The U.S. Dollar Index has recovered about half the losses from a two-month, -7% setback from the 12-year peak it established in March. We expect continued dollar strength over the next year as monetary policies in the rest of the developed world remain even looser than in the United States.

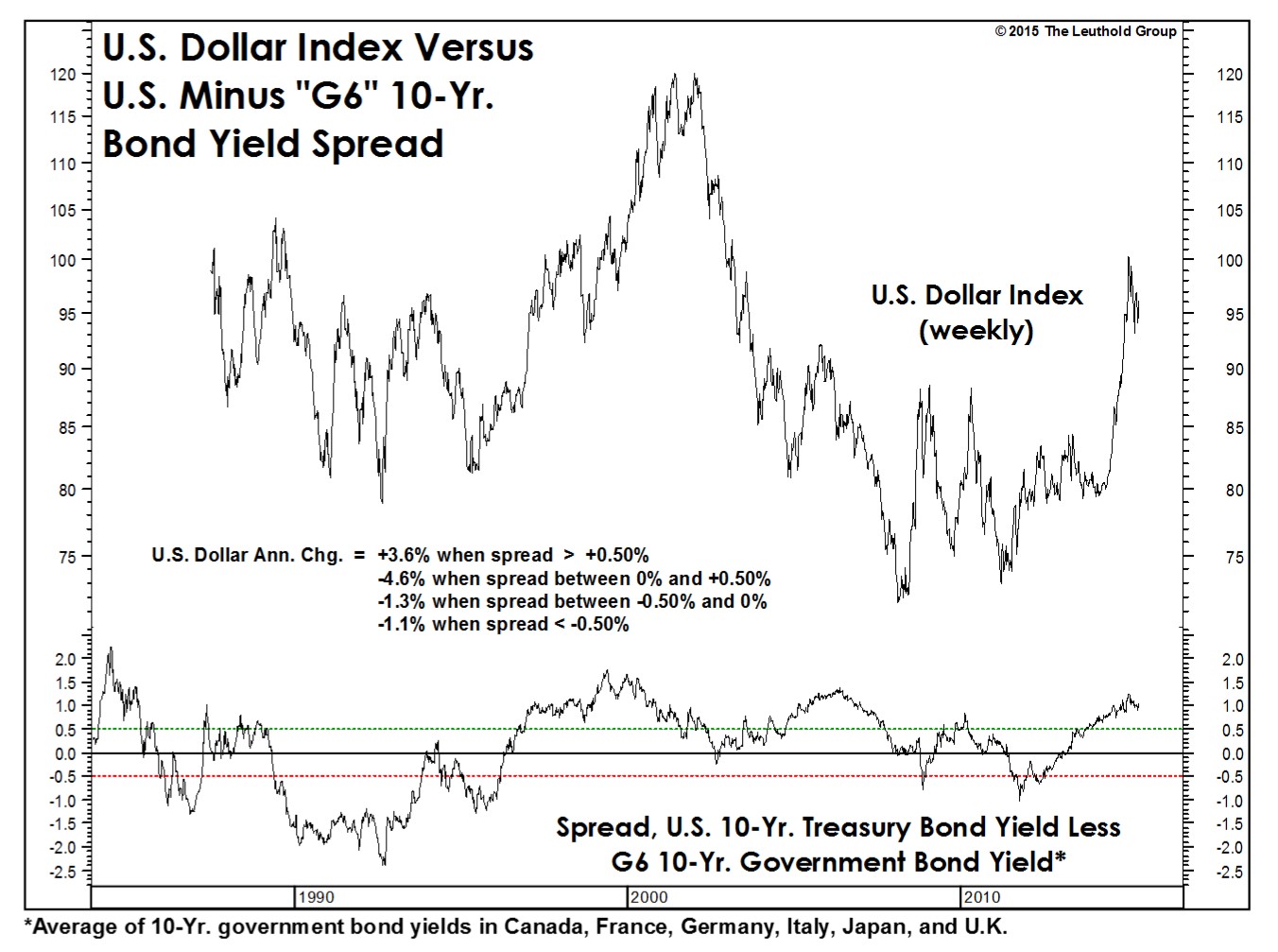

Currencies are especially difficult to model fundamentally. Purchasing Power Parity (PPP) seems to work in the extremely long run (20-30 years), but statistically is almost irrelevant on a cyclical (i.e., three– to five-year) basis. And the important cyclical drivers of currency moves vary from cycle to cycle, if not from month to month. Relative economic growth rates might drive currency moves for months on end, until there’s an overnight shift to some other “focus variable” like comparative deficit trends or interest rate spreads. And it’s the latter measure—specifically, the spread between U.S. and foreign government bond yields—that seems the key driver of today’s currency moves. Today’s 10-year U.S. Treasury yield of 2.30% is a full percentage above the G6 average. Historically, the critical threshold has been a yield spread of +0.50% or greater: since 1987, the U.S. Dollar Index has appreciated at an annualized rate of +3.6% under this condition (Chart 1). Again, though, we’d emphasize that such fundamental relationships are unstable across most asset markets and especially across the forex markets.

No discussion of the dollar would be complete without mention of its mysteriously strong (and inverse) relationship with the price of crude since early last decade (Chart 2). The fact that most of the world’s crude is priced in dollars makes the relationship an intuitive one, but in practice there was little correlation between the two series prior to 2002. In any event, the chart suggests that a new dollar up-leg could send crude to a retest of its March lows (a reason we suggest waiting for a VLT BUY signal to confirm that a solid bottom in crude has been established).