Uncertainty over the outlook for Greece’s place in the eurozone, along with significant volatility in Chinese markets, have been major drivers of asset prices during the last month — pushing aside consideration of economic growth and monetary policy. Some moderation of the former concerns should allow the latter considerations to return to the fore as we head into the heart of summer in the Northern Hemisphere. The Greek negotiations may best be described as bewildering — as the government now has to garner support for harsher provisions than those rejected by the government-called referendum. There are many negotiations, and votes, ahead as Greece struggles to secure its third bailout from Europe. Disappointingly, however, the current framework seems to heavily favor the creditors, with little structure that would facilitate improving growth and debt sustainability.

Chinese markets finally lost some of their record-setting steam, but the severity of the decline led to a surprisingly strong intervention by the central government. With nearly 50% of Chinese stocks halted for trading at the peak (mostly by the companies themselves), the government’s policies flipped from a focus on restraining margin lending to the promotion of share purchases by the country’s major brokerage firms. While this level of involvement is a step back from the goal of greater market liberalization, the severity of the declines seems out of step with the pace of gradual slowdown in the real economy. Just as Chinese growth has been slowing this year, the U.S. economy isn’t in danger of hitting “escape velocity” anytime soon. The U.S. economy contracted by 0.2% in the first quarter, and growth is expected to increase toward a 3% pace for the remainder of the year — leaving yearly growth below 2.5%.

Europe’s economic growth looks relatively predictable this year, save the risk of Greek-related disruptions. European growth is expected to flirt with 2%, after growing 1.4% in 2014, and is benefitting from the 19% depreciation of the euro against the dollar from year-ago levels. The resulting dollar strength remains a drag on U.S. corporate revenue and earnings, and has likely been a restraining factor on the Federal Reserve’s plans to start raising the Federal Funds rate. Market expectations around the first rate hike have been pushed out to February 2016 — but we think it’s still likely that the Fed will raise rates this year. Recent commentary from Fed officials confirms both the Fed’s interest in finally moving off zero interest rates, but also its unwillingness to do so if the economic data deteriorates from here.

U.S. EQUITY

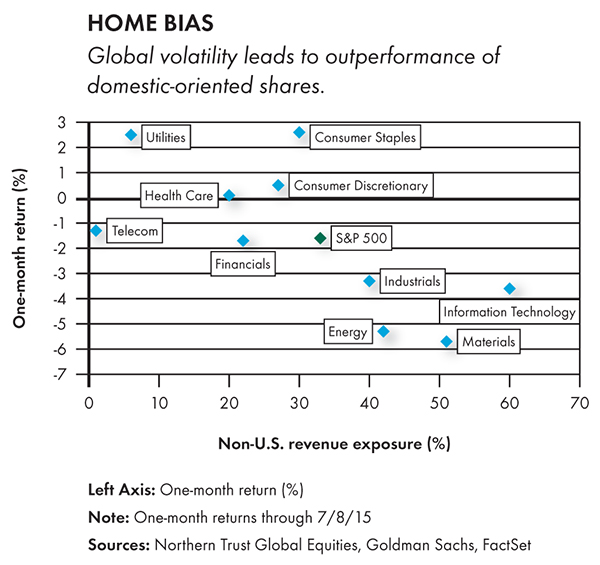

- One-third of S&P 500 revenues come from outside the United States.

- Global turmoil has led to steeper sell-offs in sectors most exposed to non-U.S. revenues.

The recent sharp decline in Chinese stock prices and increase in the probability of a “Grexit” have led to heightened volatility in U.S. equity markets during the past month. One-third of S&P 500 revenue is derived from outside the United States, justifying some investor concern. During the past 30 days, the Shanghai Composite fell nearly 30%, though shares in Europe are down just under 3% and U.S. large-cap stocks are down 1.6%. Declines have been more notable, however, in U.S. sectors with a greater reliance on non-U.S. revenues, including technology, basic materials, energy and industrials. Overall, with an estimated 12% of revenues coming from Europe, the Middle East and Africa, 8% from Asia-Pacific, and 4% from emerging markets, risks to U.S. corporate earnings remains modest, justifying the recent outperformance of U.S. shares.

