Infrastructure is the backbone of every economy, providing essential public services such as water supply, energy and mobility. And for investors, infrastructure also has the potential to provide unique benefits. In general:

- Infrastructure assets, such as airports, ports, railroads and water utilities, tend to have long useful lives, generating cash flow over a long duration — sometimes a century or more.

- Demand for infrastructure is relatively independent of business cycles. Therefore, assets tend to produce regular, stable cash flows that allow pricing adjustments for rising inflation rates. Fees for using a toll road or a pipeline, for example, are normally linked to an inflation rate.

- Infrastructure assets essentially operate as quasi-monopolies — for example, electric transmission lines — with little or no competition because the upfront investment for construction is substantial and usually irreversible.

Sweeping need, scarce funding

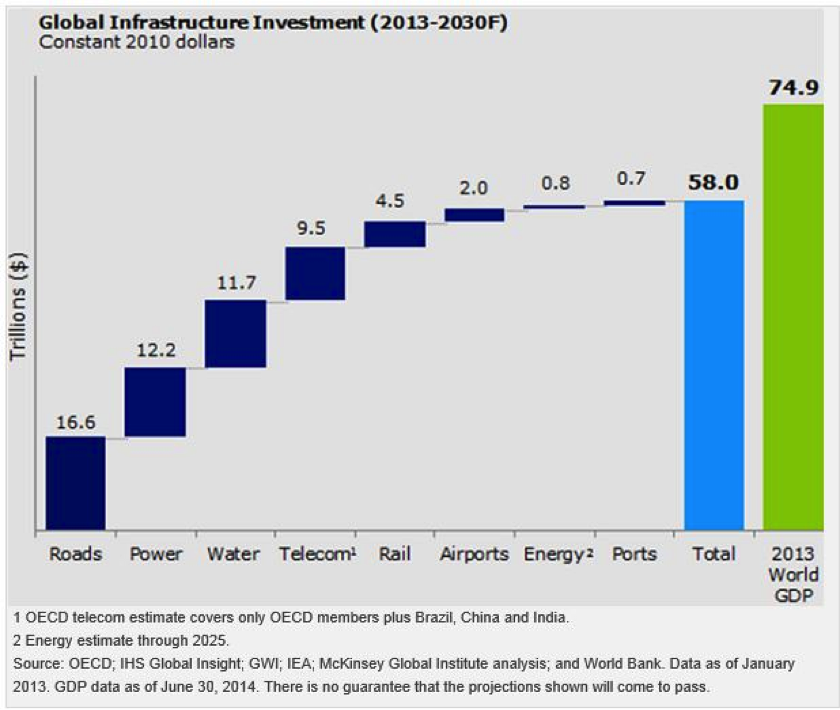

There is a crucial, expanding demand for infrastructure around the globe. Emerging economies need infrastructure to support increased urbanization as well as the expansion of the middle class. Developed countries need investment for upgrading and improving existing aging infrastructure, which often has become inadequate to support current demand. Current estimates place the global infrastructure investment need at $58 trillion. To put this number in perspective, worldwide gross domestic product (GDP) was almost $75 trillion in 2013, as the chart shows.1

