Weighing the Week Ahead: What is the Message of the Market?

As I have noted for the last two weeks, this earnings season carries a special significance. It provides an alternative to the official data on the economy. After a bad week for stocks, the punditry will be asking:

What is the message of the market?

Prior Theme Recap

In my last WTWA I predicted that attention to earnings reports would once again dominate the news. This was an accurate call. Earnings stories, both good and bad, were daily highlights. Our featured chart on dollar weakness as more important than geopolitics was especially accurate. More on earnings in the account of the week below.

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead. You can try it at home.

This Week’s Theme

Earnings season has developed a bipolar theme: Strength in some popular momentum names and weakness in stocks sensitive to the dollar. The market has provided a daily verdict on earnings reports. For many there is also an important economic message. Observers are asking:

What is the message of the market?

…and for some… Will the Fed be listening?

The Viewpoints

The earnings message draws several different viewpoints, including some noted last week.

- A weak economy has finally taken a toll on corporate profits, especially in some sectors.

- Stock market leadership has narrowed dramatically. Frank Zorilla illustrates with the chart below. He is open-minded about how this divergence could resolve, including a possible broad rally.

Stockbee has a very similar take on this important theme, including the potential for a rally.

- The strong dollar has hurt exports and profit margins of many large companies. It is showing up dramatically in energy stocks.

- Commodity price declines have accompanied the earnings reports, providing a negative feedback loop.

- Commodity prices remain strong on a long-term basis. The current economic risk is exaggerated. Scott Grannis has one of his helpful chart packs, including this “favorite indicator.”

As always, I have my own ideas in today’s conclusion. But first, let us do our regular update of the last week’s news and data. Readers, especially those new to this series, will benefit from reading the background information.

Last Week’s Data

Each week I break down events into good and bad. Often there is “ugly” and on rare occasion something really good. My working definition of “good” has two components:

- The news is market-friendly. Our personal policy preferences are not relevant for this test. And especially – no politics.

- It is better than expectations.

The Good

There was some good economic news.

- The Greek agreement held – at least for now.

- Earnings have been solid, measured by the “beat rate.” Bespoke has the story, noting the need to consider revenue and outlook as well.

- Leading indicators showed strong gains, 0.6% versus expectations of 0.2%. Steven Hansen at GEI has charts, comparisons to other measures and a full discussion.

- Existing home sales beat expectations. Bill McBride is not impressed, noting problems with the mix of sales and inventory. There is also less impact on the economy than new home sales. Good news, but perhaps not too significant.

- Initial jobless claims set an all-time low on a population-adjusted basis. NDD at the Bonddad Blog has the full story.

- Commercial real estate is strong. Scott Grannis analyzes the strength in prices, including this chart:

The Bad

There was also some negative data last week.

- LA port traffic was weak in June. (Calculated Risk).

- New home sales disappointed. Calculated Risk describes the miss in the annualized rate, but also notes year-over-year strength of 18.1%. Key question: Did mortgage rates affect the sales rate? It is too soon to tell.

- Revenues for Q2 have disappointed. Ed Yardeni notes the 4% decline including energy and the 1.5% increase without that sector.

- China Flash PMI declined to 48.2, a fifteen-month low. Combined with the decline in commodity prices, this further spooked related stocks. (China.org). This diffusion survey has a rather short life span and little demonstrated correlation to important outcomes, but it is getting a lot of attention. The world is hungry for data about the Chinese economy.

The Ugly

Louisiana shootings. These incidents are so disturbing and repetitive that I almost yearn for Congress to do something dumb to take its traditional position in this section.

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. Think of The Lone Ranger.

This week’s winner, Jimmy Atkinson at Dividend Reference, provides A Visual Guide to Useless (but Entertaining) Stock Market Indicators. Enjoy a good laugh, but there is an important conclusion. If you use data mining techniques to look at thousands of candidates, you will find some relationships. Poor methodology leads to indicators with no predictive value.

There are plenty of interesting charts, but those of us from the Chicago area will appreciate this one:

Quant Corner

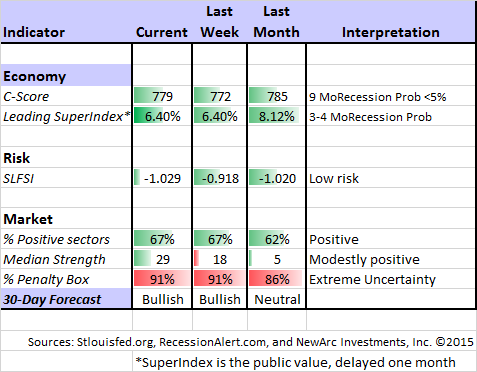

Whether a trader or an investor, you need to understand risk. I monitor many quantitative reports and highlight the best methods in this weekly update. For more information on each source, check here.

