In the U.S., the consumer economy is strengthening, while the industrial economy continues to struggle. What does it mean for equities?

SUMMARY

- While the U.S. economy overall has been strengthening, we would describe it as a “two-speed” economy, with the general health of the U.S. consumer improving rapidly, while the industrial side continues to struggle.

- It appears that the U.S. equity market has begun to “figure things out,” as the S&P consumer discretionary sector has handily outperformed the S&P industrials sector in recent months.

- We continue to believe that until the opportunity set changes, investors should be patient and selectively favor shares of companies with management teams that allocate capital well.

Janet Yellen and her colleagues at the U.S. Federal Reserve (Fed) will spend the coming weeks and months contemplating the timing of an increase in short-term interest rates. While a cynic might describe the Fed’s behavior as “reactionary,” the Fed itself prefers the term “data-dependent.”

As the Fed monitors incoming data, it will be searching for signs of the overall strength of the economy and any associated inflationary pressures. In so doing, the Fed is likely to find a two-speed economy, with the general health of the U.S. consumer improving rapidly, while the industrial side of the economy continues to struggle.

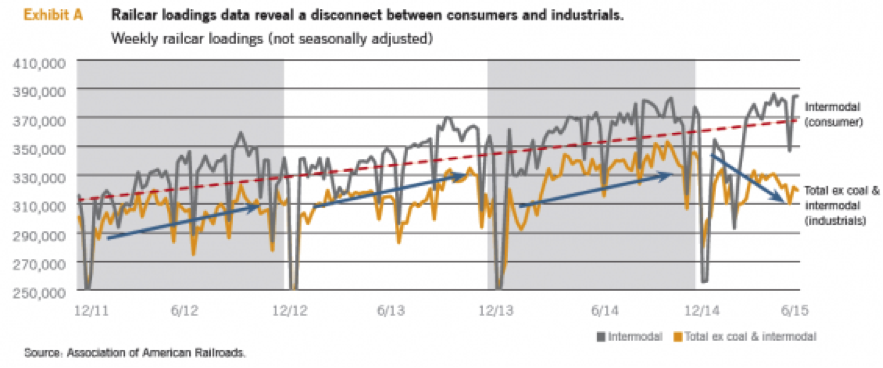

Look to Transportation

One of the best places to look for an early read on the economy’s direction is the transportation industry. Whether it’s a consumer product headed for the store shelf, coal on its way to a power plant or steel mill, or other raw materials being taken to a factory for production of an intermediate good, a train or truck is usually involved in the process.

Exhibit A shows weekly railcar loadings, as reported to the Association of American Railroads. “Intermodal” represents goods that are transported using two or more modes of transportation (i.e., ship, rail and road). These are typically finished goods and are a good proxy for consumer merchandise. The second line, labeled “Total ex coal & intermodal,” is primarily bulk commodities and can be viewed as representing the industrial side of the economy. Notice the divergence of fortunes between the two over the past few months.

Falling Oil Prices: Good for Consumers, bad for industrials

Part of the explanation for this seeming disconnect in economic data lies with energy prices. Over the past 12 months, the price of a barrel of oil has fallen 43%, from $105 to $60. This has led to a drop in average U.S. gasoline prices from approximately $3.70/gallon to $2.75/ gallon. With more money in their pockets, U.S. consumers (at least those who drive) are apparently feeling somewhat better about things. Accordingly, the University of Michigan Consumer Sentiment Index recently neared its five-year high.

While the collapse in oil prices has been good news for the consumer, it’s bad news for many industrial companies. Oil and gas is an important end market for capital goods and equipment manufacturers. We have been struck by how rapidly the energy sector cut expenses at the beginning of 2015. North American exploration and production companies tell us they have cut capital spending by roughly 35% this year. This has had a ripple effect throughout the supply chain, well beyond the direct exposure of oil and gas equipment. The softness in the industrial part of the economy has begun to manifest itself in the form of lower utilization rates at U.S. factories.