EUROPEAN EQUITY

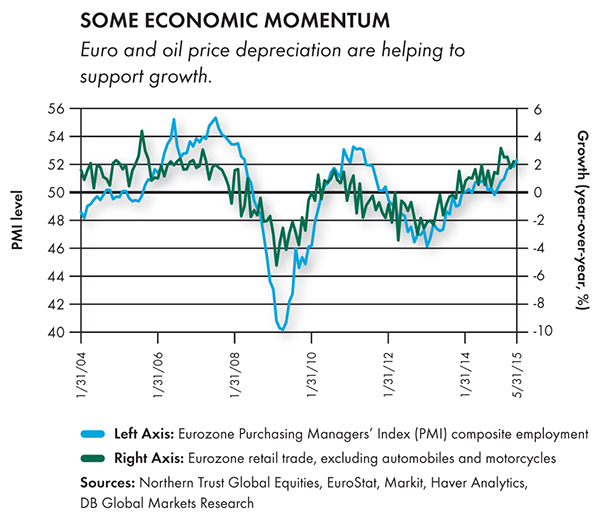

- The European economic recovery continues amid slow structural reform.

- A weaker euro and lower oil prices should benefit the European economy.

European equity markets gave back some gains during the last month but maintained high single-digit gains (in euros) at the time of this writing. Despite recent market concerns about a “Grexit,” the European economy continues to recover. A more competitive currency and lower oil prices have provided increased stimulus to eurozone economies, and the beneficial effects are beginning to show. Europe’s Purchasing Managers’ Index Composite Employment reading of 52 continues to improve, along with retail trade (excluding autos), which is growing at 2% (near 2006 and 2010 levels). Structural reform could provide uncertainty and headwinds in the near-to-intermediate term, and needs to be monitored closely, especially if it affects credit. However, the underlying economy continues to show improvement that should benefit long-term investment horizons.

ASIA-PACIFIC EQUITY

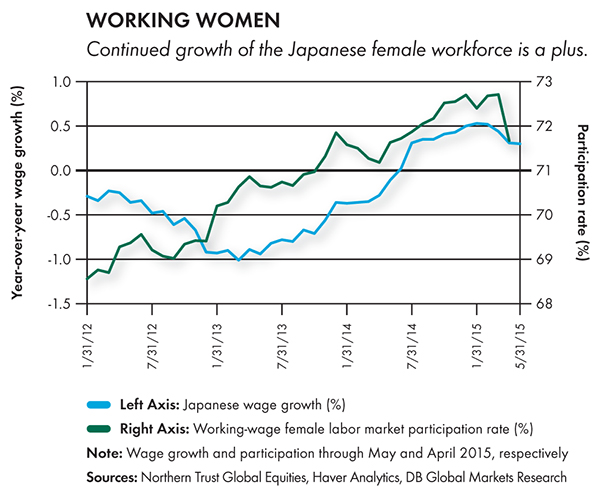

- An aging population remains problematic for Japan’s long-term outlook.

- Increased female labor market participation in Japan could bolster growth.

Japan’s Nikkei 225 moved lower with global equity markets last month, but is still holding a healthy, low double-digit gain since the end of last year. Capital allocation is starting to slowly improve, but a lingering concern over the long term is Japanese demographics. An aging population and shrinking labor force can exert a strong and lasting deflationary force on an economy. With immigration generally less robust in Japan, it’s unlikely to help alleviate this dynamic. Another avenue is to increase labor participation rates, especially among women. While there already had been a subtle rise in participation of working-age women, the rise has accelerated since the commencement of Abenomics in late 2012. Further policies to encourage gains in the female participation rate would pay dividends over both the short and long term.

EMERGING-MARKET EQUITY

- The fever in Chinese equities has broken.

- Government intervention could set back reform efforts.

