US Equity and Economic Review For the Week of July 13-17; Earnings Season Begins, Edition

The Federal Reserve issued two important documents last week: the Beige Book and Chairperson Yellen’s latest Congressional testimony. The Beige Book was largely positive. Non-financial service growth is moderate. Real estate is growing and the employment picture was generally positive. Strong demand for autos sales helped increase consumer spending. The only negative was manufacturing which was uneven due to the strong dollar and weak energy sector. For an excellent summary of the overall macro environment, see this post from Fat Pitch, which has an incredible depth of information. Also see this post from my co-blogger NDD on the long leading indicators, where he concludes, “While not every long leading indicator is making new highs, and in particular corporate profits have stalled, the other indicators solidly suggest that this economic expansion will last at least through the 2nd quarter of 2016.”

Janet Yellen gave her regular Humphrey Hawkins testimony before Congress, which contained several important passages, beginning with the potential impact of foreign economic developments on the US economy:

As always, however, there are some uncertainties in the economic outlook. Foreign developments, in particular, pose some risks to U.S. growth. Most notably, although the recovery in the euro area appears to have gained a firmer footing, the situation in Greece remains difficult. And China continues to grapple with the challenges posed by high debt, weak property markets, and volatile financial conditions. But economic growth abroad could also pick up more quickly than observers generally anticipate, providing additional support for U.S. economic activity. The U.S. economy also might snap back more quickly as the transitory influences holding down first-half growth fade and the boost to consumer spending from low oil prices shows through more definitively.

China is already impacting the world economy. Countries that benefitted from the “south-south” trade, (where raw materials were exported to China’s manufacturing base) are experiencing slower growth. And the recent Shanghai sell-off bled through to other Asian equity markets. While the EU started the year out well, it’s hard to see the Greek situation not having at least a short-term negative impact. These events have already impacted the US by giving the dollar has a strong bid:

Over the last few months, the ISM manufacturing report’s anecdotal commentaries have noted the strong dollar is negatively impacting exports. Should these event’s severity increase, it’s possible we’ll start to see a more profound impact.

Next, she made this observation about interest rates:

A decision by the Committee to raise its target range for the federal funds rate will signal how much progress the economy has made in healing from the trauma of the financial crisis. That said, the importance of the initial step to raise the federal funds rate target should not be overemphasized. What matters for financial conditions and the broader economy is the entire expected path of interest rates, not any particular move, including the initial increase, in the federal funds rate.

This is a key point: when the Fed raises rates for the first time, they will be signaling to the market that the normalization process has begun. But, this path will take some time. This part of the message was lost on the press and market observers.