A Better Job Market: More Good News for Consumers

Aside from lower energy prices, another big reason for the greater optimism on the part of many consumers is the recent improvement on the jobs front. After topping 10% in 2009, the U.S. unemployment rate has steadily fallen since then and is now at what many would consider a more “normal” level – 5.3% as of June 2015. Perhaps even more telling is that wage growth has finally begun to pick up after years of stagnation.

Bringing it Back to Equities

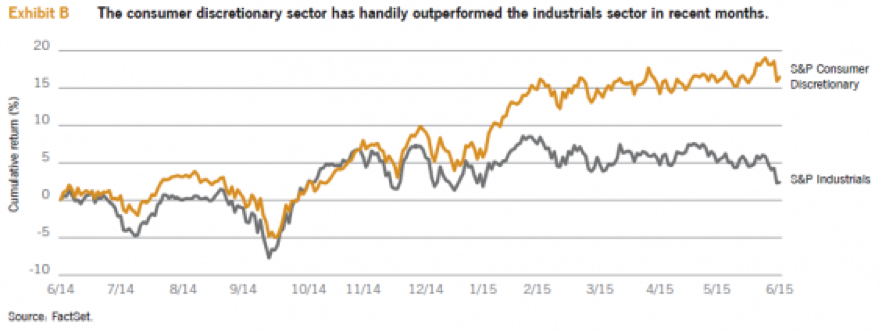

Understanding the relative health of different segments of the economy is important, but for equity investors, the key question is always, “What’s not priced in?” Looking at the trailing 12-month performance of the consumer discretionary and industrials sectors within the S&P 500 Index, it seems clear that the U.S. equity market has begun to figure things out, as consumer discretionary stocks have handily outperformed industrials over the past several months (Exhibit B).

This divergence of performance between the two sectors has led to widening valuation differentials: Consumer discretionary stocks were recently valued at 19.5x forward EPS estimates, whereas industrials stocks were only valued at 16.3x.

In the Eaton Vance Large-Cap Value strategy, we have recently been cutting back our consumer discretionary exposure and have been adding to industrials. Meanwhile, in our growth strategies, we have recently had underweight positions in industrials. Our growth team has continued to be optimistic about the outlook for companies that it believes to be benefiting from strong, secular growth trends in the areas of consumer, technology and health care, among others.

Be Patient (and Selective)

Regardless of where there may (or may not) be opportunities in today’s equity market, our view remains that true bargains are far from plentiful. However, as we pointed out in last quarter’s insight, that could change in the months ahead. In the interim, we continue to believe investors should selectively favor shares of companies with skilled management teams that allocate capital well.

About Risk

Investments in equity securities are sensitive to stock market volatility. Equity investing involves risk, including possible loss of principal. Investments in foreign instruments or currencies can involve greater risk and volatility than U.S. investments because of adverse market, economic, political, regulatory, geopolitical or other conditions. In emerging countries, these risks may be more significant.

Past performance is no guarantee of future results.

About Eaton Vance

Eaton Vance Corp. is one of the oldest investment management firms in the United States, with a history dating to 1924. Eaton Vance and its affiliates offer individuals and institutions a broad array of investment strategies and wealth management solutions. The Company’s long record of exemplary service, timely innovation and attractive returns through a variety of market conditions has made Eaton Vance the investment manager of choice for many of today’s most discerning investors. For more information, visit eatonvance.com.

The views expressed in this Insight are those of Edward J. Perkin and are current only through the date stated at the top of this page. These views are subject to change at any time based upon market or other conditions, and Eaton Vance disclaims any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Eaton Vance are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Eaton Vance fund.

This Insight may contain statements that are not historical facts, referred to as forward-looking statements. Future results may differ significantly from those stated in forward-looking statements, depending on factors such as changes in securities or financial markets or general economic conditions.

Before investing, investors should consider carefully the investment objectives, risks, charges and expenses of a mutual fund. This and other important information is contained in the prospectus and summary prospectus, which can be obtained from a financial advisor. Prospective investors should read the prospectus carefully before investing.

©2015 Eaton Vance Distributors, Inc. | Member FINRA/SIPC | Two International Place, Boston, MA 02110 | 800.836.2414 | eatonvance.com