Many media organizations and smart money managers are postulating that today’s 22-35 year old age group (millennials) might be the first generation since World War II to not marry, have children, buy cars and buy houses at high enough percentages to help us fully recover from the financial meltdown of 2007-09.

A recent trip to New York reminded me of the potential economic opportunity for the next three to five years. I looked out of my hotel window across the street to the headquarters of a Fortune 500 company. Next door, a group of construction workers were starting their day on the roof. As I gazed back into the open offices, it hit me—the success of the U.S. economy over the next ten years could be determined by the primarily college-educated folks working in open offices. Will they employ blue-collar workers in industries like construction and auto manufacturing through their consumption?

As contrarians and seekers of the truth, we are not happy to stop at the consensus opinion created by backward-looking statistics and assume the worst about today’s young people. We have learned that media outlets collect and permeate what we call the “well known fact.” This is a body of economic information which is known by nearly everyone and has been acted on by everyone with available capital.

We think today’s “well known fact” is “it is different this time” and a large percentage of Americans won’t form households, won’t buy houses and won’t employ the folks that build them. John Templeton, one of the great stock-pickers of the 20th century and pioneer of global mutual funds, was fond of saying that the five most costly words in investing are “it is different this time.”

Numerous other experts and media outlets have weighed in on the subject. Bond maven, Jeff Gundlach, and real estate king, Sam Zell, are postured for a “re-urbanization” of America. They believe that young married couples will stay in the city.

We will break our discussion of where we are heading into four categories. First, we will look at the sheer number of Americans who can marry and have kids and compare them to recent population groups. Second, we will examine the economics of buying a home versus renting. Third, we will look at the balance sheet and income statement of the average household in America and see the statistically aberrational effect that today’s 25-34 year olds have had. Lastly, we will look at the connection between the housing depression we are coming out of, the sense of well-being on the part of blue-collar Americans and the changes it could bring to the economy and U.S. stock market.

Sheer Millennial Population Numbers

There are 86 million Americans between the age of 19 and 37 years old. The absolute largest single year of population is about to turn 24 years of age. To put this into perspective, there are 80 million baby boomers in the U.S. An easy way for us to think about this is the difference between boomers, gen-Xers and millennials. There are approximately 25% more boomers than Xers and 30% more millennials than Xers.

In the study of economics, we learn that changes at the margin are powerful. The absolute difference in population group size refutes the argument that social differences between the generations will damage our economy. Some believe that a larger number of the millennial group will not do what prior groups did—buy houses, build families, etc. If that amounts to 5-10% of them, it means that there will still be between 17 to 23.5% more home and car buyers on average in the next ten years than the last ten years.

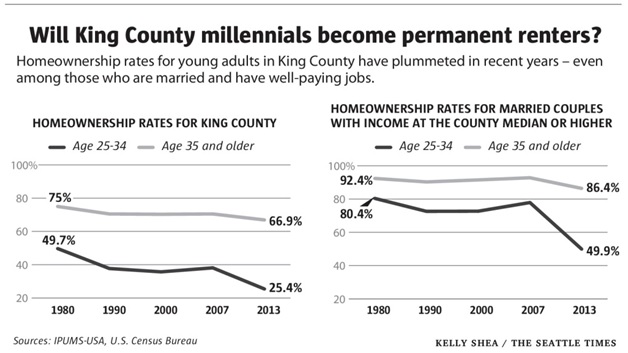

We work and live in Seattle, which has one of the highest concentrations of highly-educated people working in open-office environments. In an impressive piece from our own Seattle Times called, “Homeownership plunges among millennials in King County,” columnist Gene Balk shared the facts on a very hot housing market in the Seattle Metropolitan area:

Census data show that the rate of homeownership for the county’s 25- to 34-year-olds is the lowest it’s been since the Gold Rush era. Among county households headed by someone in that age group, just one out of four own their home — about the same as it was back in 1900.

Look at the stats provided on King County. It shows that 66.9% of those over 35 years old own a home and the current 25-34 year olds are at 25.4% home ownership. Any arbitrageur would tell you that betting on the aging of millennials to move the 25.4% number toward 66.9% is as simple as investing the time involved. Also, the married with high income rate of home ownership at 49.9% is probably heavily impacted by the postponement of child bearing until their thirties.

