Mid-Year Update: A Look at the High Yield Market

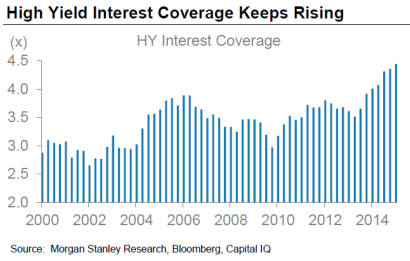

I have seen every cycle since 1985 and while this cycle which began in 2009 has not been without a few warts, it has also been very different and far more conservative than many of these prior cycles. The majority of issuance was and continues to be for refinancing activity. This lowers interest expense and improves credit metrics for companies. Case in point, as noted below, high yield interest coverage (cash flow, or earnings before interest taxes, depreciation and amortization divided by interest expense) has steadily improved and at the highest levels we have seen over the past 15 years.1

We are certainly not seeing over-extended companies in terms of their debt load or ability to service that debt, as we have often seen in historical high yield “bubbles.”

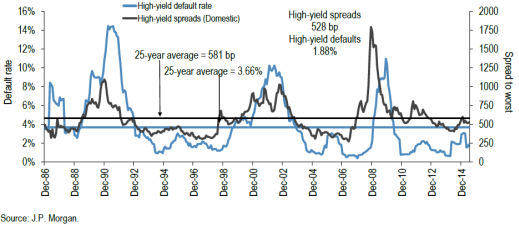

Valuation is of course hugely important as well. Valuation of high yield credit is all about spread levels. But it is much more than that because without risk adjusting spreads, a false dawn can be painted. Default rates play a very large role in the risk adjustment process and we believe default rates (outside of energy) will remain well below average. Spread (spread-to-worst) levels for the indexes are around historical averages, but default rates are expected to be about half of their long term averages (currently 1.9% versus a nearly 30-year history of 3.7%).2

![]()

While this is certainly positive, it is also not an accurate view of the market from where we sit. We are continuing to find plenty of names with spread levels well above this level, yet with what we see as excellent credit metrics. Why does this “extra” value exist today? Two words: liquidity premium. While all the focus on the lack of liquidity over the past few months is perceived as negative, we view it as a massive positive for those investors with a time horizon longer than a week. The notion of liquidity in all markets is deceiving. This goes not only for over the counter markets in bonds and loans, but for equities as well. When the environment turns ugly, how many market makers do you know that stick their necks out to ensure an orderly market? The correct answer is 0. While legislation has reduced the number of market makers and capital available to make markets in high yield, we have never viewed it differently; liquidity is a coward that disappears at the first shot. This liquidity premium is creating attractive investment opportunities for investors who are unconstrained by factors such as tranche size minimums or maturities that limit many of the larger, passive high yield funds.

Credit cycles end badly because of dramatically over-leveraged balance sheets (1990 and 2007) and/or the funding of dubious business models with lots of leverage (1998-2000—Telecom, Media, and Technology, TMT). While broadly speaking within the high yield market we are seeing reasonable value and conservative balance sheets, we have been vocal and adamant that many shale oil and gas producers fit this second broken model with their unsustainable business models and we continue to avoid them, and caution other investors to do the same. Market participants today have ring-fenced this industry and we believe an increase in defaults for this specific industry is unlikely to lead to a blowout in the overall credit market, particularly given where interest rates reside. We believe that those avoiding the entire high yield market because of possible contagion from oil and gas should re-think that strategy.

The high yield bond and loan market has grown up into a large, mature asset class, now together totaling approximately $3.5 trillion3, and that investors can’t and shouldn’t ignore this asset class.

1 Richmond, Adam, Meghan Robson, and Jeff Fong, “Leveraged Finance Insights,” Morgan Stanley Research, June 15, 2015, p. 1.

2 Acciavatti, Peter D., Tony Linares, Nelson R. Jantzen, CFA, Rahul Sharma, and Chuanxin Li. “Credit Strategy Weekly Update.” J.P. Morgan, North American High Yield and Leveraged Loan Research. June 26, 2015, p. 5. Spread referenced is spread-to-worst.

3 Blau, Jonathan, James Esposito, and Amit Jain, “Leverage Finance Strategy Weekly,” Credit Suisse Fixed Income Research, July 17, 2015, p. 4, 26.

Although information and analysis contained herein has been obtained from sources Peritus I Asset Management, LLC believes to be reliable, its accuracy and completeness cannot be guaranteed. Information on this website is for informational purposes only. As with all investments, investing in high yield corporate bonds and loans and other fixed income, equity, and fund securities involves various risk and uncertainties, as well as the potential for loss. Past performance is not an indication or guarantee of future results.