Aside from two Federal Reserve releases, the only major news announcement was the ISM services index, which printed a very strong 56% headline number. New orders were a bullish 58.3 while employment was 52.7. The report contained the following anecdotal information:

- "Avian Influenza has significantly impacted business." (Agriculture, Forestry, Fishing & Hunting)

- "Strong Summer in the industry. Supply chain challenges due to the Avian flu." (Arts, Entertainment & Recreation)

- "Health care continues strong even with the looming negative impacts of Obamacare." (Health Care & Social Assistance)

- "Favorable weather is keeping transactions positive, as well as the planting season on schedule. Drought in CA may lead to higher costs. Lower fuel cost are allowing people to travel and eat out more often. GDP is down and employment numbers are still too low. Bird Flu is a big concern and is already affecting chicken costs." (Accommodation & Food Services)

- "The earlier surge this year in new business has slowed and remained constant." (Professional, Scientific & Technical Services)

- "Activity picking up as the federal government nears late Q3 and early Q4 spending." (Public Administration)

- "The overall business outlook remains strong and performance in our market has been very good." (Retail Trade)

- "Our sales are still trending up year-to-date versus last year-to-date."(Wholesale Trade)

Aside from the bird flu issues, the overall tenor of the comments was bullish.

Last week, the Federal Reserve issued two important reviews of the economy: the most recent meeting minutes and a speech by Chairperson Yellen. The Minutes offered the following general assessment of the economy:

The information reviewed for the June 16-17 meeting suggested that real gross domestic product (GDP) was increasing moderately in the second quarter after edging down in the first quarter. Labor market conditions improved somewhat further in recent months. Consumer price inflation continued to run below the FOMC's longer-run objective of 2 percent and was restrained significantly by earlier declines in energy prices and decreases in prices of non-energy imports. Survey measures of longer‑run inflation expectations remained stable, while market-based measures of inflation compensation were still low.

The report also included the following observations:

- Although positive, industrial production was weak thanks to a strong dollar and weak oil prices

- Personal consumption expenditures were picking up

- Housing was picking up, although it was slow

- Cap-ex was slow

In general, the Fed committee saw a moderately expanding economy.