Global infrastructure investment need is estimated at $58 trillion

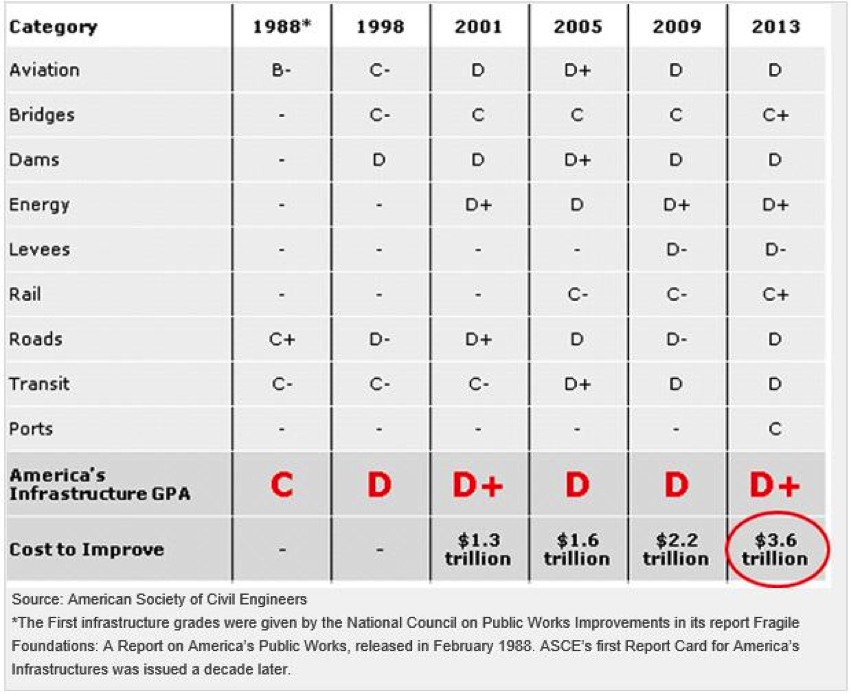

In the US in particular, lack of government spending has left infrastructure assets in poor shape. As you can see from the infrastructure “report card” from the American Society of Civil Engineers, the spending gap between infrastructure funding and needed improvements was a staggering $3.6 trillion in 2013. That number is expected to grow to $10 trillion by 2040.2

Grading US infrastructure: D+ with a $3.6 trillion spending gap

With the national debt just over $18 trillion,3 the federal government has limited resources to close that infrastructure funding gap, which has been building over the last decade with a notable decrease in federal as well as in state and local government infrastructure spending.4 More significantly, the last decade saw a decrease of 23% in capital expenditures for infrastructure, while operations and maintenance spending increased 6% over the last decade.5

Bridging the gap

The use of private funds in public works is quite common outside the US. For example, TransUrban Group, a publicly traded Australian company, develops and manages almost all the country’s toll roads, including the Cross City Tunnel, which is strategically located to reduce travel time to the Sydney Airport and, by extension, increase toll revenues for TransUrban shareholders.

Most airports outside the US are publicly listed and post significant earnings from their retail business tenants as well as from airline passenger fees. Earlier this year, Spain’s government announced the initial public offering (IPO) of 28% of Aena, the world’s largest airport operator by passenger volume.6 In addition to the IPO, the government planned to sell a 21% stake in Aena to private investors. Although Aena will remain state owned with a 51% majority stake, the government expects to reap $4.5 billion from the minority interest sale.

The US appears to be slowly following suit, although public-private partnerships are considered the new rather than the norm. The Port Authority of New York & New Jersey, for example, recently announced an “innovative public-private partnership” for the redevelopment of the LaGuardia Airport to create a central arrival and departure portal. LaGuardia Gateway Partners, the private investor, will contribute $2 billion and the Port Authority $1 billion to fund the project, which promises premier shopping, dining and business amenities; additional parking with a cell phone lot; and capacity for a hotel and rail connecting LaGuardia Airport to the subway.7

At Invesco Real Estate, we believe governments will look increasingly to private companies to bridge the infrastructure spending gap. These partnerships could prove particularly essential in countries with significant budget deficits and dire infrastructure needs, such as the US.

1 Source: OECD; IHS Global Insight; GWI; IEA; McKinsey Global Institute analysis; Oxford Economics

2 Source: American Society of Civil Engineers

3 Source: US Debt Clock.org

4 Source: Congressional Budget Office

5 Source: Congressional Budget Office

6 Source: Aena

7 Source: The Port Authority of New York & New Jersey

This two-part series examines the expanding capital requirements for infrastructure globally as developed markets confront ongoing replacement needs, and the urbanization of emerging markets place additional stress on the existing foundation. This first part looks at sources of funding, and the second part will explore what this macro trend may mean for investors.

Important information

Investment in infrastructure-related companies may be subject to high interest costs in connection with capital construction programs, costs associated with environmental and other regulations, the effects of economic slowdown and surplus capacity, the effects of energy conservation policies, governmental regulation and other factors.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2015 Invesco Ltd. All rights reserved.

Bridging the gap in global infrastructure funding by Invesco Blog