A Look at Reported Results, and Subsequent Price Performance

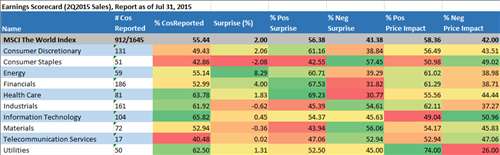

With slightly more than half of the constituents in the MSCI World Index having reported 2Q results, we thought it would be useful to take a look at the trend in sales and earnings so far. In the developed world, about 54% of those companies that have reported sales results have surprised positively, led by the Health Care and Financials sectors. The most negative sales surprises have been concentrated in the Consumer Staples, Materials, and Industrials sectors. On the bright side, just over 40% of Consumer Staples companies have reported as of July 31st– so there is room for improvement in the group.

MSCI The World Index (Sales)

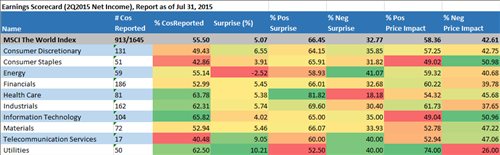

With respect to earnings, Health Care is by far the dominant sector with respect to positive surprises at just over 80%. The Energy sector has the dubious distinction of actual earnings results averaging about 2.5% less than expected earnings. Curiously, the Utilities sector has the lowest percentage of positive surprises (just over 50%), but the highest percent of companies experiencing a positive price impact.

MSCI The World Index (Earnings)

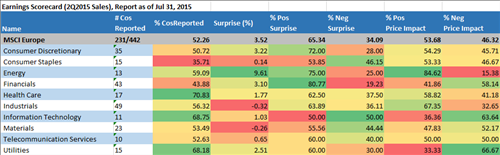

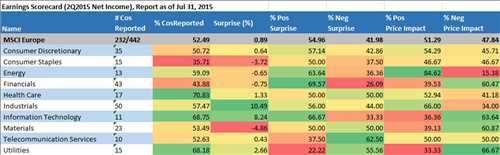

By region, other trends stand out. In MSCI Europe, Financials, Energy, and Consumer Discretionary companies have reported the most positive sales surprises so far. Information Technology (with nearly 70% of constituents having published results) lags every other sector with respect to positive surprises, which has resulted in a negative price impact in more than 60% of those companies.

MSCI Europe (Sales)

Reported earnings results in European Information Technology companies are significantly more positive, coming in second overall (just behind Financials) with about two-thirds surprising on the upside. This may or may not be a good example of companies’ ability to manipulate earnings results– a factor that plays a role in our preference for relying on valuation measures such as P/CF instead of P/E. But I digress…

MSCI Europe (Earnings)

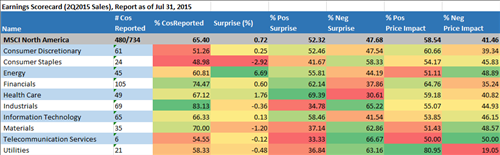

Turning now to MSCI North America, we find the most positive sales results surprises in the Health Care, Financials, and Information Technology sectors. We see that the 81% positive price impact in the Utilities sector here plays a large role in the similar observation in the MSCI World average results. Does it seem odd to anyone else that, in an environment of poor sales results and rising interest rates, four in five Utilities companies have seen positive trends in price?

MSCI North America (Sales)

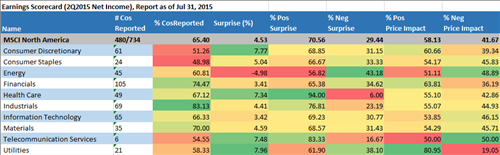

Heath Care stands out, once again, with nearly 100% of reporting companies beating expected earnings results. Even the Energy sector has more than 50% of its constituents generating positive surprises.

MSCI North America (Earnings)

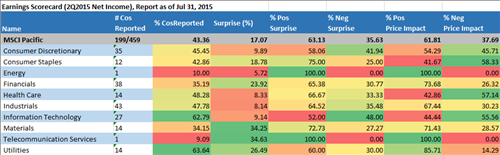

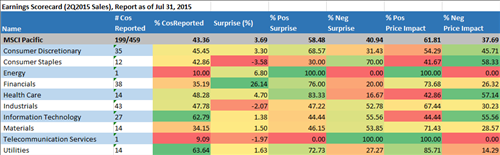

In MSCI Pacific, we note first that the overall percentage of companies that have reported 2Q results is just over 40%– significantly lower than in the other regions. Here, we note again the large positive price impact for Utilities companies but, in this case, actual sales results have been more positive than expected in more the 72% of those companies that have reported so far. The only other sector with more than 60% of companies reporting, Information Technology, has generated mostly (56%) negative surprises– leading to a primarily negative impact on price performance in those companies.

MSCI Pacific (Sales)

Sectoral trends in earnings are (so far) very similar to those for reported sales, a picture that could change as more companies report second quarter results. One interesting feature to note: the large dispersion in percentages by which companies have surprised. Ranging from 5% to nearly 35%, the magnitude of surprises has been significantly higher in MSCI Pacific earnings results than in any other region and does not appear to be related to the higher variation in the percentage of companies that have reported versus those that have not yet done so.

MSCI Pacific (Earnings)