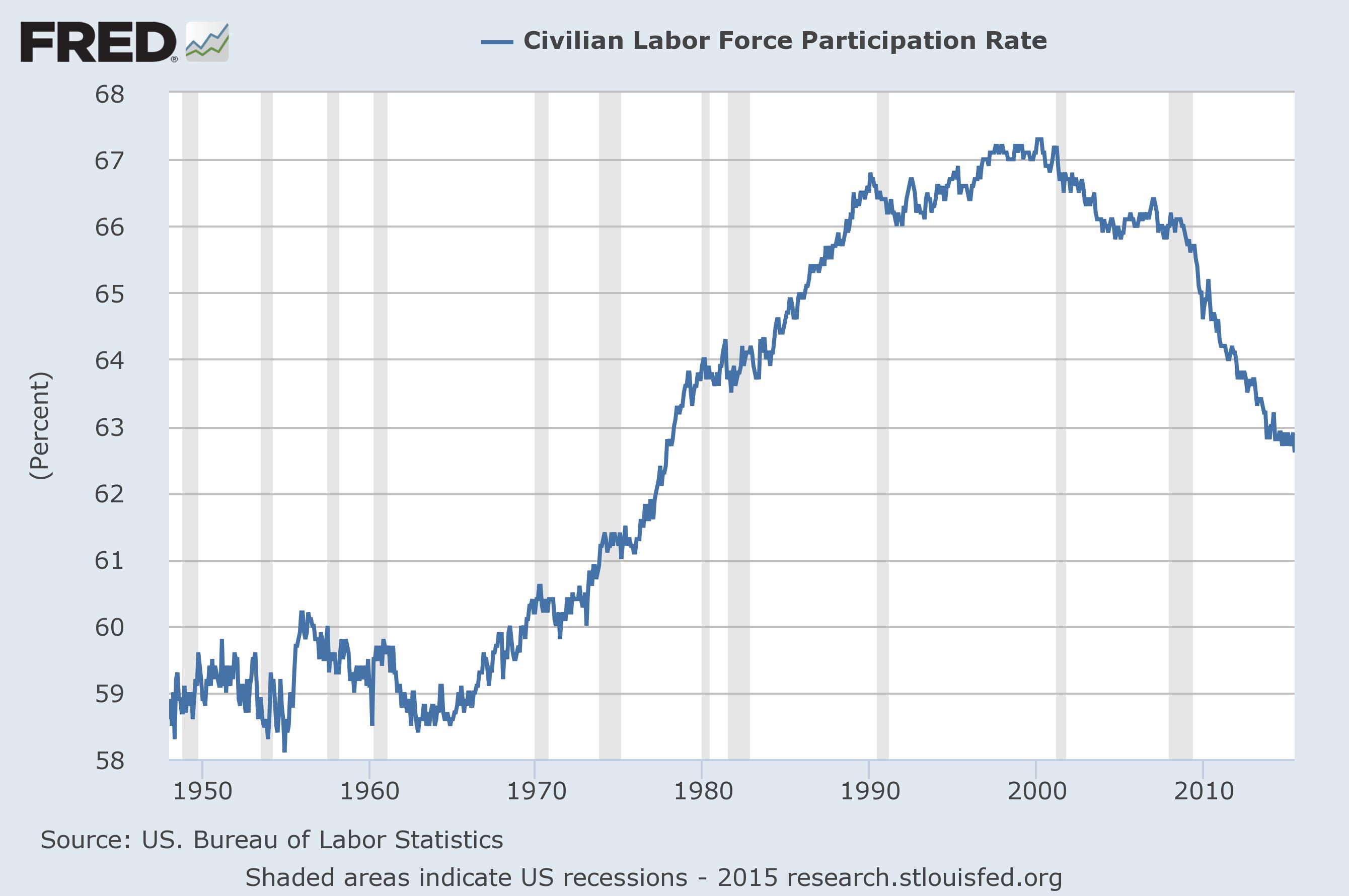

Chairperson Yellen’s speech focused on two key economic metrics: the labor market and inflation. Beginning with the labor market, she noted that while the unemployment rate has dropped, she doesn’t believe it is fully reflective of the labor market. She then discussed several broader measures of labor utilization starting with the labor force participation rate:

Many working-age people who are not in the labor force have chosen that status voluntarily; examples would include retirees, teenagers and young adults in school, and people staying home to care for children and other dependent family members. Even in a stronger job market, it is likely that many of these individuals would prefer not to work. And, indeed, a noticeable portion of the decline in labor force participation seen over the past decade or so clearly relates to the aging of baby boomers and their ongoing retirements. However, the pace of decline in the participation rate accelerated during the recession, as some individuals who lost their jobs became discouraged and stopped looking for work. It appears that, despite a drop in the participation rate reported in June, the pace of this decline has slowed since early last year. Nevertheless I think a significant number of individuals still are not seeking work because they perceive a lack of good job opportunities, and that a stronger economy would draw some of them back into the labor force.

Here's a chart of the indicator:

The LFPR has (unfortunately) become a politically charged number. Thankfully, Invictus over at the Big Picture Blog did the blogging world a great favor by locating a majority of the research on the topic. Here’s the short version: it was well known that the baby boomers would start retiring sometime in the 00s, leading economists to research the potential impact. Notice that Yellen’s last sentence is an opinion, which is a bit at odds with the research; according to the BLS:

Of note is the fact that the drop in the labor force participation rate was just 0.6 percentage point during the 2007–2009 economic downturn whereas, between 2009 and 2012, since the end of the recession, the rate declined by another 1.7 percentage points. A major factor responsible for this downward pressure on the overall labor force participation rate is the aging of the baby-boom generation.

In short, this is mostly a demographic issue.