The great bull market in Chinese stocks of the last year has been interrupted, and the catalyst may well have been MSCI’s decision to defer adding China’s A-shares to the MSCI’s emerging-market index. However, the government’s heavy involvement in trying to stabilize market values — and the large percentage of stocks where trading was suspended by the companies themselves — may give MSCI pause before the next review. With its closed capital account and active domestic investor base, the rolling one-year correlation between the returns of Chinese stocks and global equities has been low. Recent weakness in Chinese equities likely overstates economic softness but we still expect Chinese and broader emerging-market growth to disappoint during the next year, supporting our tactical underweight to emerging-market equities.

REAL ASSETS

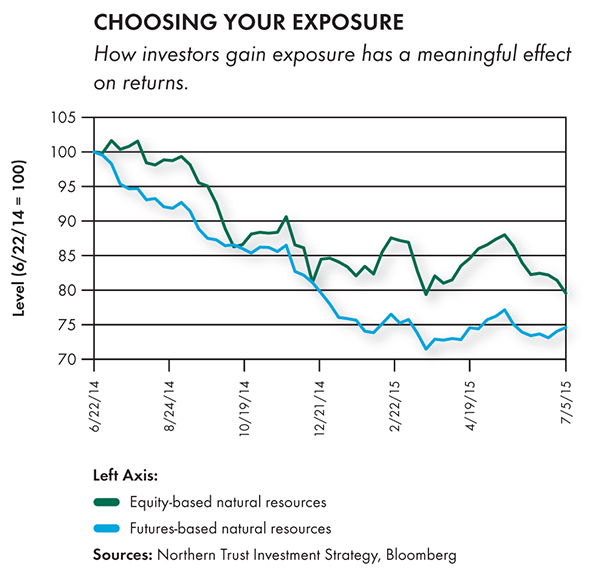

- Natural resource investing requires understanding your equity exposure.

- Natural resource exposure looks more appealing long term than short term.

The recent increase in equity market volatility serves as a reminder of the inherent differences between equity- and futures-based approaches to natural resources. As equity markets sold off during the past two months, natural resource equities underperformed natural resource futures contracts by almost 6%. It’s this same exposure to the equity markets that allowed natural resource equities to outperform a futures-based strategy by 15% in the year prior to Greek default risk escalation when commodity prices were falling. While “upstream” natural resource companies are highly correlated to the underlying prices of those natural resources, investors must also be aware of the exposure to the broader equity markets. Regardless of the approach, constructive longer-term supply/demand dynamics in natural resources are currently being trumped by cyclical weakness, leaving us tactically underweight the asset class.

U.S. HIGH YIELD

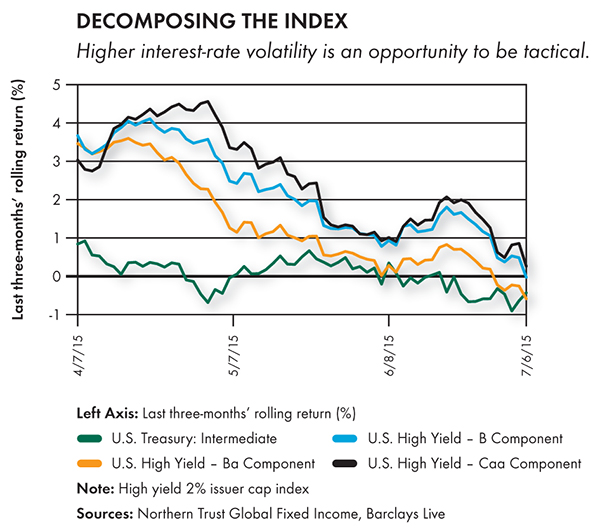

- High yield historically performs relatively well as interest rates rise.

- Actively managing interest-rate exposure can enhance performance.

