SUMMARY

- Since the end of the financial crisis, fixed-income investors have experienced higher liquidity costs and greater market price volatility – a trend that is likely to continue. This is largely a direct result of post crisis financial reform – actions taken by central bankers and regulators that transferred risk from the banking system to investors in the capital markets.

- Financial reform has caused a decline in dealer market making and has reduced the “grease” in the system: The spreads between bids and offers in the market have widened, which represents a repricing of liquidity.

- Fixed-income markets have demonstrated their resilience following significant post crisis sell-offs. End market demand – not inventories of securities held by dealers – has been the principal source of liquidity that helped market prices bounce back.

"Liquidity" takes center stage

The biggest story in financial news reports today about the bond market is “liquidity,” which we believe may be one of the most misunderstood topics for fixed-income investors. Many investors and market commentators worry about a coming liquidity crisis without fully understanding what that would mean. Fixed-income investors have already begun to experience higher liquidity costs and market price volatility. The silver lining is that they may be better conditioned for the environment ahead.

Higher liquidity costs have often been accompanied or followed by market price declines, but the two are independent concepts. Understanding the distinction can help investors stay the course and be better positioned to meet their investment objectives. From our perspective, as long as there is a buyer and a seller for a given security, it is liquid. A separate, important question is the price of that liquidity – most commonly expressed as the spread between the bid and the offer. Spreads can widen in sectors or securities for any number of technical or fundamental factors, and such widening increases liquidity’s cost. But that should not be confused with illiquidity, which has been a very rare, transient occurrence in major U.S. capital markets.

In this quarter’s report, we examine some of the causes of recent increased liquidity costs and what it may mean for investors.

The dark side of financial reform

Traditionally, the willingness of dealers to make markets by holding inventories of fixed-income securities provided investors with a source of initial liquidity. However, since the crisis, reforms such as the Dodd-Frank Act and the Volcker Rule have compelled dealers to reduce leverage and increase capital, which has made holding those inventories more expensive. This has led to a significant reduction in bond dealer inventories (which were never very large relative to the size of the markets), pegged by the SEC as a drop of more than 75% since the precrisis period. In addition, over the past 10 years, there has also been marked growth in credit sectors like investment-grade corporates and high yield – outstandings have increased by 169% and 100%, respectively. Much of that growth has come in the retail sector through mutual funds and ETFs.

The combination of diminished dealer inventories, increased bond volume and greater retail ownership has prompted concern from a number of observers, including Fed Chair Janet Yellen, who noted the potential for this to exacerbate a market sell-off once rates begin to rise. The bottom line is that regulators effectively acknowledge that risk has been shifting from the banking system to capital market investors. This move appears to have put the banking system on a sounder footing, but also has led to the repricing of liquidity and higher market price volatility in fixed-income markets.

Liquidity is a relative concept

The price of liquidity for a specific holding is dynamic – that is, it adjusts based on the market environment and changes over time. A related concept, developed by Interactive Data Corp. (IDC), provides an interesting way to think about liquidity risk and market price volatility. IDC’s so-called liquidity ratio examines the market price impact per dollar traded of a specific security. The liquidity ratio is defined as the projected potential market price volatility divided by the projected potential trading volume. The larger the IDC liquidity ratio for a particular asset, the higher the price of liquidity and the greater the potential for market price volatility.