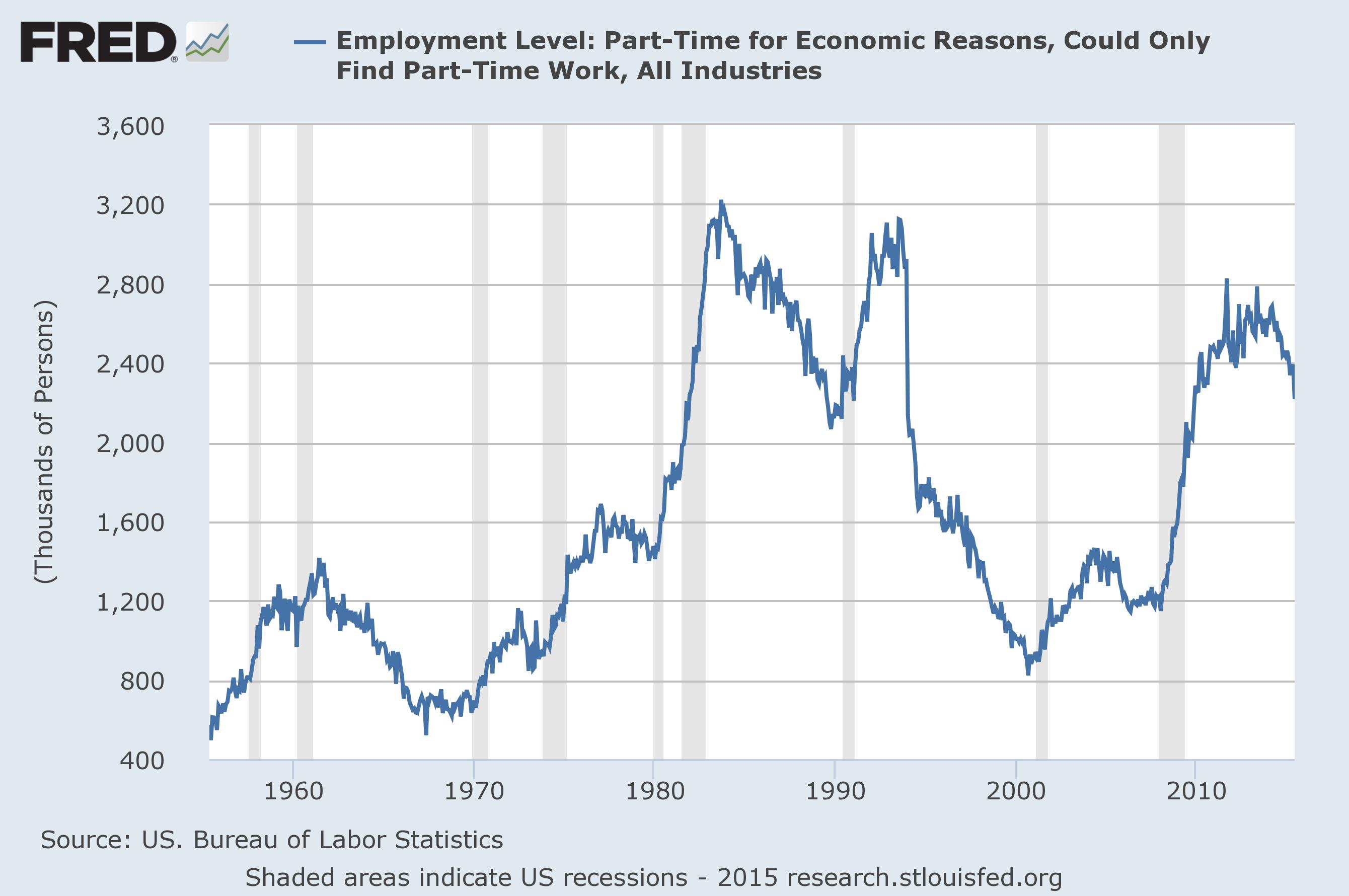

Yellen also mentioned the number of workers employed for part-time reasons, which is shown in this chart:

Yellen made these observations:

Some portion of the greater share of workers who are part time for economic reasons may reflect structural rather than cyclical factors.3 For example, the ongoing shift in employment away from manufacturing and toward services, a sector which historically relied more heavily on part-time workers, may be boosting the share of part-time jobs. Despite these structural trends, which make it difficult to know where the share of those employed part time for economic reasons may settle in the longer run, I continue to think that it probably remains higher than it would be in a full-employment economy.

Like her observations on the LFPR, Yellen ends by noting that, in her opinion, this number is negatively impacted by the economic environment. Remember that Chairperson Yellen has been studying the economy for over 40 years, and is probably one of the most credentialed Chairmen in the Fed’s history; her opinion is highly informed. And regarding this metric, I think she is likely correct.

