returns came from bouts of inflation during a period in which nominal rates were kept low. The next thirty years saw rising nominal yields and rising inflation combine to offer investors a mixed bag of negative real returns punctuated with a few years in which real returns exceeded 5%.

Once inflation reached the lofty levels of the late 70s and early 80s and peaked, so began the ‘golden age’ of fixed income in which strict monetary policy and radically increased productivity fostered by technological innovation loosened labor’s grip on wage growth. Falling inflation begat falling nominal yields, rising bond prices, and large annual real returns from fixed income securities. Yields on mortgage-backed securities, high yield bonds and dollar-denominated emerging market debt generally declined as well, delivering generous total returns from all forms of debt beginning in 1982 and continuing to the present.

While we expect on-going management of rates by the Federal Reserve amid continued de-leveraging by households and the financial sector to keep intermediate

U.S. Treasury note yields from rising much above 4% over the next decade, we don’t expect high total returns. In our opinion, interest rates will likely decline whenever the economy suffers a spasm of low growth, but we also think the resulting jump in yields following those spasms will cause sharp losses.

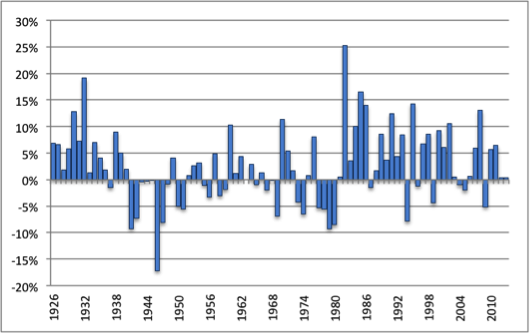

Real Returns of U.S. Intermediate Treasury Notes:

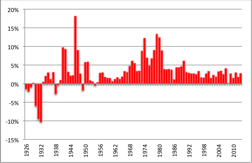

Nominal Yields on U.S. Intermediate Treasury Notes:

Annual Inflation Used to Calculate Real Returns:

All data used for the three charts above come from the Morningstar 2012 Ibbotson® SBBI® Classic Yearbook. “Real” returns are total returns adjusted for inflation. A simple approximation of inflation-adjusted returns can be calculated by subtracting the annual inflation rate from the annual total return of an asset class. Morningstar calculated total returns for intermediate-term U.S. government notes for the period 1987-2012 using prices from The Wall Street Journal from 1987 to 2012, and from the CRSP Government Bond file for the period 1934 through 1986.

1 Intermediate term to maturity U.S. government debt are notes maturing between 2 years and 10 years, and all data here refer to time series of notes with 5 years to maturity. In fact, the average maturity of government debt issued tends to be around five years as well.

2 Carlson, Mark. “A Brief History of the 1987 Stock Market Crash with a Discussion of the Federal Reserve Response”, 10. Finance and Economics Discussion Series. The Federal Reserve Board, 1 May 2007.

Disclosure

Larkin Point Investment Advisors LLC (“Larkin Point”) is an investment advisor registered with the U.S Securities and Exchange Commission. Registration with the U.S Securities and Exchange Commission does not constitute an endorsement of the firm by the Commission, nor does it indicate that Larkin Point has attained a particular level of skill or ability. Larkin Point is not a registered broker-dealer in the United States. Larkin Point is not registered under the laws of any foreign jurisdiction and this report shall not be deemed a solicitation of any investors or clients in contravention of any such foreign laws and regulations.

The statements and material appearing in this report have been prepared, except as otherwise noted, by Larkin Point, contain confidential or privileged information, and should not be read, copied or otherwise used by any other persons.

This publication is for your information only and is not intended as an offer, or a solicitation of an offer, to buy or sell any investment or other specific product. The analysis contained herein does not constitute a personal recommendation or take into account the particular investment objectives, investment strategies, financial situation and needs of any specific recipient. It is based on numerous assumptions. Different assumptions could result in materially different results. We recommend that you obtain financial and/or tax advice as to the implications (including tax) of investing in the manner described or in any of the products mentioned herein.