Searching for Natural Hedges Against Interest-Rate Risk

In the United States, the fixed income story today is a cautionary tale of rising interest rates lurking around the corner. Most investors probably have heard this story for a while now, surmising that the end of the bond bull market will mean it is game over for their fixed income portfolios. Franklin Templeton’s Eric Takaha doesn’t see that as a foregone conclusion, but also believes plotting a fixed income strategy to meet tomorrow’s challenges requires a willingness to think about investing in the sector a little differently, perhaps looking beyond traditional borders, benchmarks and duration models, and seeking out strategies that have the potential to provide what could be considered a natural hedge against interest-rate risk.

Diversifying Beyond Core Fixed Income

Do rising US interest rates mean investing in bonds or bond funds is destined to become a losing proposition? That the “bond bubble” that some say has been building for decades is set to burst? While we do not know the exact timing around future interest-rate moves, we think investors should consider managing their fixed income portfolios with a defensive posture—one that can not only potentially generate income, but also aims to position for the least-nausea-inducing ride. In our view, part and parcel of that approach should look beyond the US interest rate curve1, aiming to provide income generation and potential return across a broad range of fixed income markets globally.

We believe that in the decade ahead, the strategies that have relied on falling interest rates to generate returns could be challenged. For that reason, we think investors should think about diversifying beyond core fixed income in their portfolios—looking beyond the US rate curve to provide potential income and return across a broad range of global fixed income markets—but also be keenly focused on building and evolving a dynamic risk-management strategy.

Finding the “True Risk” in a Portfolio: An Inexact Science

We believe there is growing recognition among the investment community that risk is a primary lever in the investment process. While effective modeling is built on a foundation of transparency, no single measure—including the concepts discussed here—will provide a complete picture of the “true” risk inherent in any individual investment or portfolio. Risk professionals must look at a wide variety of data points from a host of sources and risk measures.

When discussing interest-rate risk, the conversation often turns to duration. An examination of duration (see sidebar), which takes into account bond maturity, coupon and call features, can offer a mechanism to help manage the risk—and the volatility—in fixed income investments that accompany interest-rate movements. For example, maintaining a shorter duration in a portfolio tends to result in lower interest-rate-related volatility.

We view traditional core and passive fixed income strategies with concentrated duration exposure as likely ill-suited to succeed in coming years. In our view, a truly unconstrained strategy has more flexibility to potentially navigate and exploit varying market conditions and diversify the drivers of return in a portfolio. This result becomes more apparent when compared with relatively duration-heavy core fixed income portfolios, particularly in a rising-rate environment.

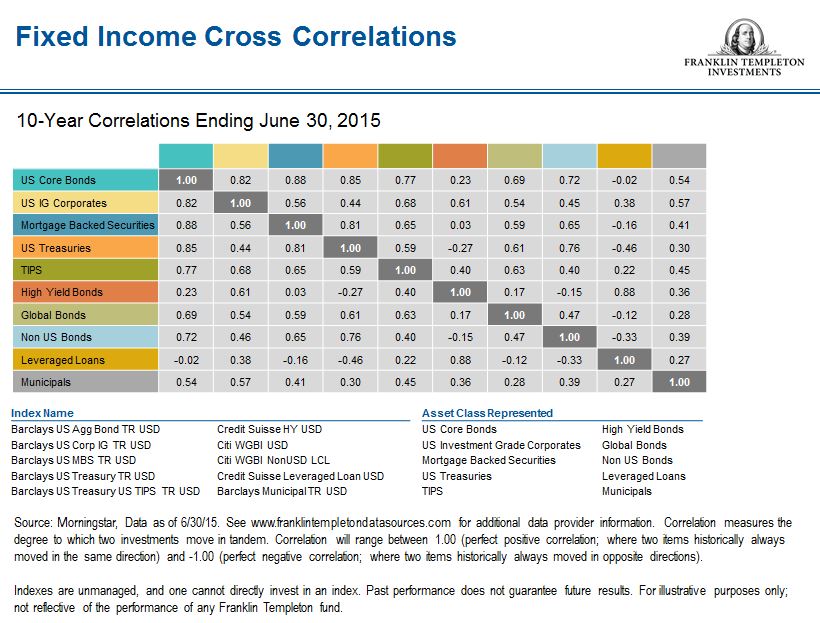

Various fixed income indexes and US Treasuries have experienced relatively strong correlations (see table below), indicating that duration has been the predominant risk, and yield movements have been the primary driver of returns. Conversely, a strategy with relatively low correlation—and even a negative correlation—to US Treasuries could be a more efficient allocation to fixed income. The table below shows how cross correlations across the fixed income market can potentially enhance diversification—without guaranteeing of profits or protection against risk of loss—in an unconstrained portfolio that has the ability to exploit these different sectors.