Lessons from the recent past: Market resilience has followed sell-offs

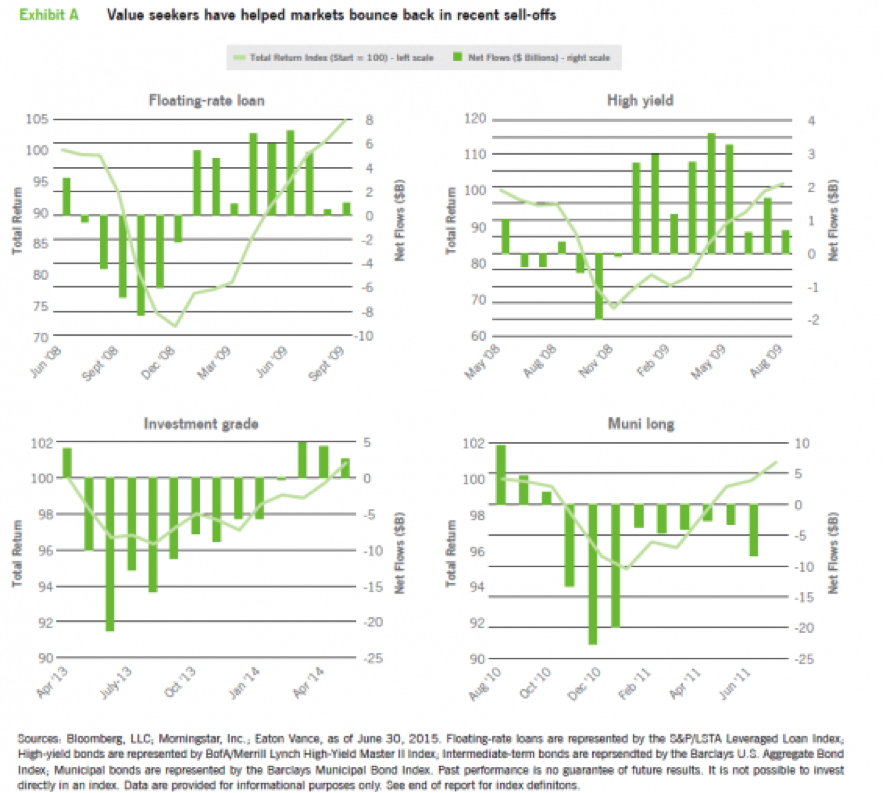

There is concern among many that rising interest rates (among other factors) could be the catalyst for a mass exodus of investors from fixed-income funds. Combined with current elevated liquidity costs, this could result in significant price declines in traditional fixed-income markets. What most investors don’t appreciate is that since the financial crisis, with the price of liquidity already rising, we have witnessed several large market price declines in specific fixed-income sectors. We believe these market downdrafts are highly instructive. Exhibit A shows how four sectors – floating-rate loans, high-yield, investment-grade and municipal bonds – fared before, during and after significant market sell-offs. In each graph, the blue line shows the cumulative total return of the given index, with the index set to 100 at the start of the period. (The price component of total return, excluding income, isn’t shown, but price movements during such episodes represent the overwhelming driver of total return.) The bars show the net flows from retail fund investors, as tracked by Morningstar.

Floating-rate loans and high yield. In the case of floating-rate loans and high yield, the period starts with the 2008 financial crisis. The historical declines in both markets were precipitated by fears of a significant erosion of credit quality stemming from the crisis. During the sell-offs, it became clear quickly to investors that dealers were unwilling to keep making markets using their balance sheets, and that liquidity would need to come from other buy-side investors (e.g., hedge funds and institutional investors). With the aid of some emergency action, buy-side investors did step in, and within a year from the trough in prices, both markets regained all lost ground. Market participants understood that elevated liquidity costs and higher market volatility created unique buying opportunities for assets whose intrinsic values were well above their current market prices.

Municipal. The muni episode was sparked by bearish comments from Meredith Whitney, then a prominent municipal bond analyst, who issued a report in September 2010 that there would be hundreds of billions of dollars of defaults in U.S. municipal bonds within a year. The long end of the municipal bond yield curve sold off significantly in the second half of 2010, as liquidity costs jumped and retail investors in long-duration muni bond funds headed to the exits. Again, dealers may have been willing to use their balance sheets briefly to support the market, but this was very short-lived. Dealers were in business to generate a return on their capital investment, not to provide a backstop for investors. Rather, when market prices swooned to levels well below their intrinsic values, crossover buyers – those who typically invest in taxable bonds – provided liquidity to municipal bond investors. Ms. Whitney’s gloomy forecast never panned out and the market regained all of its lost ground within a year.

Investment grade. Many believe the next sell-off in fixed income will not come from deteriorating credit, but from rising interest rates. In this case, we can also look to recent precedent. The investment-grade bond market sold off materially in June 2013 due to fears that the wind down of quantitative easing by the Fed would lead to rising interest rates – the so-called “taper tantrum.” At that time, liquidity costs were elevated, the 10-year U.S. Treasury note jumped approximately 1% and retail mutual fund flows were in net redemption. Other market participants, not dealers, came into the market, and once again the market fully rebounded.

Implications of a higher liquidity-cost environment

- Bond price movements typically reflect changing expectations about the market’s macro view as well as the fundamental outlook for specific investment sectors. In an elevated liquidity-cost environment (like today’s), prices are likely to adjust faster when investor sentiment changes.

- At some point, fears of rising rates or other factors may lead to significant net outflows in specific fixed-income sectors, and a corresponding rapid decline in prices. But, as we have seen, higher liquidity costs can also help markets rebound very quickly. The key is to recognize that prices are more likely to overshoot underlying intrinsic value on both the downside and the upside. Recent history has shown it can make sense to stay the course during a segment sell-off rather than panic.