Yellen then turns to prices:

Overall consumer price inflation has been close to zero over the past year, in large part because the big drop in crude oil prices since last summer has pushed down prices for gasoline and other consumer energy products.Price inflation excluding the volatile categories of energy and food prices, or so-called core inflation, is often a better indicator of future overall inflation. But it too is running below our 2 percent objective and has been over most of the recovery. The recent low level of core inflation -- 1.2 percent over the past 12 months -- partly reflects the appreciation of the foreign exchange value of the U.S. dollar during the second half of last year, as global financial markets seemed to judge that our economy was relatively stronger than those of many of our trading partners. The stronger dollar has pushed down the prices of imported goods, and that, in turn, has put downward pressure on core inflation. In addition, the plunge in oil prices may have had some indirect effects in holding down the prices of non-energy items in core inflation, as producers passed on to their customers some of the cost savings from lower energy prices. In all, however, these downward pressures seem to be abating, and the effects of these transitory factors are expected to fall out of measures of inflation by early next year.

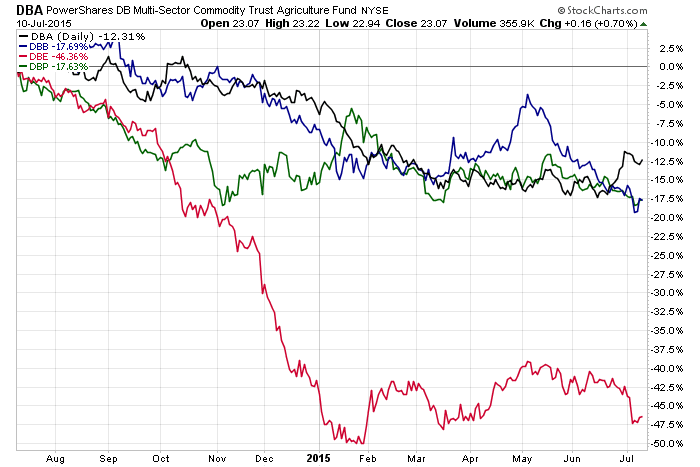

Yellen specifically mentions oil and the dollar. But all commodities – and hence, all input prices – are at low levels. Here is a chart of the ETFS that track, industrial metals, agricultural goods, energy and precious metals:

All are showing a negative return for the last year. While the dollar’s strength is partly responsible, China’s raw material appetite is decreasing. And there is a general over-supply of some raw materials. For example, Australian basic materials business is at the tail end of a massive infrastructure build-out that is flooding the market with ore. The combination of these factors should keep maintain downward pressure on prices for the foreseeable future.

Regarding rate hikes, she stated in the Q&A session that she expects a rate hike later this year:

"I expect it will be appropriate at some point later this year to take the first step to raise the federal funds rate and thus begin normalizing monetary policy," Yellen said in a speech to the City Club of Cleveland, a civic group that sponsors high-level speakers.

"But I want to emphasize that the course of the economy and inflation remains highly uncertain...We will be watching carefully to see if there is continued improvement in labor market conditions, and we will need to be reasonably confident that inflation will move back to 2 percent in the next few years."

It’s important to place the potential rate hike in context. Rates have been abnormally low for an extended period of time. The Fed is getting a bit itchy to return rates to what they feel is a more “normal” environment. Therefore, an increase would simply be the Fed saying, “See? Rates can go up.”

Finally, the Atlanta Fed GDP tracker continues to move higher:

Conclusion

Little changed in the Fed’s perception of the US economy. The reports continue to rely heavily on the adjective “moderate” to describe economic activity. From the policy perspective, the economy is in a sweet spot. Unemployment is low, but thanks to lower labor utilization rates wage pressures are weak. Raw material price pressures are down due to weakening Chinese demand, increasing global supply and a strong dollar.

The Markets

Overall, the market is a bit weaker this week:

The underlying technicals continue to move lower. The MACD and RSI are still in an overall declining position while prices drift lower. However, the 200 day EMA is still providing support as prices consolidate below the 206 price level. The big issue here is the 200 day EMA, which the index briefly took out last week. Ryan Detrick has some nice analysis on what this means at this link. Josh Brown and the Irrelevant Investor also have some great analysis on the topic. Here’s the short version: below the 200 day EMA we have weaker growth and higher volatility.

Supporting the market is the fact we’re at the beginning of earnings season, which started last week with Alcoa’s disappointing announcement. The market desperately needs to see companies print strong top line revenue growth. Unfortunately, companies will have a weaker overseas environment and strong dollar to contend with. Oil’s weakness is also hurting the energy sector. In short, don't expect a blow-out quarter.