Duration and Risk: Thinking Empirically

While interest-rate movements drive a meaningful portion of fixed income returns, there are other factors, including credit spreads and currency movements, among others, that also drive returns.

If a rise in interest rates is anticipated, maintaining a low or negative duration might be considered to seek to avoid potential portfolio losses due to a drop in bond values. Negative duration may seem highly desirable in a rising-rate environment, but it can result in undesirable levels of volatility and risk. And, while the value of a portfolio with negative duration might increase when rates rise, there is the possibility rates may remain steady or even fall, resulting in potential loss. Our goal is to have a complete understanding of the interest-rate risk in our portfolio and position based on our views across a variety of markets and sectors. To review a portfolio’s sensitivity to interest-rate risk, we believe an examination of empirical duration—calculating duration based on historical data over a specified time period—is a worthwhile exercise.

We cannot completely remove the risk elements, but we can try to influence the interest-rate experience of a portfolio. Our approach to risk management is three-pronged: It involves recognizing the risks we are taking, making sure they are rational, and determining that there is appropriate reward potential.

In a portfolio comprising highly duration-sensitive assets, yield curve movements will dominate performance. However, there are other potential drivers of performance in a flexible, unconstrained fixed income portfolio—such as Franklin Strategic Income Fund—including various spread sector and global exposures. By expanding into these sectors, we aim to reduce the reliance on interest rates as a driver of performance. The primary performance drivers in our strategy are sector allocations and rotation decisions, along with security selection within those sectors. So, we examine empirical duration not necessarily as a primary performance driver, but as part of our overall risk-management toolkit.

Certain bonds have pricing that tends to be impacted more significantly by factors other than changes in interest rates, such as economic growth, corporate earnings patterns and temporary market shocks. This is particularly true for more credit-oriented sectors. Rising interest rates tend to accompany healthy economic growth, and when growth is healthy in an economy, corporate assets are generally supported.

Putting It into Practice

So what does this all mean in terms of portfolio positioning? Our goal for Franklin Strategic Income Fund is to build a well-diversified portfolio that has a variety of performance drivers beyond interest-rate movements; Franklin Strategic Income Fund invests at least 65% of its assets in US and foreign debt securities.

From a portfolio-duration-positioning standpoint, incorporating a view of empirical duration alongside model-based durations (such as Option Adjusted Duration) can help provide a more complete picture. Additionally, as mentioned, our unconstrained approach allows us to look across a broad range of credit markets globally for potential income and return, regardless of interest-rate movements in one particular market.

While many US investors seem to be so singularly focused on the impact of rising rates—to the point of panic in some cases—they fail to examine what has actually happened to various fixed income investments over similar periods historically. We have found that historically over time, interest-rate moves do not often play as large of a role in a broadly diversified fixed income portfolio as one might think.

The impact of rising rates on a fixed income portfolio (for better or worse) ultimately depends on what asset classes and market segments one is invested in. It is also worth pointing out the importance of the “income” component within fixed income—the primary attraction for many investors to the asset class—that we think can be achieved using myriad tools and market exposures. We believe what it takes is a broad view of the sectors that comes from a truly unconstrained approach. And, we think it requires a thoughtful examination of the risks, one that looks at risk modeling through a variety of different lenses.

Eric Takaha’s comments, opinions and analyses are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

What Are the Risks?

Franklin Strategic Income Fund

All investments involve risks, including possible loss of principal. Bond prices generally move in the opposite direction of interest rates. Thus, as the prices of bonds in the fund adjust to a rise in interest rates, the fund’s share price may decline. Changes in the financial strength of a bond issuer or in a bond’s credit rating may affect its value. High yields reflect the higher credit risks associated with certain lower-rated securities held in the portfolio. Floating-rate loans and high-yield corporate bonds are rated below investment grade and are subject to greater risk of default, which could result in a loss of principal—a risk that may be heightened in a slowing economy. The risks of foreign securities include currency fluctuations and political uncertainty. Investments in developing markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and less liquidity. Investing in derivative securities and the use of foreign currency techniques involve special risks and, as such, may not achieve the anticipated benefits and/or may result in losses to the fund. These and other risk considerations are discussed in the fund’s prospectus.

Investors should carefully consider a fund’s investment goals, risks, charges and expenses before investing. To obtain a summary prospectus and/or prospectus, which contains this and other information, talk to your financial advisor, call us at (800) DIAL BEN/342-5236, or visit franklintempleton.com. Please carefully read a prospectus before you invest or send money.

1 An interest rate curve is a graphical representation of interest rates at a set point in time of bonds having equal credit quality but differing maturity dates, such as US Treasury securities. It is generally seen as a benchmark for market interest rates.

© Franklin Templeton Investments

© Franklin Templeton Investments