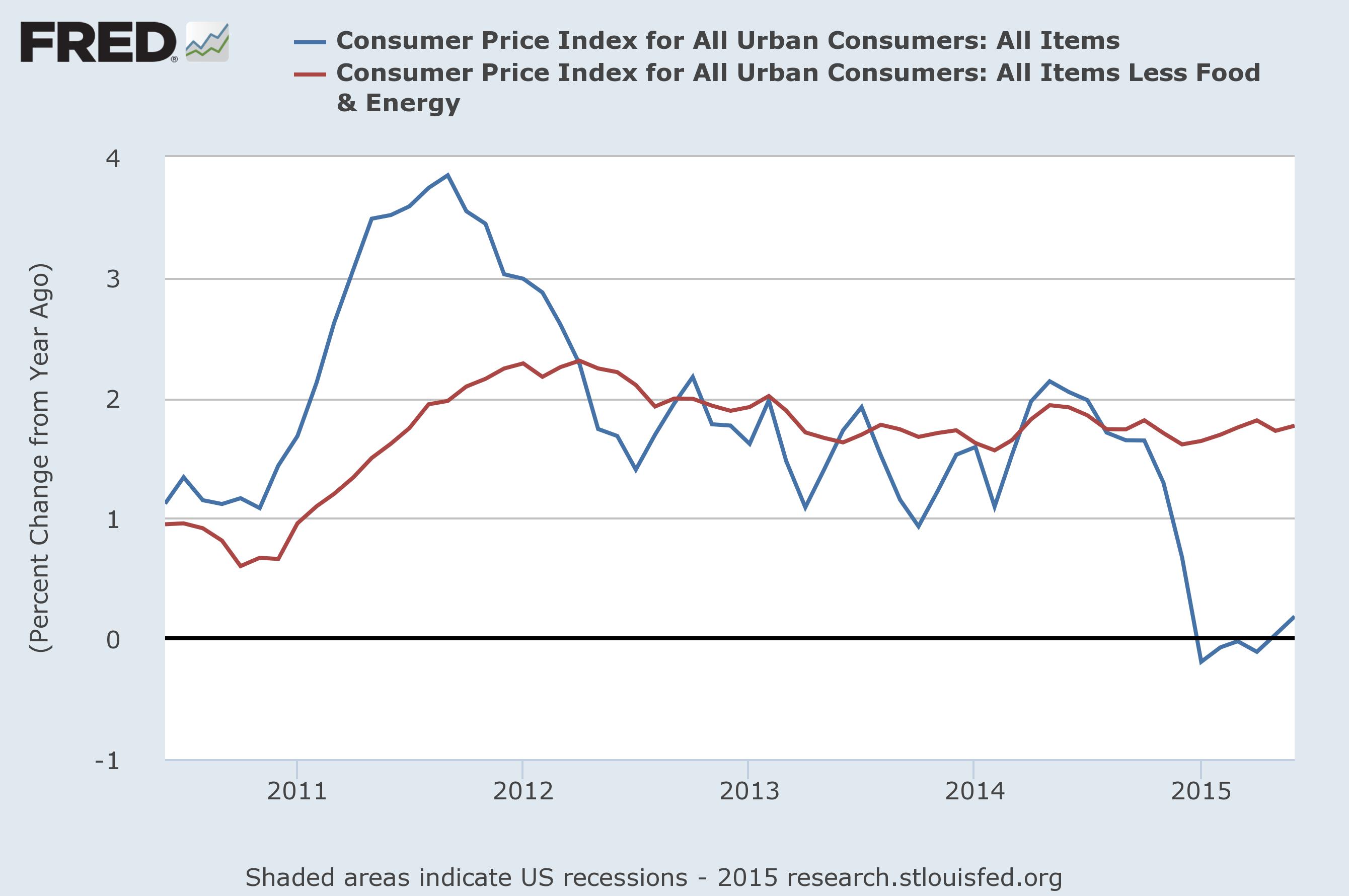

Inflation is still low. From the BLS: “The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.3 percent in June on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index rose 0.1 percentbefore seasonal adjustment.” This chart shows that while core costs are stronger than total inflation, prices are still very much under control:

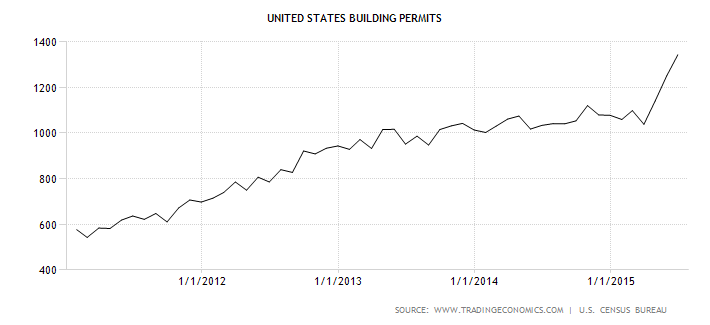

Building permits printed another strong number, indicating the housing rebound is gaining steam. The total number of permits issued for the last three months was revised higher. More importantly, this report’s recent numbers have sent this indicator into stronger territory:

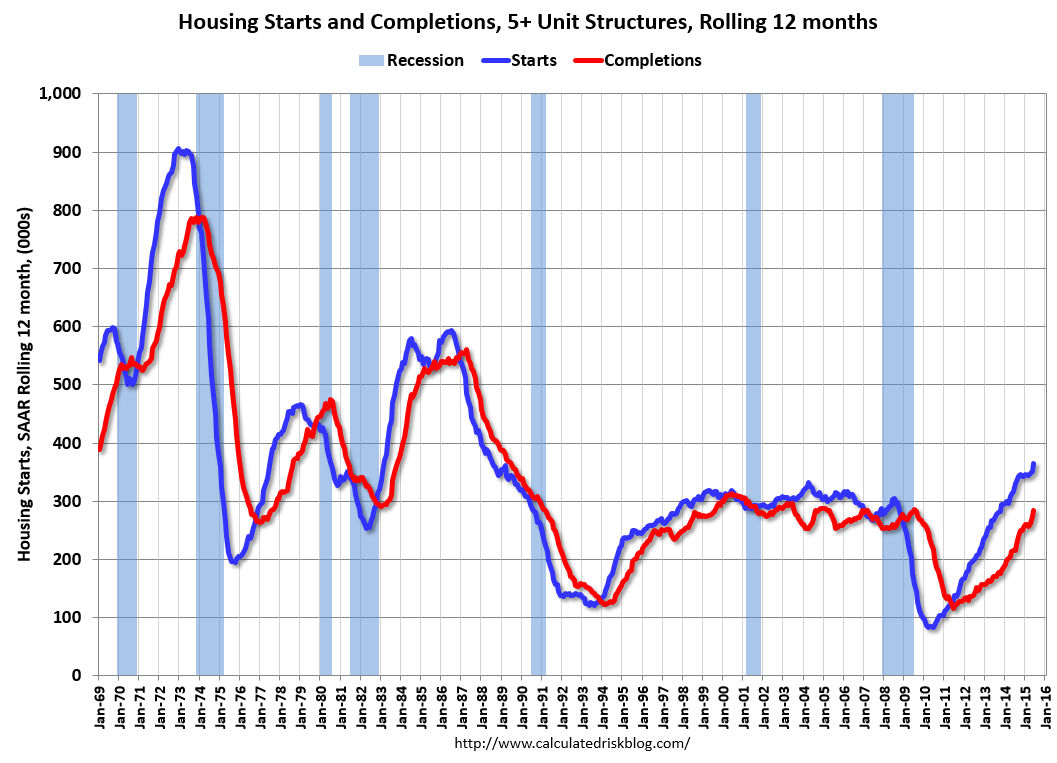

Also consider this chart of total starts and completions from Calculated Risk:

Starts cratered after the recession, lowering supply. Starts (the blue line) are playing catch-up with the market, which explains why it is now above the 300,000 level. Over the last few months, housing sector numbers have been very positive and encouraging for the economy as a whole.