The high yield market has returned 2.54% year-to-date through July 6. While first-quarter returns reflected credit risk, the second quarter was influenced by interest-rate risk. The credit component of high yield securities has historically allowed high yield to perform well in periods of rising interest rates. However, active management of interest-rate exposure can further enhance returns. Higher-rated securities have greater correlation with interest rates than lower-rated securities. In periods influenced by interest rates, Caa and B securities materially outperform Ba securities and treasuries. In addition, Ba securities underperform treasuries. Because high yield trades on price rather than spread, the lack of demand for interest-rate-sensitive securities results in underperformance relative to the underlying treasury. High yield carries risks other than default risk, and actively managing interest-rate exposure can further enhance performance.

U.S. FIXED INCOME

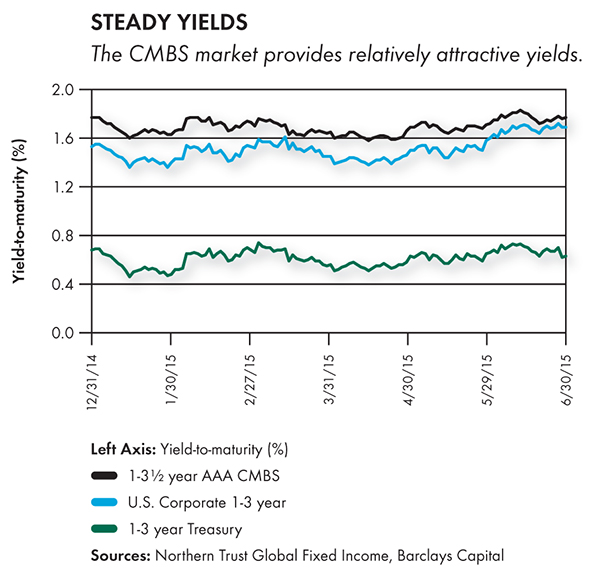

- The fundamentals of the commercial real estate market continue to improve.

- Short AAA-rated commercial mortgage backed securities (CMBS) offer attractive relative value.

Fundamentals in the commercial real estate market have been benefiting from the slow but steady recovery of the U.S. economy, along with higher occupancy rates, limited new supply and lower delinquency rates. As a result of the low-interest-rate environment across the globe, investors have been forced to search for yield in less traditional asset classes, with the CMBS market being one such asset class. We believe that AAA-rated CMBS with weighted average lives between one and three years offer significant yield in comparison to cash or U.S. Treasuries and look attractive relative to lower-rated corporate bonds. Additionally, short-term, high quality CMBS exposure may provide investors with some reprieve from the recent volatility experienced in the corporate bond market.

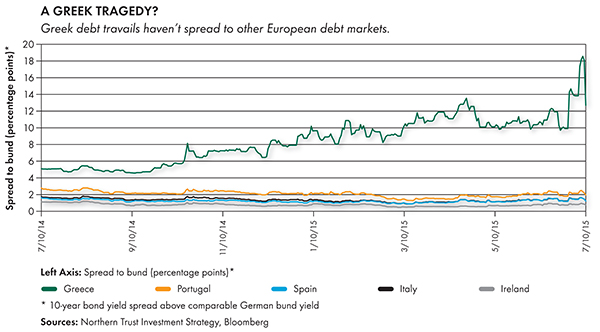

EUROPEAN FIXED INCOME

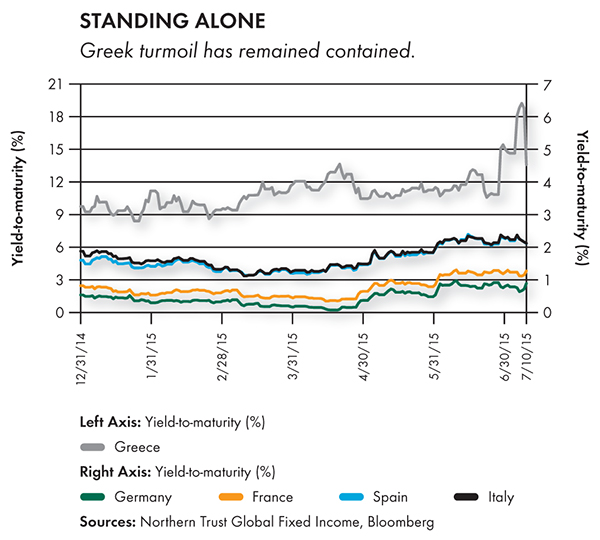

- Some clarity on Greece’s future in Europe is likely to appear soon.