Housing is Incredibly Affordable

Many studies have recently shown how compelling buying a house is for the average household in today’s environment. The average renter in the U.S. spends 30% of their gross income on rent. The average household can buy the average house with a mortgage payment of 15% of their gross income. This is even a compelling story in the most expensive real estate markets like Honolulu, San Francisco, New York and Seattle.

Our gut feeling is that something will spark the first-time home buying and cause a rampage of interest over the next three to five years. Maybe it will be the massive number of weddings this summer and the babies which might come one year later. Southwest Airlines spent millions of dollars on a commercial in the spring which announced, “It is wedding season and we have fares as low as $73 each way.” They ran it during the NCAA Final Four Basketball Tourney, some of the most expensive advertising minutes of the year.

Great Balance Sheets and Income Statements

The balance sheet of American households has improved more in the last six years than almost any time in history. The Federal Reserve Board reported that the assets held by households grew by $18 trillion, while debts shrank by $250 billion since the last peak in 2007. The household debt service ratio (HDSR) has been below 10% for most of the last two years and in the deepest recessions of the last three decades it never got below 10.3%.1 This means that Americans have balance sheets and income statements which would support much higher rates of economic growth.

The difference in HDSR from the 1980’s and 1990’s and now is the financial behavior of our nation’s 22-35 year olds. When people married at 23 years of age, had babies in their twenties and bought homes and cars to fit their lifestyle, it put HDSR at higher levels. WHEN YOUR LARGEST POPULATION GROUP IS UNDER-OWNING HOUSES AND CARS YOU HAVE ABBERRATIONALLY LOW USE OF DEBT AND ANEMIC ECONOMIC GROWTH!

Let’s put all of this in a historical context. In the 1960 U.S. Census, there were 180 million people counted. The deepest recessions of the 1960’s and 1970’s saw a bottom at 1 million housing starts. In 2013 and 2014, we have recovered up to 1 million housing starts with a population of 325 million people in America.

We did some research recently and found that of the houses Americans live in today, around 10% of them were built in 1975-1980. What was going on back then? The largest population group (baby-boomers) was buying their first house in 1975-1980. Houses were incredibly unaffordable and interest rates were in the high double-digits! Much of what they did was based on necessity.

The kids require cars and ones which fit a car seat and a bunch of accessories. Two kids ultimately require a yard and an urge to get away from the noise you keep making that annoys your neighbor.

Whether you agree with the “re-urbanization” crowd or not, this massive group of people between 22 and 35 years of age are likely to cause a huge increase in home building and car buying compared to the last 8 years. Most of the people who work in a cubicle will demand the services of those who build cars and houses. Even most of the characters in the television show “The Big Bang Theory” will end up marrying and having kids.

The New Economic Picture

At the margin, a huge re-composition of household spending is likely to happen among the millennial group over the next three to five years. Visualize what you would see if you follow single folks between 25-30 years of age around for a couple of weeks and see what they spend money on. Then examine today’s equivalent of a 90-day check register for a 35-year old couple with a baby and a toddler. The single folks are probably pounding the daylights out of Chipotle, Shake Shack, craft beers and Apple electronic devices. The married couples with kids are likely going to Home Depot for home repairs, reading about local school board elections, buying diapers and cold medicine at Walgreen’s, and visiting Disney’s theme parks (or watching its movies and cable channels). If most things happen at the margin, we think this will be a drastic change, even if 5-10% of millennials stay in the city and forgo children.

The re-composition of household spending could cause a marked change in popularity among the sectors of the S&P 500 Index. If the people working in cubicles or open offices employ those who build houses and cars, the domestic economy of the U.S. should strengthen and maybe hit “escape velocity.” This GDP growth could be high enough to kick what economists like John Maynard Keynes call “animal spirits” into gear. How we prefer to think of this, is to think of today’s largest population group taking the risks that new household formation and family formation demand, as opposed to behaving financially like 55-70 year olds do.

To us, this means higher interest rates over the next five years, a strong U.S. dollar, and the S&P 500 Index bifurcated between the beneficiaries of the spending re-composition. This should tilt the economy toward higher blue-collar employment and higher wages for skilled trades. In turn, foreign sources of revenue might continue to get profits crimped by the stronger dollar. Finally, stock-picking organizations might have to anticipate who the winners are to beat the popular S&P 500 Index options.

[1] The Federal Reserve Board. “Household Debt Service and Financial Obligation Ratios.” Accessed June 30, 2015.

http://www.federalreserve.gov/releases/housedebt/.