Recent Expert Commentary on Recession Odds and Market Trends

Bob Dieli does a monthly update (subscription required) after the employment report and also a monthly overview analysis. He follows many concurrent indicators to supplement our featured “C Score.”

RecessionAlert: A variety of strong quantitative indicators for both economic and market analysis. While we feature the recession analysis, Dwaine also has a number of interesting systems. These include approaches helpful in both economic and market timing. He has been very accurate in helping people to stay on the right side of the market.

Georg Vrba: An array of interesting systems. Check out his site for the full story. We especially like his unemployment rate recession indicator, confirming that there is no recession signal. He gets a similar result from the Business Cycle Indicator. Georg continues to develop new tools for market analysis and timing, including a combination of models to do gradual shifting to and from the S&P 500.

Doug Short: Provides an array of important economic updates including the best charts around. One of these is monitoring the ECRI’s business cycle analysis. Recently the ECRI finally admitted to the error in their forecast, but still claims the best overall record. This is simply not true. I rejected their approach in real time during 2011 and also highlighted competing methods that were stronger. Until we know what is inside the black box (I suspect excessive reliance on commodity prices and insistence on unrevised data) we will be unable to evaluate their approach. Doug is more sympathetic in his last update. While I disagree, it will require a longer post to elaborate.

ECRI now thinks that a near-term recession is unlikely, and Doug has the story.

Doug has regular updates of the “Big Four” economic indicators making up the NBER’s recession timing method. This week’s update includes revisions to industrial production, making the picture a bit worse.

The Week Ahead

It is a big week for economic data.

The “A List” includes the following:

- FOMC rate decision (W). No one expects a policy change, but the statement will get a lot of attention.

- Initial jobless claims (Th). The best concurrent news on employment trends, with emphasis on job losses.

- Michigan sentiment (F). Important concurrent indicator on spending and employment – some leading elements.

- Consumer confidence (T). Similar to Michigan sentiment. Showing recent strength.

The “B List” includes the following:

- Q2 Advance GDP estimate (Th). This may seem like “old news” and it will get revised.

- Durable goods (M). June data and volatile, but still important.

- Pending home sales (W). Less significant for construction and economic growth than new home sales.

- Crude oil inventories (W). Current interest in energy keeps this on the list of items to watch.

- Chicago PMI (F). Ranked highly in the analysis of indicators, and always significant when a weekend intervenes before the ISM index.

It is the quiet period for Fed speeches.

The earnings stories will command attention.

How to Use the Weekly Data Updates

In the WTWA series I try to share what I am thinking as I prepare for the coming week. I write each post as if I were speaking directly to one of my clients. Each client is different, so I have five different programs ranging from very conservative bond ladders to very aggressive trading programs. It is not a “one size fits all” approach.

To get the maximum benefit from my updates you need to have a self-assessment of your objectives. Are you most interested in preserving wealth? Or like most of us, do you still need to create wealth? How much risk is right for your temperament and circumstances?

My weekly insights often suggest a different course of action depending upon your objectives and time frames. They also accurately describe what I am doing in the programs I manage.

Insight for Traders

Felix has continued in bullish mode after more than a month in a neutral stance and the negative results last week. The confidence in this three-week forecast remains very low with the continuing extremely high percentage of sectors in the penalty box. Felix has shifted back to fully invested, including some foreign exposure. For more information, I have posted a further description — Meet Felix and Oscar. You can sign up for Felix’s weekly ratings updates via email to etf at newarc dot com. Felix appears almost every day at Scutify.

Tradeciety has another great post, aimed this time at “amateur” traders. There are four common questions and good answers. I especially like the discussion of stop losses and whether the market is rigged.

Brett Steenbarger has great advice for traders on avoiding promiscuity! Read it all, and learn to focus on the right type of trade. (This is pretty good advice for investors as well).

Insight for Investors

I review the themes here each week and refresh when needed. For investors, as we would expect, the key ideas may stay on the list longer than the updates for traders. Major market declines occur after business cycle peaks, sparked by severely declining earnings. Our methods are focused on limiting this risk. Start with our Tips for Individual Investors and follow the links.