- The United Kingdom remains a poster child for austerity.

Negotiations between European authorities, the International Monetary Fund and Greece continue to advance the potential of a near-term bailout deal, but time is short. The construct of the current deal being discussed seems to heavily favor the creditors, with little focus on restoring growth. European markets appear sanguine about the outcome, and any fallout should be short lived as the region is less exposed now, given the lead time on events. The U.K. government’s first Conservative budget in almost 20 years continues to bang the austerity drum with a focus on welfare spending cuts. More interestingly, the government’s pledge to raise the minimum or “living wage” against tight labor market conditions may make it easier for the Bank of England to raise interest rates in coming months.

ASIA-PACIFIC FIXED INCOME

- Chinese authorities are under pressure as stock markets unravel.

- New Zealand is moving back toward record-low interest rates.

After announcing several monetary easing measures in recent months in response to the economic slowdown, Chinese authorities surprised markets by embarking on direct policies to support market confidence. It’s debatable how much investor confidence will be supported, given the Shanghai Composite Index fell nearly 30% from its recent peak and almost 50% of stocks halted trading. Given the aggressive stance in addressing economic concerns, it seems likely that the People’s Bank of China is far from done. Less than a year after the last interest rate increase, the Reserve Bank of New Zealand has reversed course and cut the official target rate to 3.25%. With business confidence at a three-year low, this move is unlikely to be the last. Currency strength has been a widely noted concern, but was a likely consequence of earlier policy tightening.

CONCLUSION

Last month we said that the odds favored some sort of “kick the can down the road” agreement between Greece and its creditors, and it looks like that may be coming to pass. While there’s still much work to be done, the tone of the current agreement seems focused on avoiding a euro exit and debt write-downs, while ignoring growth-oriented policies. With the hard decisions yet again put off for another day, this should be euro-weakening, all else equal. On top of the nearly 20% decline in the euro/dollar exchange rate during the last year, Europe’s economy should gain some benefit from more competitive exports. However, Europe’s growth has been more dependent on improving domestic consumption than exports as global growth has disappointed. This is also critical when analyzing European equities, which generate only about 55% of revenue from Europe itself.

One of the prominent themes from our upcoming 2015 Capital Markets Assumptions whitepaper is “the slow burn of low growth.” This theme is clearly evident in the economy this year, as we are again experiencing disappointing global growth. High debt levels that persist from the global financial crisis are leading to fiscal problems in economies as diverse as Puerto Rico, Greece and China. While elevated debt levels suppress growth potential, they’re also deflationary. With most major economies experiencing inflation below targeted levels, there’s little pressure on central bankers to raise interest rates. We continue to expect the Fed will begin its liftoff from zero interest rates this year, ahead of market expectations, but think the market’s discounting of 0.50% in rate increases during the next year is on target. This level of rate normalizing in the United States should be manageable for the financial markets.

This month we made an additional risk reduction in our global tactical asset allocation model, reducing our exposure to emerging-market equities and natural resources (1% each), with the proceeds moving into U.S. investment-grade bonds. This was done to reflect the continuing soft growth environment in the emerging markets, and follows similar risk-reduction recommendations which started in the fourth quarter of 2014. The end result is a tactical portfolio that has an overall risk level in line with our long-term asset allocation — meaning we’re making no tactical bet on a large move in risk assets over the coming year. The growth outlooks in the United States and China are the most important variables to the risk outlook during the next year, while the risk of dollar strength remains a downside risk. Finally, Europe’s response to the Greek situation is unfortunately shaping up to be disappointing. While policy makers may be reducing near-term risk, the lack of focus on growth-oriented policies is an opportunity lost.

(c) Northern Trust