Storm clouds seem to build by the day. Many investors have an ongoing love affair with a few large-cap and more futuristic companies, yet they have corrected the prices of any stock with disappointing earnings or an attachment to the production of commodities.

Faith in U.S. economic growth is muted by five years of 2% or lower GDP growth, while highly-regarded strategists, who perpetuate belief in economic stagnation or Malthusian theories, rule the thinking of most investors. In short, the wind and the clouds seem pretty obvious.

As long-duration common stock pickers, we are reminded of King Solomon, who as a teenage king prayed for the wisdom to lead his people. His astute observations on life offer much to the patient investor. In Ecclesiastes 11:4, he wrote:

He who observes the wind will not sow,

And he who regards the clouds will not reap.

When Solomon was alive, wealth was accumulated through owning and raising livestock, farming and by conquering other groups of people. The wind and clouds affected all three of these wealth building activities.

At the market's close on July 27th of 2015, the S&P 500 Index was nearly flat from the beginning of 2014. Stocks have had a hard time getting out of their own way all year and individual/institutional investors have grown skittish along the way. International markets and economies like China are facing an economic slowdown and have sent an ill wind at U.S. multi-national companies.

We think the long-duration investor should take Solomon's advice. We must ignore the wind and sow the seeds of future success. The best way for us to think about this is to think of the absolutely worst wind storms that the stock market has provided in my 35 years in the investment business.

The first was the stock market crash of 1987. The S&P 500 Index peaked in August of 1987 at a little over 340 and bottomed in October at just over 200. The Index peaked again in March of 2000 at over 1600. If you observed the wind in August of 1987, you missed a gain of 370% plus dividends in 13 years.

In October of 2007, the S&P 500 peaked at 1560 as the clouds of the residential real estate and mortgage debacle arose. It then declined to 676 on March the 9th of 2009.

Today, the S&P 500 stands around 2067 and has tripled in price without counting dividends.

As professional investors, our observations affirm Solomon’s wisdom. If economic forecasting, market timing or political leanings were a wind which would blow your seeds off course, it has cost you money over the decades. If popularity among stock groups touted for their momentum provided you clouds and pessimism somewhere along the way, you missed long-duration rewards in companies and industries which never gained that kind of favor.

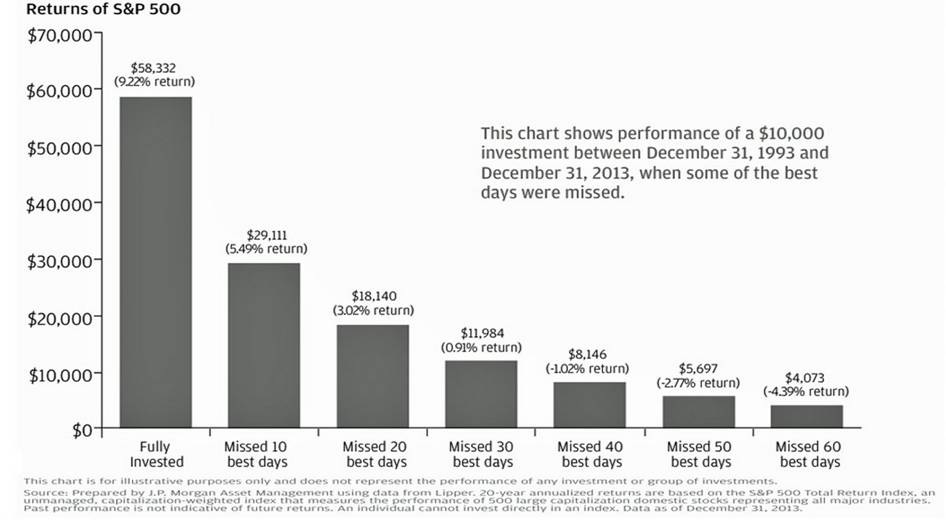

If you had the courage to sow and reap (staying fully invested), you could have grown your wealth overtime with the occasional attitude readjustment that a 40% or greater decline causes. The chart below helps you understand why.

Solomon knew that those who waited for a time with no wind and no clouds would likely never participate. They wouldn't place good seed investments in companies on sale with the kind of characteristics we look for via our eight criteria for stock selection nor would they reap the benefit of buying when clouds bring meritorious company share prices low.

When it comes to implementing the advice of the "Genius of Jerusalem," we turn to the "Oracle of Omaha," Warren Buffett. In 2011, CNBC’s Becky Quick asked if he had hired Todd Combs and Ted Weschler because they protected capital well in the financial crisis. In other words, had they avoided the ill winds and dark clouds of 2008? His answer was priceless: "I wouldn't have hired anyone who didn't get slaughtered in 2008." If today's wind and clouds cause a stock market decline, remember that those who avoid it will never have an entry point without them.

Warm Regards,

William Smead

The information contained in this missive represents SCM's opinions, and should not be construed as personalized or individualized investment advice. Past performance is no guarantee of future results. Bill Smead, CIO and CEO, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. A list of all recommendations made by Smead Capital Management within the past twelve month period is available upon request.

This Missive and others are available at www.smeadcap.com.