When higher liquidity costs signal value

During the 2013 taper tantrum, New York Life stepped up to buy investment-grade and high-yield bonds, according to Bloomberg News. Tom Girard, head of fixed-income investments at New York Life, said the declines were “exaggerated because the need for liquidity was in excess of what the dealer community could provide.” What about the next sell-off? Girard adds: “If we get another situation similar to that taper tantrum … it starts to shift from a challenge to an opportunity.”

- There’s typically a buyer for most securities at a certain price. If we look at the investor landscape today, there is a lot of cash on the sidelines earning very little return and looking for a home. Consider a scenario in which investors are spooked by rising rates, and market prices for investment-grade bonds start to fall. Other investors will likely be looking to “leg in” to the sector as market prices drop in order to generate attractive risk-adjusted returns over the longer term (see sidebar on page 4).

- The industry, with the encouragement of the SEC, is seeking ways to reduce liquidity price risk for investors by looking outside of traditional dealer market-making. This includes efforts to centralize trading venues through enhanced use of electronic communications networks (ECNs), exchanges and clearinghouses.

Understanding liquidity repricing risk and market price volatility is key for fixed-income investors in today’s environment:

- Keep a steady hand through volatile market pricing cycles. It is very difficult to time or predict market disruptions or periods of large net outflows in specific market segments. The opportunity cost of carrying cash to implement market-timing strategies can be very high and in general, when liquidity costs are high, markets can recover relatively quickly.

- Consider a multisector strategy Managers of such strategies are continually seeking relative value among different market sectors and may be better positioned to take advantage of sell-offs in specific segments.

- Consider a laddered bond strategy. The idea is to “ladder” bond maturities in a portfolio from short to long. When rates rise, the proceeds of maturing short-term bonds can be reinvested in longer-term bonds at higher yields. This allows fixed-income investors to dollar cost average into the market and maximize return in a rising interest-rate environment. This assumes we have a positively sloping yield curve – the most common kind, like today’s curve, in which long-term bonds yield more than short-term ones.

Index Definitions

Barclays U.S. Aggregate Bond Index is an unmanaged index of domestic investment-grade bonds, including corporate, government and mortgage-backed securities.

S&P/LSTA Leveraged Loan Index is an unmanaged index of the institutional leveraged loan market.

BofA/Merrill Lynch High-Yield Master II Index is an unmanaged index of below-investment-grade U.S. corporate bonds.

Barclays Municipal Bond Index is an unmanaged index of municipal bonds traded in the U.S.

BofA Merrill Lynch Indexes: BofA Merrill Lynch™ indexes not for redistribution or other uses; provided “as is,” without warranties, and with no liability. Eaton Vance has prepared this report, BofA/Merrill Lynch does not endorse it, or guarantee, review or endorse Eaton Vance’s products.

Unless otherwise stated, index returns do not reflect the effect of any applicable sales charges, commissions, expenses, taxes or leverage, as applicable. It is not possible to invest directly in an index. Historical performance of the index illustrates market trends and does not represent the past or future performance of any investment.

About Risk

An imbalance in supply and demand in the income market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. Investments in income securities may be affected by changes in the creditworthiness of the issuer and are subject to the risk of nonpayment of principal and interest. The value of income securities also may decline because of real or perceived concerns about the issuer’s ability to make principal and interest payments. As interest rates rise, the value of certain income investments is likely to decline. An imbalance in supply and demand in the municipal market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. There generally is limited public information about municipal issuers. As interest rates rise, the value of certain income investments is likely to decline. Investments involving higher risk do not necessarily mean higher return potential. Diversification cannot ensure a profit or eliminate the risk of loss.

Important Information and Disclosure

This material is presented for informational and illustrative purposes only as the views and opinions of Eaton Vance as of the date hereof. It should not be construed as investment advice, a recommendation to purchase or sell specific securities, or to adopt any particular investment strategy. This material has been prepared on the basis of publicly available information, internally developed data and other third-party sources believed to be reliable. However, no assurances are provided regarding the reliability of such information and Eaton Vance has not sought to independently verify information taken from public and third-party sources. Any current investment views and opinions/analyses expressed constitute judgments as of the date of this material and are subject to change at any time without notice. Different views may be expressed based on different investment styles, objectives, opinions or philosophies. This material may contain statements that are not historical facts, referred to as forward-looking statements. Future results may differ significantly from those stated in forward-looking statements, depending on factors such as changes in securities or financial markets or general economic conditions. Actual portfolio holdings will vary for each client.

Investing entails risks and there can be no assurance that Eaton Vance, or its affiliates, will achieve profits or avoid incurring losses. It is not possible to invest directly in an index. Past performance is no guarantee of future results.

©2015 Eaton Vance Distributors, Inc. | Member FINRA/SIPC | Two International Place, Boston, MA 02110 | 800.836.2414 | eatonvance.com