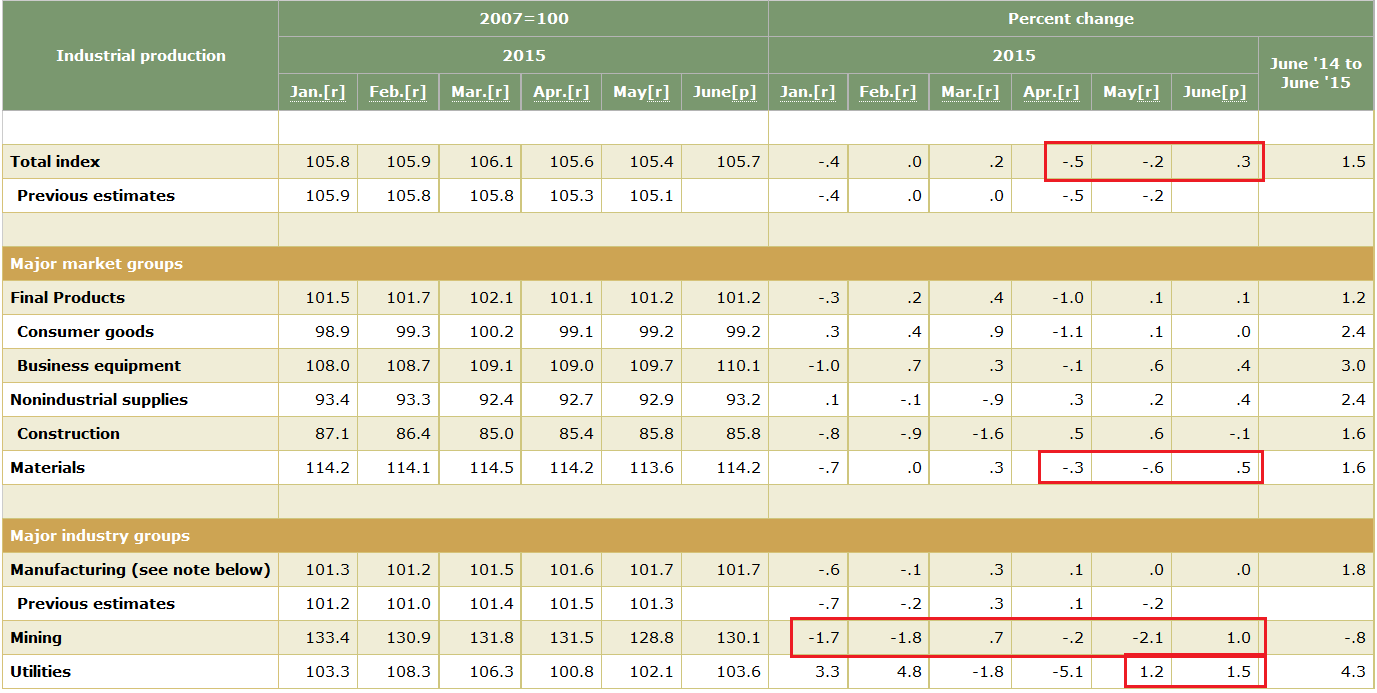

Industrial production – which has been in a slight downward trend for the last five months – increased .3% last month. The biggest surprise in the report was the 1% increase in “mining:”

As oil dropped at the beginning of this week due to the Iran deal, it’s doubtful we’ll see a continuation of this trend.

Retail sales decreased .3% M/M. As this chart from the FRED system shows, retail sales are also lower Y/Y since the start of the year:

The weakness in the latest report is broad-based: auto sales, building materials, clothing and general merchandise are all lower. This is a bit surprising, especially since oil’s price drop has increased consumer buying power. But it is consistent with the increased personal savings rate we’ve seen from consumers since the end of the recession:

Remember the US consumer has spent the better part of this recovery de-leveraging, meaning he’s allocating at least some of his income to debt payments. On the good side, this means he is in far better financial shape than before the recession. On the bad side, it also means he is spending less which detracts from overall growth.

Finally, we have the Atlanta Fed’s GDP now graph, which is predicting 2Q growth a little below 2%:

Conclusion

The moderate growth of this expansion continues. The Beige Book reported moderate growth over a majority of sub-sectors. While industrial production increased last month, oil’s price drop and the strong dollar will provide meaningful headwinds for at least the next few months. The US consumer continues to spend modestly to continue strengthening his financial position. There has also been a sea-change in his overall behavior: lower spending with a larger focus on this financial position. Finally, the Atlanta Fed’s GDP now points to continued 2Q growth.

Market Analysis

The market remains expensive: the current and forward PEs for the SPYs and QQQs are 21.24/23.39 and 17.87/19.56, respectively. And as we enter another earnings season, overall corporate earnings are weak:

According to Standard & Poor's, S&P 500 revenues fell 2.3% y/y during Q1 mostly as a result of the plunge in the revenues of the Energy Sector, and also the strength of the dollar. On a same company basis for both periods, we calculate that S&P 500 revenues fell 3.0% y/y during Q1, but rose 2.4% excluding the Energy sector. A similar pattern is likely for Q2. Industry analysts currently estimate a 4.0% decline in revenues during the quarter, but a small gain of 1.5% excluding Energy.

At a time when traders desperately need to see a consistent stream of stand-out revenue numbers, it’s highly unlikely they’ll see any.

Due to the weak earnings environment, I remain slightly bearish. Several market undercurrents support the bulls, however. First, the QQQs broke to new highs last week:

Prices moved strongly through the 110-111 price level. Momentum is positive and prices are strengthening. And the number of stocks about the 200 day EMA is a little above 50%, meaning there is plenty of room to move higher.

But, there are troubling signs from other parts of the market, starting with the Transports:

Prices hit 166.55 in November. They trended sideways until the end of March. They’ve printed a series of lower lows and lower highs since. This is especially troubling with oil’s price weakness. With one of the largest input costs massively over-supplied and a major producer (Iran) coming back into the market, transports should be rallying strongly. For a contrary opinion, see this post from Greg Harmon at Dragonfly Capital.

And the Russell 2000 (IWMs) aren’t confirming the new high:

Prices hit the 126 level and stalled. It would have been far better if they moved through this level and then at least hit resistance at 128. As of now, this index is facing resistance from two levels.

The SPYs had a similar technical issue last week:

After hitting the 122 level, prices stalled. Also note the weakness of the candles, especially in comparison to the QQQs.

The QQQs made their move last week, so it’s possible this move higher was the first step that will be followed by the IWMS or the SPYs. There is also plenty of upside room as a large number of stocks are trading below their respective 200 day EMAs. But the negative situation in the transports is very concerning. Prices are down 11% after hitting the 166 level. And this is when oil is cheap. This fact highlights how troubling the transports situation is. It’s very difficult to see a concerted move higher when this index is in a correction.