We also have a page summarizing many of the current investor fears. If you read something scary, this is a good place to do some fact checking.

In Part Two of my series on risk I used the Chinese market as an example of headline risk. My main objective is to explain how to navigate the ever-threatening headlines. Along the way I share a few ideas of how you might profit from stocks with Chinese exposure.

Other Advice

Here is our collection of great investor advice for this week.

If I had to pick a single most important article, it would be this story of how a Harvard econ prof and retirement expert blundered on her own retirement account and what she did to recover.

Hints: Beware of tapping retirement funds for current spending. A few years of extra work can make all of the difference.

Investment Ideas

REITs. There are some interesting REIT ideas this week. We all know that there is risk from rising interest rates. Some sectors are growing rapidly enough that this risk might be offset. CNBC’s Diana Olick looks at some names in cloud computing, including what to look for. (I am using these and health care REITs as a bond alternative for some clients).

Offices are another idea, offering reward in some areas, but fraught with peril (ghost space) in others. Beware.

Real Estate. There are several ways of investing in real estate, ranging from direct purchase, to loans, to construction stocks. Bernice Napach at ThinkAdvisor covers the waterfront. Has the easy money been made already?

Personal Finance

Professional investors and traders have been making Abnormal Returns a daily stop for over ten years. The average investor should make time (even if not able to read every day as I do) for a weekly trip on Wednesday. Tadas always has first-rate links for investors in this special edition. As always, there are several great links, like this one about why it is great to be a young investor. I especially liked this great post (yet another) from Ben Carlson. I am not a fan of buy-and-hold, preferring attention to risk in adjusting size, but the article provides a good understanding of the fundamental approach.

If you sold your stocks the Friday before Lehman went bankrupt, went to cash & stayed there you would have missed out on a gain of 93%

He also quotes Jason Zweig as follows:

In 2009, when no one, I repeat NO ONE, was predicting that stocks would end up at the levels they’re at today, Jason Zweig talked about the paradox of buy and hold at a time when many had completely given up on it.

You can check out the quote, but it is not completely accurate. I am not getting much recognition for my 2010 Dow 20K call.

Junk Bonds

Watch out! That is the warning from Jeff Gundlach and Carl Icahn. Josh Brown reports the story and agrees.

Gold

Kid Dynamite warns about using charts to determine value in the yellow metal. He writes as follows:

the same people who are telling you that gold miners are cheap have been touting that story for at least the past four years, as the miners have gotten absolutely obliterated.

Energy Stocks

Morgan Stanley has a four-point checklist (via Bloomberg) suggesting the oil prices will stabilize and move higher. The biggest wild card is expanded supply from a reduction in Iran sanctions and improved conditions in Libya. It is an interesting, data-driven approach suggesting important points to follow.

Final Thought

As I have often observed in “the final thought”, the right answer may well be different for traders and for investors.

Felix’s trading approach reflects a market that is at the lower part of a long-term trading range and has several attractive sectors. Traders (including Felix) are very skeptical of economic data and use a lot of charts, trends, and theoretical points of support and resistance.

Investors have a different problem. Investors cannot make major position shifts in short time periods. Most who try to be agile wind up losing money through the market timing attempts.

Investors do better to focus on fundamentals – the economic cycle and corporate earnings. If there is no recession in prospect, the risk of a major decline (40-50%) is low. The risk of a 15-20% market correction is always present and essentially unpredictable.

The result is that investors are often on the other side of the market from traders. This week that means two things:

- Selling (or reducing size) in momentum stocks with exaggerated multiples.

- Buying (or increasing size) in downward momentum stocks that are oversold based upon the economy.

Put another way, the economic data are far more positive than the apparent message of the market. A strong approach to investing is to make your investment choices on fundamental grounds and take advantage of errors by “Mr. Market.”

A common investor error is to change course whenever the market seems to be going against you.

None of our indicators show major economic risk. Commodity prices have notoriously given false signals before, especially in 2011. Cullen Roche analyzes the question and draws a solid conclusion, consistent with the work we regularly cite:

More importantly, is the big outlier risk at this point still further upside in the economy as opposed to the next big crisis that everyone seems to be in search of on a daily basis? In other words, is our boom still in front of us before the next big bust? It’s looking like that just might be the case. Therefore, while we’re very likely entering the middle to later stages of this recovery the current 72 months relative to historical averages does not necessarily mean we’re at the end of the cycle.